The housing market in the United States and Canada continues to shift with interest rates, local job growth, and supply constraints. If you’re eyeing 2025, the big decision is whether you should flip for quicker profits or hold for steady appreciation and rental income. Both strategies can work. The right call depends on where you buy, how you finance the deal, and how much risk you’re comfortable taking.

This guide provides a practical approach, backed by facts and insights you can apply directly.

The Market Backdrop to Plan Around

You are likely to see a market that is still tight on inventory in many metros, with rates that have eased off peak levels but are not back to the ultra-low era. In the U.S., migration toward affordable, job-rich metros has stayed strong. In Canada, demand remains firm in cities that offer more value than the priciest cores. Think of this moment as a “quality-of-buy” market. The better your entry price, renovation scope, and financing plan, the better your outcome.

Before you choose a lane, narrow your focus to specific neighborhoods. Submarkets inside the same metro can behave very differently. Blocks with new employers, transit improvements, or school upgrades can outperform nearby areas that do not have those catalysts.

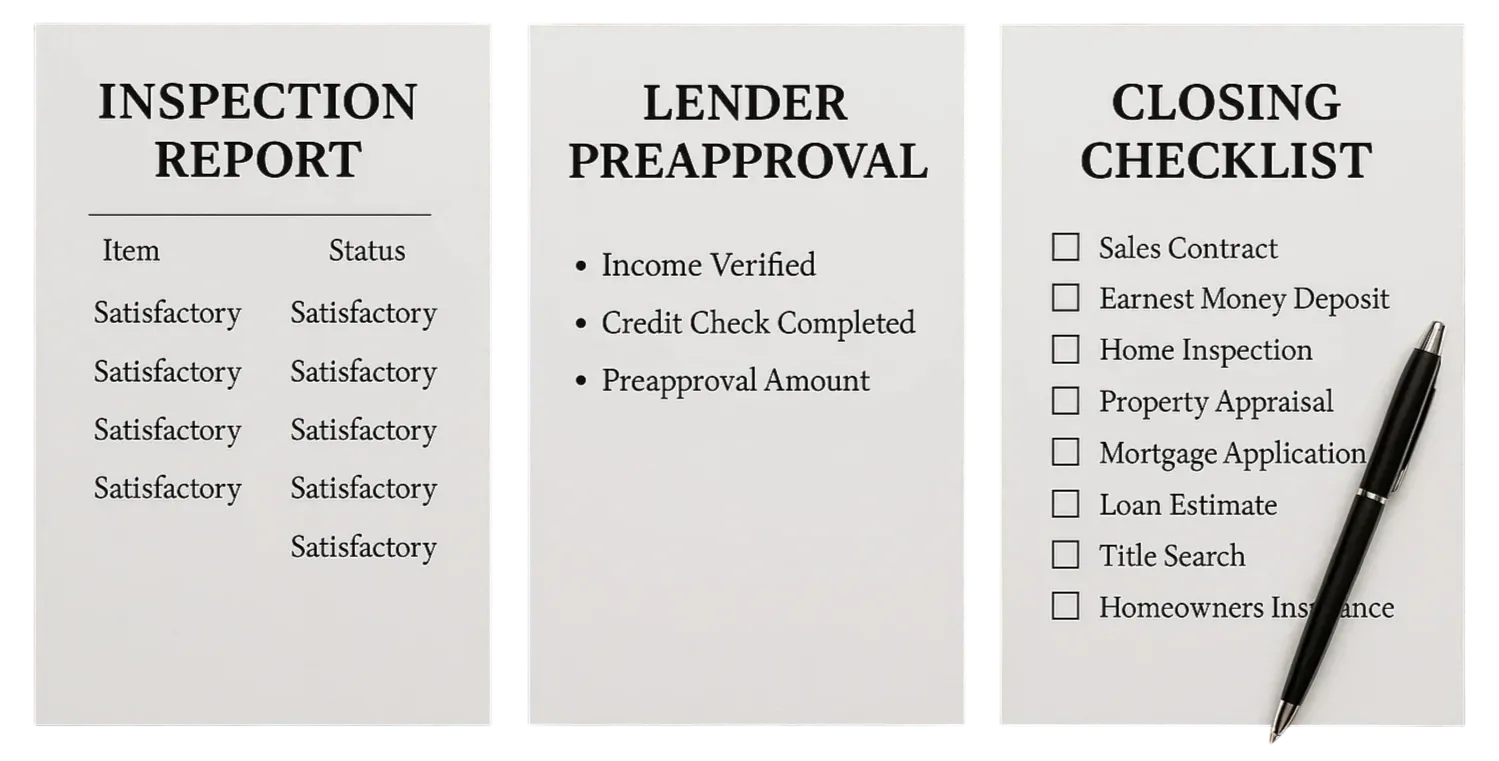

As you evaluate targets, build a closing checklist early. Line up your Closing Disclosure, title documents, and insurance proof so you can move quickly when a good deal appears. That prep work reduces last-minute friction and helps you avoid delays at the table.

Flipping in 2025: Risks, Rewards, and Realities

Flips win when you buy right, keep the renovation tight, and sell into solid demand. It sounds simple enough, yet in 2025 pulling it off will take sharper project management.

- Costs and Timing:

Material and labor costs remain elevated in many markets, and permit backlogs can push timelines. Build a conservative budget and timeline. Add a 10 to 15 percent cushion for surprises so carrying costs do not eat your spread. - Block-Level Demand:

Look for neighborhoods with rising household formation, healthy resale comps, and a clear ceiling price you can hit after improvements. Walk the street at different times of day and talk with property managers and contractors about days on market and buyer must-haves. - What to Renovate:

Aim for repairs that unlock buyer confidence and appraisal value. Kitchens, bathrooms, major systems, and curb appeal usually carry more weight than purely cosmetic upgrades.

If you’re writing an offer, protect your downside with a clean inspection playbook. Order a full home inspection right away and be ready to negotiate repairs or credits if issues pop up. Working with a top real estate agent can sharpen your terms and further protect you, especially on repair credits, appraisal gaps, and timeline risks.

In a competitive situation, you might shorten the inspection window instead of waiving it outright so you still preserve an exit if a major defect appears. Most buyers work within a 7- to 10-day inspection period, and sellers often respond within a few days after that.

Flips can still pencil if you buy with enough spread, control scope, and move decisively. The biggest risks are timeline slippage, change orders, and a softer resale window that stretches your holding costs.

The Long Hold: Build Wealth Through Time, Rent, and Discipline

A long-term hold combines gradual appreciation with rental income that helps cover the mortgage, taxes, insurance, and maintenance. If you prefer steadier returns and less day-to-day project risk, this lane often fits better.

- Durable rental demand:

Affordability pressures keep many would-be buyers in the rental pool, which supports occupancy and rent growth in the right neighborhoods. - Tax treatment:

In the U.S., long-term capital gains rates are generally lower than short-term rates. In Canada, principal residence rules and other planning strategies can reduce taxes when used appropriately. Consult a licensed tax professional to structure ownership appropriately for your situation. - Compounding effects:

Each rent check helps amortize your loan while the property can appreciate over time. Renovations you make are less about a quick retail pop and more about reducing future capex and vacancy.

Your operating checklist matters here too. Keep clean records, budget for repairs, and schedule regular inspections so small issues do not become expensive emergencies. When you eventually sell, you will still go through the same closing process buyers face today, including document prep, insurance verification, and a final walk-through that confirms property condition.

Flip Now or Hold Longer: How to Make the Call

Use side-by-side projections so you can compare cash today against total return over time. Here’s a simple way to frame it for a property you can buy at a fair price in a growth corridor.

Flip scenario

- Purchase at a discount.

- Tight, value-adding renovation.

- Clear exit comps within the next few months.

- Short-term, higher-rate financing that magnifies carrying costs.

- Execution risk is higher, but cash comes back faster.

Hold scenario

- Buy in a school district or job node that renters value.

- Stabilize with a targeted refresh that reduces repairs over the next five years.

- Traditional mortgage that a good rent can help service.

- Returns build through cash flow, principal paydown, and appreciation.

Run the numbers both ways, then stress-test them with longer days on market, a lower resale price, or a small rate increase. If you cannot absorb a slower sale or a vacant month, the flip may be too tight. If the cash flow barely covers the mortgage at conservative rents, the hold may need a better buy price.

As you negotiate, keep your inspection contingency and timelines front and center so you can exit or renegotiate if a major issue is uncovered. If the inspection reveals structural or safety problems, you can push for repairs, credits, or decide to walk away without risking your earnest money when the contingency is properly drafted and timed.

Practical Steps to Take

- Research the submarket, not just the metro. Track sales on the blocks where you plan to buy. Drive the area, talk to neighbors, and note any public works or new retail.

- Get your financing buttoned up early. Preapproval shows strength and keeps closing on schedule. Strong files help you avoid last-minute document chases and let you lock a rate within your lender’s timeline.

- Build a reliable team. For flips, you want a contractor who can price scope quickly, an inspector who finds deal-breakers fast, and an agent who understands investor comps. For holds, add a property manager and a tax pro.

- Use your inspection period wisely. Order the general inspection first, then add pest and, where relevant, radon testing. Review results promptly so you can negotiate repairs, credits, or price. Keep your deadlines tight enough to stay competitive but long enough to make a smart call.

- Prepare for closing day like a pro. Bring your ID, confirm your Closing Disclosure matches the final paperwork, and have proof of homeowners insurance ready. Verify wire details with your title company over a trusted phone number before you send funds. Finish with a thorough final walk-through so the property you receive matches the contract and any agreed repairs.

- Keep liquidity. Whether you are flipping or holding, a cash reserve keeps you flexible if a repair runs over budget or a unit sits vacant longer than expected.

So, What Should You Do?

There is no universal play here. If you have renovation experience, a dependable crew, and the appetite for hands-on work, a well-bought flip can deliver quick profits. If you prefer steadier growth and less project volatility, a long-term hold can build wealth through cash flow and time in the market. Many investors blend both approaches by flipping to generate capital and then rolling profits into solid long-term rentals.

Whichever path you choose, let your neighborhood data, your financing terms, and a disciplined closing and inspection plan drive the decision. That combination gives you the best odds of walking out of closing confident—and set up for the results you want.