As a Dallas real estate investor, your portfolio is likely anchored in physical properties across thriving neighborhoods like Uptown, Highland Park, or Deep Ellum. While these assets offer excellent long-term yields, they are inherently illiquid. To balance this, many property investors are turning to more liquid instruments for diversification and hedging. After-hours CFD trading is a popular strategy used by traders and investors seeking flexibility and faster reactions to market-moving events. For CFD traders, this strategy presents unique market opportunities to capitalize on price movements before the market reacts.

However, these opportunities come with notable risks. Reduced liquidity, wider spreads, and increased volatility can significantly impact trade execution and your overall profitability. Knowing the pros and cons is essential if you plan to try after-hours CFD trading.

Here, we discuss the key benefits and risks associated with after-hours trading on CFDs, helping you navigate this dynamic but often misunderstood strategy and how it applies to your broader investment goals.

What Is After-Hours Trading on CFDs?

After-hours CFD trading allows traders to speculate on price movements outside regular trading hours. The traditional stock and commodities markets have fixed opening and closing times. However, some CFD brokers extend trading hours to cover pre-market and post-market periods.

Can you trade CFDs during after-hours trading? Yes, you can. During those hours, CFD market prices are derived from a combination of global market activity, futures markets, and broker liquidity providers. However, the market conditions are different, and liquidity is often lower.

For property investors, this means you can trade CFDs on Real Estate Investment Trusts (REITs) or shares of major national homebuilders operating in Texas, allowing you to stay engaged with the real estate sector even when standard markets are closed.

Key Benefits of After-Hours CFD Trading

After-hours CFD trading offers traders on Weltrade greater flexibility and access to opportunities that occur outside standard market sessions. One of the key benefits is the ability to react immediately to economic news, geopolitical developments, and corporate earnings reports. For example, if the Federal Reserve announces an unexpected interest rate shift late in the day, it will immediately impact mortgage rates and real estate stocks. Instead of waiting for the market to officially open the next morning, Dallas investors get an early head start to adjust their positions.

This strategy also works well for traders living in different time zones or who cannot trade during regular hours due to other commitments. It allows them to participate in the global markets since CFDs track the prices of underlying assets, such as stocks, indices, commodities, and REITs.

Another benefit of after-hours CFD trading is that it can serve as a valuable risk management tool. This allows traders and investors to adjust or hedge positions —such as protecting against a sudden drop in property-related stocks, in response to unexpected developments in the broader financial markets.

Major Risks and Challenges Traders Should Know

While trading CFDs during after-hours sessions offers unique opportunities, it comes with its fair share of risks, most of which are less pronounced during regular market sessions.

One of the major downsides is low liquidity. After-hours trading on CFDs doesn’t attract many traders, leading to low market activity and liquidity levels. This makes it harder to execute orders at desired prices, increasing the likelihood of delays and slippage.

Moreover, it often leads to wider bid-ask spreads, meaning traders may enter and exit positions at less favorable prices, raising overall trading costs.

Another key risk is heightened volatility. Prices can move sharply in response to limited order flow or unexpected news, making markets more unpredictable. While volatility can create opportunities, it can also lead to losses if the prices don’t move in your favor.

The last significant risk of after-hours CFD trading is limited market information and reduced transparency. With fewer participants, it is more challenging to gauge and evaluate true market sentiment. This means traders must employ disciplined risk management when trading CFDs after standard market hours.

The Crescent Office. Image courtesy of crescent.com

Crescent Real Estate has closed a new $241.5 million investment fund to target commercial property deals, leaning heavily into high-end office real estate even as fundraising across private markets remains under pressure.

The Fort Worth based firm’s latest investment vehicle, GP Invitation Fund IV, came in just under its $250 million target, according to the Dallas Business Journal. A federal securities filing shows the fund was structured for a $250 million offering and had reported $207.36 million sold to 43 investors as of Dec. 19, 2025. This suggests the bulk of the capital was in place heading into year-end, as regulatory disclosures often lag behind final closes.

The timing is significant. Global private equity fundraising fell for a third straight year in 2025, sliding 12.7% to $480.29 billion from $551.16 billion in 2024, according to S&P Global Market Intelligence. Additionally, fewer funds launched in 2025 than the year prior.

A concentrated bet on “flight towards quality” assets

While Crescent’s mandate is broad which involves spanning office, hospitality, and multifamily sectors, its recent moves show where it sees the clearest upside being trophy office space in prime submarkets.

The firm reports a portfolio totaling more than $16 billion in investments, including 67 million square feet of office space, 10,100 multifamily units, and 9,300 hotel keys with these figures based on its existing portfolio as of February 2025.

That scale is now being deployed within a very specific geography

In Uptown Dallas, Crescent has been snapping up marquee office towers. In late 2025, the company bought the 19 story office building at 2100 McKinney Avenue which is an Uptown property with prominent CBRE signage acquired using $170.4 million in financing, according to The Real Deal’s review of deed records. The deal closed Dec. 17.

A few months earlier, Crescent acquired Texas Capital Center at 2000 McKinney Avenue representing one of the biggest office trades in the Dallas and Fort Worth market in 2025. The 21 story, roughly 457,000 square foot tower is anchored by Texas Capital Bank, which has a lease running through 2040.

Fort Worth is becoming a new office hub taking shape as Crescent is also building at home, where in April 2025, the firm broke ground on “Crescent Offices West,” a 170,000-square-foot office building at its Fort Worth campus that it says will be anchored by JPMorganChase and open in 2027.

That project isn’t just a real estate play because it’s part of a broader shift in how business districts form in fast growing Sun Belt metros. When a major employer anchors a high-end building outside a traditional downtown core, it acts as a magnet for other tenants, restaurants, and services.

For city leaders, that’s a win if it expands the tax base however it also raises hard questions about what happens to older office stock and legacy central business districts.

The policy backdrop: interest rates, downtown strategy, and what comes next

Here’s the bigger picture noting that commercial real estate doesn’t move in a vacuum. The Federal Reserve’s pandemic era low rate environment helped fuel dealmaking and fundraising, and the higher rate era that followed has reshaped the math by compressing values, tightening lending, and making investors far pickier.

That’s where public policy quietly enters the story as follows.

Monetary policy sets the cost of capital. Higher rates don’t just slow transactions but they also create market dislocation thereby offering windows where well capitalized buyers can negotiate better pricing especially on assets that still have strong tenants and long leases.

Local policy determines whether downtowns rebound or stagnate. Cities can influence office outcomes through zoning flexibility, permitting speed, transit access, and incentives for conversions of obsolete buildings. If capital flows mainly to “best in class” properties in prime districts, the policy challenge becomes managing the obsolete inventory meaning aging buildings that can no longer compete on amenities, efficiency, or location.

Economic development becomes a tug of war. Fort Worth and Dallas like many large metros are competing submarkets inside one regional economy. When investment and leasing momentum cluster in specific nodes such as Uptown Dallas or the Cultural District area in Fort Worth then public sector decisions around infrastructure and placemaking can accelerate that clustering.

None of that guarantees Crescent’s strategy will pay off. But it explains why a firm can be bullish on trophy office while much of the broader office market still looks shaky since the office sector is increasingly bifurcated meaning it is split between premium buildings with strong tenancy prospects, and everything else.

For Crescent, Fund IV signals that its investors believe this divergence is real furthermore that the firm can keep finding deals on the right side of it.

2026 is shaping up to be an interesting year for home financing. After several years of rate volatility and tight housing supply, the mortgage market is settling into a more stable and flexible phase. Whether you’re a first-time homebuyer, a real estate investor, or a self-employed borrower, understanding where the market is headed can help you make smarter, more confident decisions.

As lending guidelines continue to evolve, today’s borrowers have more paths to homeownership and investment than ever before. Let’s break down what’s changing and what it means for you.

Interest Rates Stabilize, But Don’t Expect 3% Again

One of the biggest questions for homebuyers is where mortgage rates are headed. The good news: after years of volatility, 2026 interest rates are expected to stabilize. Most forecasts expect 30-year fixed rates will sit in the mid-5% to mid-6% range, hovering around 6% for much of the year. If inflation continues to cool, small dips are possible, but don’t expect dramatic swings like we saw after 2020.

That said, the ultra-low 3% rates from the pandemic era are not expected to return. Those historic lows were driven by emergency economic policies that are no longer in place. Instead, experts agree we’ve entered a “new normal” of slightly higher, but more predictable, mortgage rates.

So what does a stable 6% rate mean in real life? Predictability. Buyers can budget with more confidence, investors can better forecast rental cash flow, and self-employed borrowers can plan purchases or refinances without worrying about sudden rate spikes.

While 6% isn’t cheap, it’s historically average. The takeaway for 2026: focus less on waiting for the perfect rate and more on building a smart loan strategy that works in today’s market.

Evolving Borrower Profiles and Needs

Another major trend in 2026 is a shift in who is borrowing and how they qualify. Today’s mortgage borrowers are no longer limited to traditional W-2 employees with simple tax returns. The rise of the gig economy, entrepreneurship, and real estate investing means more people earn income in nontraditional ways. In response, lenders are expanding underwriting guidelines and finding new ways to approve qualified borrowers who may not fit the old lending mold.

Several borrower groups stand out in 2026:

First-time homebuyers

First-time homebuyers remain a core part of the market but face affordability challenges due to higher home prices. With rates stabilizing, many are focused on saving for down payments, exploring low down payment loan options, using seller concessions, or choosing adjustable-rate mortgages to keep monthly payments manageable. Slower home price growth may help ease some of the pressure.

Real estate investors

Real estate investors continue to stay active, supported by more predictable interest rates. Stable financing makes it easier to plan purchases, manage risk, and forecast rental income. Many investors are turning to loans that qualify based on property cash flow rather than personal income.

Self-employed borrowers

Self-employed borrowers are a growing segment, often earning strong income but showing lower taxable earnings due to business deductions. Alternative qualification methods such as bank statement loans and non-QM mortgages are becoming more common and accessible.

Overall, the 2026 mortgage landscape is more flexible and better aligned with how people actually earn and invest today.

Flexibility in Underwriting and Alternative Qualification Methods

A key trend in 2026 is flexibility in how loans are underwritten and documented. Traditional mortgages rely on W-2s, tax returns, and strict formulas, but many borrowers today don’t fit that mold. Non-QM loans and alternative qualification methods are growing, allowing lenders to consider bank statements, cash flow from rental properties, or assets in place of traditional income.

Even niche options like stated-income loans exist for qualified borrowers. These programs may carry slightly higher rates but open the door for self-employed professionals, investors, and others to secure financing. Flexibility and loan structure are becoming more important than chasing the lowest rate.

Other Mortgage Trends to Watch in 2026

Homeowners Tap Into Equity Instead of Moving

Record-breaking home equity is giving homeowners more options than ever. Many who locked in historically low mortgage rates during the pandemic feel “stuck” and are hesitant to refinance or sell. Instead, they are leveraging home equity through loans or HELOCs to fund renovations, consolidate debt, or even finance investment property down payments. Using existing equity allows homeowners to improve their property or access cash without losing their low-rate first mortgage. With inventories still tight and affordability a challenge, tapping equity is becoming one of the smartest financial moves for 2026.

Digital HELOCs Simplify Access to Funds

Technology is making it easier to access home equity. Digital HELOCs allow homeowners to apply online, get approvals in minutes, and draw funds in days rather than weeks. Fintech lenders and forward-thinking banks are creating streamlined, user-friendly platforms with data-driven underwriting and secure portals. This makes the borrowing experience faster, more convenient, and less stressful. Whether it’s for renovations, debt consolidation, or investment purposes, digital HELOCs are changing how homeowners leverage their equity in 2026.

Hybrid STR and DSCR Loans Power Investors

Hybrid short-term rental (STR) loans let borrowers combine personal income with rental income from platforms like Airbnb when qualifying. DSCR loans focus on a property’s cash flow rather than personal income, making it easier for investors to expand their portfolios. These loans simplify qualification and speed up approvals, allowing investors to move on deals confidently even if their personal tax returns don’t fully reflect their income. Hybrid STR and DSCR loans are unlocking opportunities for owner-occupants and investors alike in today’s market.

Home Renovation Loans Are on the Rise

Many homeowners are choosing to stay put and upgrade rather than move. Renovation loans are becoming increasingly popular to fund remodeling, repairs, or luxury upgrades. Options include HELOCs for flexible, ongoing access to funds, FHA 203(k) loans that bundle purchase and renovation costs, and Fannie Mae HomeStyle loans that allow a wider range of improvements for primary, secondary, or investment properties. Renovation financing allows homeowners to increase property value and enjoy their homes without the stress of moving.

More Flexibility for Self-Employed Borrowers

Self-employed borrowers have more options than ever before. Bank statement loans, P&L-only mortgages, DSCR loans, and asset-based mortgages are becoming standard in 2026. Lenders are using AI and digital tools to review bank statements, profit-and-loss reports, and alternative documents efficiently. This streamlines income verification, reduces paperwork, and helps freelancers, entrepreneurs, and gig workers qualify for home financing or investment loans without relying solely on tax returns.

No-Appraisal HELOCs Gain Momentum

No-appraisal HELOCs are becoming mainstream in 2026. Automated Valuation Models, or AVMs, replace in-person appraisals by estimating home value based on real-time market data. This dramatically speeds up access to funds, reduces costs, and allows homeowners to tap equity without refinancing their first mortgage. No-appraisal HELOCs are ideal for renovations, debt consolidation, or unexpected expenses, giving borrowers quick, flexible access to cash while keeping their low-rate mortgage intact.

The Bottom Line: Preparing for Success in 2026

The mortgage landscape in 2026 blends steady rates with innovative loan options. Borrowers of all kinds, including first-time buyers, investors, and self-employed individuals, can benefit by staying informed and open-minded. The era of one-size-fits-all mortgages is fading, replaced by personalized financing strategies.

Homebuyers should focus on what they can control: improving credit, saving, and choosing the right loan program. Stable rates around 6% create predictable opportunities, and options like bank statement loans, down payment assistance, or HELOCs for renovations can help make homeownership achievable.

Real estate investors can grow thoughtfully this year. Cash flow remains critical, and DSCR loans enable purchases where rental income covers expenses. With home price growth leveling off, better deals may be available, especially when working with lenders familiar with investor needs.

Self-employed and non-traditional borrowers have more choices than ever. Non-QM loans and specialty products remove traditional barriers, allowing entrepreneurs and gig workers to qualify on their terms. Expert guidance can help match the right loan to your situation.

In short, 2026 is about balance: stable rates, creative financing, and flexible solutions. The goal isn’t just chasing the lowest rate, it’s finding the mortgage that fits your life, goals, and opportunities this year.

Homeownership in Dallas is more than just having a place to live. For many homeowners, it represents stability, long-term growth, and an opportunity to build financial flexibility over time. As property values in the area continue to rise, more homeowners are discovering that their homes hold more value than they may realize. That value, known as home equity, can sometimes be accessed to help meet major financial goals.

One option that often comes up in these conversations is a cash-out refinance. It can sound complicated at first, but it can be a practical financial tool when used thoughtfully. Understanding when a cash-out refinance makes sense, and when it doesn’t, can help Dallas homeowners make informed decisions that support their long-term plans.

This article breaks down how cash-out refinancing works, why homeowners choose it, and the situations where it may be worth considering. By the end, you’ll have a clearer idea of whether tapping into your home equity aligns with your current needs and future goals.

Understanding Home Equity in the Dallas Market

Home equity is the difference between what your home is worth and what you still owe on your mortgage. In Dallas, steady population growth, a strong job market, and ongoing development have helped push property values upward over time. As a result, many homeowners now have significant equity built into their homes, even if they purchased only a few years ago.

This growing equity is not just a number on paper. It can be a financial resource that, when used responsibly, helps homeowners navigate major life expenses or financial transitions. Equity tends to increase through a combination of rising home values and consistent mortgage payments, both of which have worked in many Dallas homeowners’ favor. However, having equity does not automatically mean you should use it.

The decision to access it depends on timing, personal financial stability, and what you’ll use the money for.

What a Cash-Out Refinance Really Means

A cash-out refinance replaces your existing mortgage with a new one for a higher amount than you currently owe. The difference between the two loan amounts is paid to you in cash at closing. You then repay the new loan over time, typically with a new interest rate and term. Unlike a home equity loan or line of credit, a cash-out refinance restructures your primary mortgage.

This can be appealing if interest rates are favorable or if your financial goals call for a larger lump sum of cash. However, because you are increasing your loan balance, it is important to weigh both the benefits and the long-term costs. The bottom line is that you are converting a portion of your home’s value into accessible funds. You can then use those funds for a variety of purposes, some more financially sound than others.

Common Reasons Dallas Homeowners Choose Cash-Out Refinancing

Homeowners pursue cash-out refinancing for many reasons, and the right reason often depends on individual circumstances. One of the most common motivations is home improvement. Upgrading kitchens, bathrooms, or outdoor spaces can improve daily living while also increasing property value. Another frequent reason is debt consolidation. High-interest debts such as credit cards or personal loans can sometimes be rolled into a mortgage with a lower interest rate, simplifying payments and potentially reducing monthly expenses.

Some homeowners use the funds to cover major life events, such as education costs, medical expenses, or starting a business. Others may use a cash-out refinance to invest in additional property or strengthen their emergency savings. Before moving forward, many homeowners find it helpful to estimate how much equity they can safely access and how it would affect their monthly payments. This is where planning tools become especially valuable.

At this point, it can help to explore how much home equity you could access and understand the financial impact before committing. A tool like this can provide clarity by showing estimated loan amounts, payment changes, and available cash based on your current equity.

When a Cash-Out Refinance May Be a Smart Move

A cash-out refinance often makes sense when you’ll use the funds for purposes that either improve your financial position or add long-term value. Home improvements that increase resale value or energy efficiency can fall into this category.

When done carefully, these upgrades may help offset the additional debt taken on through refinancing. It can also be a smart option when it meaningfully lowers the interest rate on existing debt. Replacing multiple high-interest obligations with a single mortgage payment can make budgeting easier and reduce financial stress over time.

Additionally, if your current mortgage rate is higher than today’s rates, refinancing may offer an opportunity to secure better terms while also accessing cash. In these situations, homeowners may find that the benefits outweigh the costs, especially if they plan to stay in their home long enough to realize the savings.

Situations Where Caution Is Warranted

Despite its advantages, a cash-out refinance is not always the right choice. Using home equity for short-term spending or non-essential purchases can put long-term financial security at risk. Because your home is used as collateral, increasing your loan balance also increases your responsibility. Another factor to consider is how long you plan to stay in your home.

Refinancing comes with closing costs, and it may take several years to break even. If a move is likely in the near future, the financial benefits may not have time to pay off.

Final Thoughts on Using Home Equity Wisely

For many Dallas homeowners, a cash-out refinance can be a practical way to unlock the value built into their homes. When used thoughtfully, it can support meaningful investments, simplify finances, and provide flexibility during important life moments.

The key is intentional decision-making. Understanding how much equity you have, why you want to use it, and how it affects your long-term financial picture can make all the difference.

By approaching the process with clarity and caution, homeowners can turn equity into opportunity without compromising future stability. As with any significant financial move, the most successful outcomes come from informed choices, realistic expectations, and a clear sense of purpose.

Buying a home is likely the biggest financial decision you will ever make. The excitement of finding your dream property can quickly turn to stress when you realize how complicated the financing process actually is.

Most buyers spend hours researching neighborhoods, school districts, and property features. Yet many spend surprisingly little time understanding their mortgage options. This oversight can cost thousands of dollars over the life of a loan.

Working with the right professionals makes all the difference. A skilled mortgage broker can navigate the lending landscape on your behalf, potentially saving you both money and headaches along the way.

Understanding the Role of a Mortgage Broker

Mortgage brokers act as intermediaries between you and potential lenders. Unlike bank loan officers who can only offer their institution’s products, brokers have access to multiple lenders and loan programs.

This access translates into options. Different lenders specialize in different borrower profiles. Some excel with first-time buyers, others with self-employed individuals, and still others with investment property financing.

A broker’s job is to match your unique situation with the most appropriate lending solution. They evaluate your financial picture, understand your goals, and then shop the market on your behalf.

The relationship works similarly to how a real estate agent represents you in property transactions. You benefit from their expertise, relationships, and market knowledge without having to develop these yourself.

Why More Buyers Are Choosing Brokers

The mortgage industry has grown increasingly complex. New loan products emerge regularly, and qualification requirements vary significantly between lenders.

Trying to navigate this landscape alone is like exploring a foreign city without a map. You might eventually find your destination, but you will waste time and probably miss better routes along the way.

When you work with a Go mortgage broker instead of going directly to a single bank, you gain access to wholesale rates that are often unavailable to individual consumers. Brokers leverage their volume relationships to negotiate better terms.

The time savings alone justify working with a professional. Instead of completing multiple applications and gathering documents repeatedly, you work with one broker who handles distribution to various lenders.

Communication also tends to get a lot easier. A good broker keeps you informed throughout the process, translating industry jargon into plain language and setting realistic expectations.

What to Look for in a Mortgage Professional

Not all brokers offer the same value. Experience matters, but so does specialization and communication style. Finding the right fit requires some homework.

Start by asking about their lender relationships. A broker with access to dozens of lenders offers more options than one working with just a handful. More options generally mean better chances of finding ideal terms for your situation.

Image Source: freepik.com

Inquire about their experience with borrowers like you. First-time buyers have different needs than seasoned investors. Self-employed applicants face unique documentation challenges. You want someone who has successfully navigated situations similar to yours.

Check reviews and ask for references. Past client experiences reveal how brokers handle challenges, communicate during stressful moments, and deliver on their promises.

Transparency about fees should be non-negotiable. Reputable brokers explain exactly how they are compensated and disclose any potential conflicts of interest upfront.

The Importance of Local Market Knowledge

Real estate markets vary dramatically from one area to another. Property values, buyer competition, and lending conditions all differ based on location.

Brokers with strong local presence understand these nuances. They know which lenders perform well in specific markets and which ones tend to cause delays or complications.

This localized expertise extends to relationships with other professionals. You might consider a well-connected Mortgage Broker Hawthorn, for example, would have established connections with local real estate agents, attorneys, and appraisers.

These relationships smooth the transaction process. When professionals know and trust each other, communication flows better and problems get resolved faster.

Local brokers also understand regional economic factors that affect lending decisions. Employment trends, development plans, and market cycles all influence how lenders evaluate properties in specific areas.

Timing Your Mortgage Application

When you apply for financing matters more than most buyers realize. Interest rates fluctuate daily, and your personal financial situation can change quickly.

Getting pre-approved before seriously shopping gives you several advantages. You know exactly what you can afford, sellers take your offers more seriously, and you can move quickly when the right property appears.

Pre-approval also reveals any issues with your credit profile or documentation. Discovering problems early leaves time to address them before they derail a purchase.

Image Source: freepik.com

However, pre-approval letters typically expire after 60 to 90 days. If your home search extends longer, you may need to refresh your approval and potentially lock in different terms.

Work with your broker to develop a timeline that aligns with your search plans. They can advise on rate lock strategies and help you understand market conditions.

Common Mistakes to Avoid

Many homebuyers undermine their own mortgage applications without realizing it. Simple mistakes can delay closings or result in less favorable terms.

Avoid major purchases before closing. That new car or furniture set might seem exciting, but the additional debt affects your qualification ratios. Wait until after closing to make big purchases.

Do not change jobs during the mortgage process unless absolutely necessary. Lenders want to see stable employment history. Even a lateral move to a similar position can complicate verification.

Keep cash deposits traceable. Large deposits that cannot be documented raise red flags for underwriters. If someone gives you money for a down payment, work with your broker to handle it properly.

Stay responsive to document requests. Delays in providing paperwork slow down the entire process. When your broker or lender asks for something, prioritize getting it to them quickly.

Building Long-Term Relationships

The best mortgage professionals think beyond single transactions. They want to help you build wealth through strategic real estate decisions over time.

As your circumstances evolve, your financing needs will change too. Growing families need different homes than young professionals. Investors seek different terms than primary residence buyers.

A broker who understands your long-term goals can advise on refinancing opportunities, investment property financing, and equity strategies. For instance, For instance, working with a mortgage broker East Tamaki could provide ongoing guidance as your portfolio expands.

These relationships also pay dividends through referrals. When friends and family need mortgage help, you can confidently point them toward someone you trust.

Stay in touch with your broker even after closing. Market conditions change, and opportunities to improve your position may arise. A quick annual check-in keeps the relationship going and keeps you informed.

Questions to Ask Before Committing

Before selecting a mortgage professional, conduct thorough interviews. The answers reveal both competence and compatibility.

Ask how they will communicate with you throughout the process. Some buyers prefer frequent updates while others want to hear only about major developments. Make sure styles match.

Inquire about their typical timeline from application to closing. Experienced brokers can provide realistic estimates based on current market conditions and your specific situation.

Request a breakdown of all costs involved. Beyond the interest rate, understand origination fees, discount points, and third-party charges. The lowest rate does not always mean the lowest total cost.

Ask what happens if problems arise. Every transaction hits bumps. How the broker handles challenges reveals their true value.

Making Your Decision

Choosing the right mortgage broker sets the tone for your entire home buying experience. Take this decision seriously, but do not let it paralyze you.

Trust your instincts about communication and professionalism. You will be sharing sensitive financial information and relying on this person during stressful moments. Comfort and confidence matter.

Compare multiple options before committing. Even a brief conversation with two or three brokers helps you get a feel for what good service looks like.

Remember that the cheapest option is not always the best value. Expertise, responsiveness, and problem-solving ability often prove more valuable than small fee differences.

Moving Forward With Confidence

The mortgage process does not have to be overwhelming. With the right professional guidance, it becomes manageable and even educational.

Take time to understand your options before jumping in. Knowledge empowers you to ask better questions and recognize good advice when you hear it.

Your home purchase deserves the same careful attention to financing that you give to choosing the property itself. Both decisions affect your financial future for years to come.

The right broker makes this journey smoother, more successful, and far less stressful. Start your search today and take the first step toward your new home.

Seasonal real estate trends affect when people start shopping for a home or decide to list in Calgary, how quickly homes move, and who has more negotiating room at different times of the year.. If you know what each season tends to bring, it’s easier to pick your timing and set expectations for pricing, showings, and negotiations.

Broad seasonal housing trends can point you in the right direction, but real estate is local. A market that slows in one city may stay competitive in another. Working with a top real estate agent or other trusted housing professional can help you interpret local data and understand how the Calgary real estate market aligns with your plans.

Spring: More Listings and More Buyer Activity

Spring is widely considered the most active season for buying and selling. As more sellers list, more buyers jump back in, and competition often picks up. One national analysis found that existing home sales typically rise by about 45% between the winter low and the peak from April through June, making spring the busiest stretch of the year.

For sellers, spring often means:

Larger buyer pools, including families planning a summer move.

More showings packed into a shorter time frame.

Stronger pricing power when homes are well prepared and priced correctly.

For buyers, spring usually brings tradeoffs:

More options as new listings hit the market.

Heavier competition and quicker decision timelines.

Less room to negotiate on homes priced close to market value.

While these figures reflect broader housing patterns, seasonal behavior in Calgary often follows similar timing, with local inventory, weather, and economic factors shaping the details.

Summer: Busy Closings and Lifestyle-Driven Moves

Summer carries many of the same conditions as spring, but with a stronger focus on timing. Recent research shows that about 29.1% of annual residential property sales happen in the summer, compared with 20.2% in winter. So yes, more deals get done in summer, and buyers often have less time to hesitate.

For sellers, summer can work well because:

Steady foot traffic from buyers who started looking in spring.

Buyers are motivated to close before a new school year or job start.

Longer daylight hours help homes show better in person.

Buyers shopping in summer often notice:

Continued competition, especially in strong school districts.

Limited flexibility on price for well-located or move-in-ready homes.

A clearer sense of neighborhood noise, traffic, and daily activity.

Fall: More Balance and Better Negotiating Conditions

By fall, the market usually cools without fully stalling. Some buyers step back, but those who remain tend to be more serious. While inventory may shrink, the drop in casual shoppers often creates a calmer environment for pricing and negotiation.

For sellers, fall typically brings:

Buyers motivated to close before year-end.

Fewer competing listings than in spring or summer.

Greater pressure to price realistically before winter slows activity.

For buyers, fall can feel more manageable:

Less urgency to rush into decisions.

More flexibility to negotiate on price or closing terms.

A better sense of how the home performs in cooler weather.

Winter: Lower Activity but Strategic Opportunities

Winter is usually the slowest season in residential real estate, but that slowdown can work in favor of prepared buyers and motivated sellers. With fewer listings and fewer showings, the people who are still in the market are often the ones who need to move.

Here’s what you’ll usually see in winter:

Fewer active listings, paired with less buyer competition.

Buyers who tour in poor weather are typically committed.

More willingness from sellers to offer price or term concessions.

Several studies show that sale prices often soften from summer into fall and winter as demand cools, even when list prices do not drop dramatically. For buyers comfortable with winter logistics, that softer pricing can sometimes make up for the smaller pool of available homes.

When Broader Forces Matter More Than the Season

Image Source: shutterstock.com

Seasonality matters, but it’s not the whole story. Economic conditions and day-to-day life factors can change the market faster than the calendar does.

A few things can shift demand quickly:

Interest rates, which can cool demand when they rise or pull buyers back in when they drop.

Local job conditions, including hiring trends, layoffs, and wage growth.

Ongoing inventory shortages that keep competition high year-round in some markets.

Lifestyle shifts, such as remote work, that change when and why people move.

Matching Market Timing To Your Goals

Instead of asking, “What month is best?” start with what you need out of the move.

Different goals tend to line up with different timing strategies:

First-time buyers may benefit from late fall or winter, when competition eases and negotiations feel less rushed.

Investors often focus less on seasonality and more on cash flow, vacancy trends, and financing terms.

Buyers upsizing for family reasons may prefer spring or summer to align with school calendars.

Sellers downsizing can list during stronger seasons, then buy when competition is lighter.

Relocations driven by work usually require flexibility, regardless of the calendar.

Why There Is No Single “Best Time”

Seasonal trends help explain what’s typical, but they do not guarantee outcomes. A well-priced home in a tight market can still attract multiple offers in January, while an overpriced listing may struggle even in peak spring. Local climate, economic conditions, and neighborhood-level supply all shape how the calendar plays out.

What works better than chasing a “perfect month” is doing a quick local reality check:

Review recent sales in your specific area.

Track inventory levels, days on market, and price trends by season.

Match timing decisions to your financial readiness and lifestyle needs.

Stay flexible enough to adjust as conditions change.

Image Source: shutterstock.com

In the end, the best time to buy or sell is less about finding a perfect month and more about understanding how seasonal market patterns interact with your situation. When your budget, timeline, and local market conditions agree with each other, the decision usually gets a lot simpler.

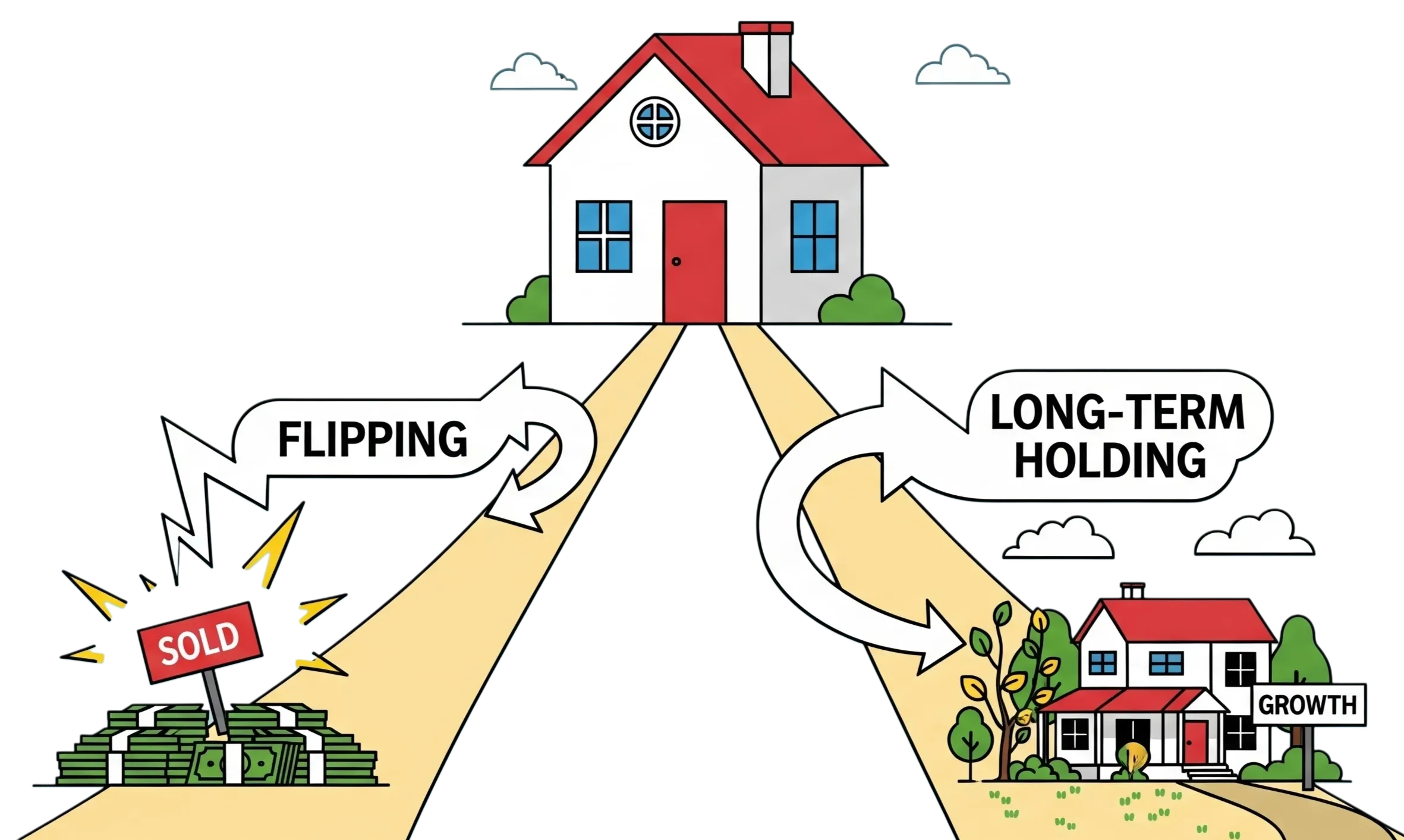

The housing market in the United States and Canada continues to shift with interest rates, local job growth, and supply constraints. If you’re eyeing 2025, the big decision is whether you should flip for quicker profits or hold for steady appreciation and rental income. Both strategies can work. The right call depends on where you buy, how you finance the deal, and how much risk you’re comfortable taking.

This guide provides a practical approach, backed by facts and insights you can apply directly.

The Market Backdrop to Plan Around

You are likely to see a market that is still tight on inventory in many metros, with rates that have eased off peak levels but are not back to the ultra-low era. In the U.S., migration toward affordable, job-rich metros has stayed strong. In Canada, demand remains firm in cities that offer more value than the priciest cores. Think of this moment as a “quality-of-buy” market. The better your entry price, renovation scope, and financing plan, the better your outcome.

Before you choose a lane, narrow your focus to specific neighborhoods. Submarkets inside the same metro can behave very differently. Blocks with new employers, transit improvements, or school upgrades can outperform nearby areas that do not have those catalysts.

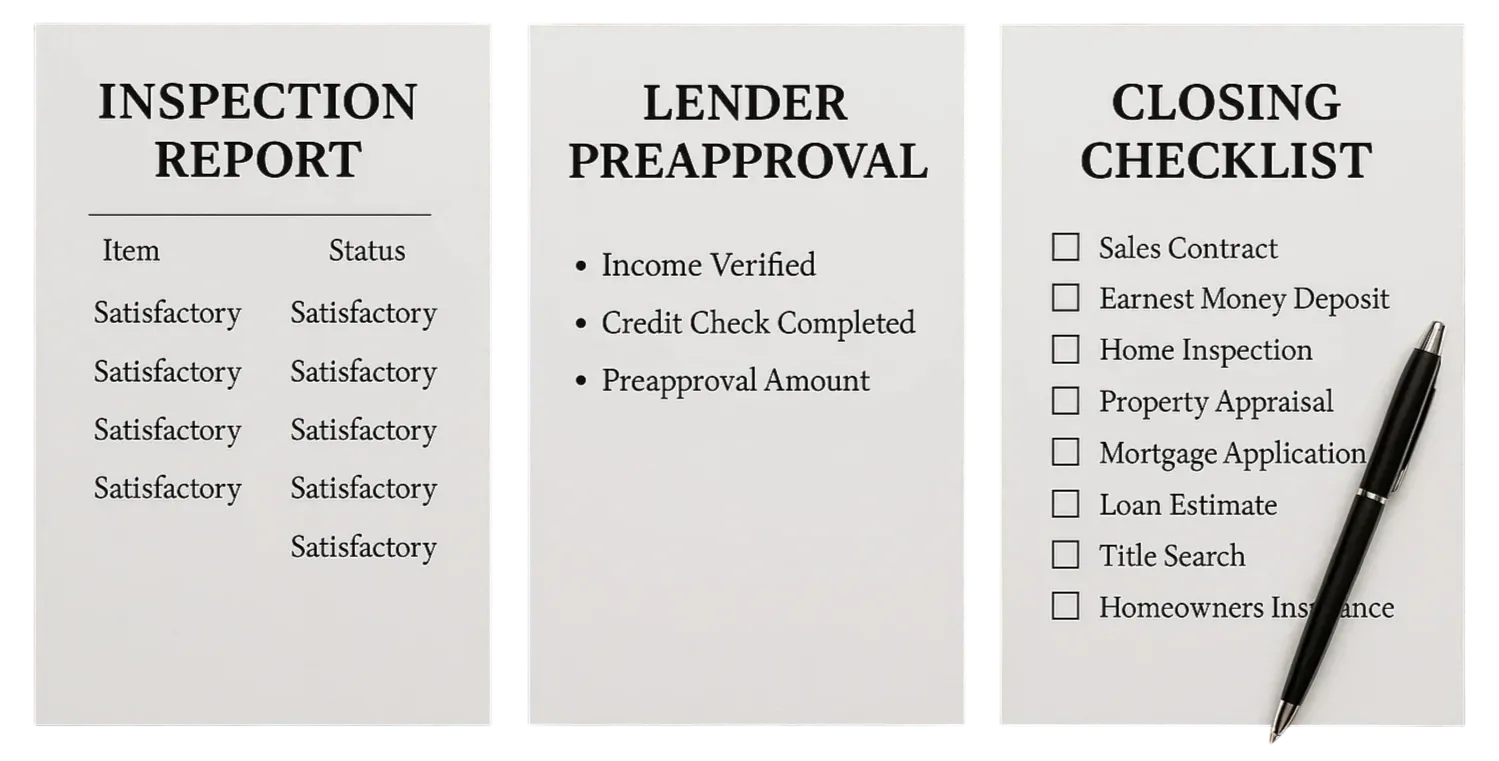

As you evaluate targets, build a closing checklist early. Line up your Closing Disclosure, title documents, and insurance proof so you can move quickly when a good deal appears. That prep work reduces last-minute friction and helps you avoid delays at the table.

Flipping in 2025: Risks, Rewards, and Realities

Flips win when you buy right, keep the renovation tight, and sell into solid demand. It sounds simple enough, yet in 2025 pulling it off will take sharper project management.

Costs and Timing: Material and labor costs remain elevated in many markets, and permit backlogs can push timelines. Build a conservative budget and timeline. Add a 10 to 15 percent cushion for surprises so carrying costs do not eat your spread.

Block-Level Demand: Look for neighborhoods with rising household formation, healthy resale comps, and a clear ceiling price you can hit after improvements. Walk the street at different times of day and talk with property managers and contractors about days on market and buyer must-haves.

What to Renovate: Aim for repairs that unlock buyer confidence and appraisal value. Kitchens, bathrooms, major systems, and curb appeal usually carry more weight than purely cosmetic upgrades.

If you’re writing an offer, protect your downside with a clean inspection playbook. Order a full home inspection right away and be ready to negotiate repairs or credits if issues pop up. Working with a top real estate agent can sharpen your terms and further protect you, especially on repair credits, appraisal gaps, and timeline risks.

Image Source: pexels.com

In a competitive situation, you might shorten the inspection window instead of waiving it outright so you still preserve an exit if a major defect appears. Most buyers work within a 7- to 10-day inspection period, and sellers often respond within a few days after that.

Flips can still pencil if you buy with enough spread, control scope, and move decisively. The biggest risks are timeline slippage, change orders, and a softer resale window that stretches your holding costs.

The Long Hold: Build Wealth Through Time, Rent, and Discipline

A long-term hold combines gradual appreciation with rental income that helps cover the mortgage, taxes, insurance, and maintenance. If you prefer steadier returns and less day-to-day project risk, this lane often fits better.

Durable rental demand: Affordability pressures keep many would-be buyers in the rental pool, which supports occupancy and rent growth in the right neighborhoods.

Tax treatment: In the U.S., long-term capital gains rates are generally lower than short-term rates. In Canada, principal residence rules and other planning strategies can reduce taxes when used appropriately. Consult a licensed tax professional to structure ownership appropriately for your situation.

Compounding effects: Each rent check helps amortize your loan while the property can appreciate over time. Renovations you make are less about a quick retail pop and more about reducing future capex and vacancy.

Your operating checklist matters here too. Keep clean records, budget for repairs, and schedule regular inspections so small issues do not become expensive emergencies. When you eventually sell, you will still go through the same closing process buyers face today, including document prep, insurance verification, and a final walk-through that confirms property condition.

Flip Now or Hold Longer: How to Make the Call

Use side-by-side projections so you can compare cash today against total return over time. Here’s a simple way to frame it for a property you can buy at a fair price in a growth corridor.

Flip scenario

Purchase at a discount.

Tight, value-adding renovation.

Clear exit comps within the next few months.

Short-term, higher-rate financing that magnifies carrying costs.

Execution risk is higher, but cash comes back faster.

Hold scenario

Buy in a school district or job node that renters value.

Stabilize with a targeted refresh that reduces repairs over the next five years.

Traditional mortgage that a good rent can help service.

Returns build through cash flow, principal paydown, and appreciation.

Image Source: pexels.com

Run the numbers both ways, then stress-test them with longer days on market, a lower resale price, or a small rate increase. If you cannot absorb a slower sale or a vacant month, the flip may be too tight. If the cash flow barely covers the mortgage at conservative rents, the hold may need a better buy price.

As you negotiate, keep your inspection contingency and timelines front and center so you can exit or renegotiate if a major issue is uncovered. If the inspection reveals structural or safety problems, you can push for repairs, credits, or decide to walk away without risking your earnest money when the contingency is properly drafted and timed.

Practical Steps to Take

Research the submarket, not just the metro. Track sales on the blocks where you plan to buy. Drive the area, talk to neighbors, and note any public works or new retail.

Get your financing buttoned up early. Preapproval shows strength and keeps closing on schedule. Strong files help you avoid last-minute document chases and let you lock a rate within your lender’s timeline.

Build a reliable team. For flips, you want a contractor who can price scope quickly, an inspector who finds deal-breakers fast, and an agent who understands investor comps. For holds, add a property manager and a tax pro.

Use your inspection period wisely. Order the general inspection first, then add pest and, where relevant, radon testing. Review results promptly so you can negotiate repairs, credits, or price. Keep your deadlines tight enough to stay competitive but long enough to make a smart call.

Prepare for closing day like a pro. Bring your ID, confirm your Closing Disclosure matches the final paperwork, and have proof of homeowners insurance ready. Verify wire details with your title company over a trusted phone number before you send funds. Finish with a thorough final walk-through so the property you receive matches the contract and any agreed repairs.

Keep liquidity. Whether you are flipping or holding, a cash reserve keeps you flexible if a repair runs over budget or a unit sits vacant longer than expected.

So, What Should You Do?

There is no universal play here. If you have renovation experience, a dependable crew, and the appetite for hands-on work, a well-bought flip can deliver quick profits. If you prefer steadier growth and less project volatility, a long-term hold can build wealth through cash flow and time in the market. Many investors blend both approaches by flipping to generate capital and then rolling profits into solid long-term rentals.

Whichever path you choose, let your neighborhood data, your financing terms, and a disciplined closing and inspection plan drive the decision. That combination gives you the best odds of walking out of closing confident—and set up for the results you want.

What does it mean for property investors when interest rates are lowered? Investors often wonder how such changes affect their portfolios. If you’re one of them, you’re not alone. Many property owners and prospective buyers are also trying to understand how this affects their strategies and opportunities.

While many investors are asking, “when will interest rates go down?”, there is no certain answer. However, how lower interest rates influence the property market is what will potentially help investors make better choices. Let’s break down key factors.

The Effects of Borrowing Costs

The most immediate result of cutting rates is lower borrowing costs. Investors could have mortgages at comparatively cheaper rates if the interest rates are low and would considerably minimize the monthly payout. This may make financing fresh properties or re-financing active loans a hell lot easier for people.

Lower rates can increase your borrowing power, opening doors to more properties or higher-value investments, thus making real estate more accessible to a larger pool of buyers

Rising Demand in the Market

When borrowing gets cheaper, people dive into the housing market. Low rates, on the other hand, sometimes turn first-time homebuyers into frequent investors. With an increased demand, especially in hot areas, the jump may also push the prices of the property upward.

For homeowners, that could mean a solid boost in their property value if they bought in a growing neighborhood. But for new buyers, it can mean stiffer competition and fewer bargains. Lower mortgage rates can make homes more affordable even with the extra competition.

Impact on Rental Yields

Lower interest rates also have an impact on rental yields: with reduced mortgage payments, this means lower ongoing costs that can increase profit margins coming in from rental income. If rental prices hold, it’s a win for investors.

What’s more, in competitive markets, rents can even go up to increase the possibility of higher yields. Where lower rates have drawn more people into an area, coupled with a strengthening local economy, landlords are in a position where they can charge higher rents to improve overall returns.

Refinancing Opportunities for Investors

One of the biggest advantages to investors regarding rate cuts is refinancing. Being able to refinance at a lower rate can enable investors to decrease their monthly payments, thus freeing up cash for further investments or property improvement.

Other refinancing benefits may include debt consolidation, equity access, and even the change in terms of loans to better suit your financial situation. This will be great for cash flow improvement if you had a high-interest loan that brings it down by refinancing.

Long-Term Market Growth

The interest rate cut has long-term effects on property prices, but those might not directly show up in the current period. There are a variety of ways for investors to see through market trends and strategically time when they buy or sell. Lower interest rates spur economies and boost consumer confidence in the property market. With consumer spending on a rise and unemployment rates reducing, property usually appreciates in value with a long-term return.

Timing Your Investment Decisions

Property investors need to consider rate cuts, whether they’re buying or refinancing. If rates have increased, it’s worth locking in lower rates before further changes occur. That said, there’s no such thing as perfect timing, especially given the volatility of interest rates in the market and the broader economy.