Buying or refinancing property in New Orleans is exciting, but it also brings tight deadlines, piles of documents, and the need to manage multiple parties. A quality title company keeps the entire process on track. They organize the transaction, make sure ownership transfers cleanly, and prevent the surprises that often delay closing.

Most title companies sound similar at first. They all promise smooth closings and clear title, which makes it easy to pick the cheapest option or go with a quick recommendation.

However, the difference between an average company and a great one becomes obvious once you know what to look for. This is especially true in New Orleans, where older properties and quirky title issues make the details matter.

A Closing Team That Communicates Like Pros

One of the clearest signs of a quality title company is how they communicate before problems show up. Getting ahead of issues usually results in a smoother closing. You should understand the next steps, feel comfortable asking questions, and get updates without having to chase anyone down.

A strong title company keeps everyone in the loop without causing confusion. Lenders, agents, attorneys, and buyers all need different information at different times. Handling that back-and-forth smoothly shows real experience.

Do They Explain the Process in a Way You Actually Understand?

A quality title company avoids unnecessary jargon. Real estate already has enough confusing terms. When you ask about a title search, title insurance, or how an issue is resolved, the explanation should be clear and specific to your situation instead of sounding like a scripted response.

This is even more important when timelines are tight. Confusion grows quickly when people feel rushed. A title company that breaks the process into clear steps helps you stay confident so you don’t miss important decisions.

Strong Local Knowledge of New Orleans Real Estate

New Orleans is not a market where one approach works for every deal. A quality title company understands more than just street names. They are familiar with neighborhood quirks, older homes, and local practices that impact timing. That experience often leads to fewer delays and better solutions.

Local knowledge also means knowing how to work efficiently with local lenders, agents, and inspectors. When a title company understands what typically slows deals down, they can stay ahead of issues rather than scrambling at the last minute.

Thorough Title Search and Clear Issue-Spotting

A quality title company focuses on getting you to closing safely, not just quickly. Rushing without accuracy creates headaches later. A strong title search identifies ownership issues, unreleased liens, and recording errors early enough to fix them without panic.

They should also explain their findings in plain English. You need to know what is routine versus what requires action. When it feels like the title company is actively protecting your interests, you are working with the right team.

Transparent Pricing

A quality title company is upfront about costs. Nobody wants to get to the closing table and find fees that were never discussed. You should understand exactly what you are paying for, which fees are standard, and which depend on your specific situation.

Clear pricing also shows respect for your budget. When costs are explained early, you can plan ahead without feeling blindsided.

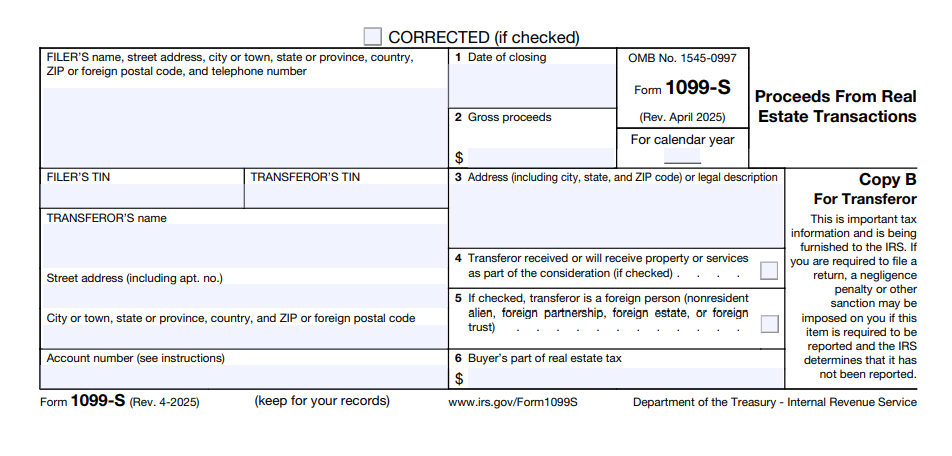

Secure Handling of Funds and Wire Instructions

Security should never feel casual in a real estate transaction. Wire fraud is a real risk when large sums of money are moving around. A quality title company follows strict procedures to verify wire instructions and confirm identities, even if that means repeating steps to stay safe.

Look for a consistent, professional approach. Careless emails or unclear instructions can create opportunities for fraud. Taking security seriously protects everyone involved.

An Organized Closing Experience

Even simple closings benefit from structure. You should know exactly what to bring, what you’ll be signing, and how long the appointment will take.

Organization also shows up in the details, like sending paperwork early and answering questions before closing day. When a closing feels calm, it is usually the result of strong preparation.

Do They Coordinate Smoothly With Lenders and Agents?

A quality title company keeps communication organized. Closings often stall when information breaks down. A strong title team keeps lender requirements and document timing aligned.

If your lender or agent speaks highly of a title company, take note. Professionals remember who makes their work easier. You want more than a closing date. You want a closing that happens without unnecessary friction.

Handling Issues When They Arise

Many transactions hit a bump in the road. This might involve a missing document, a payoff issue, or a timeline conflict. What matters most is how the title company responds.

A quality team stays calm and focuses on solutions. They know when an issue requires extra documentation versus a simple fix. A steady approach helps prevent the stress that makes closings feel overwhelming.

A Reputation You Can Trust

Strong title companies build their reputations through consistency. Look for patterns in feedback about responsiveness and organization. It is worth noticing whether a company is known for reliability in a market where timing matters.

Professionalism also means setting realistic expectations. The best companies avoid empty promises. Instead, they explain potential delays clearly and work hard to deliver results.

Choosing the Right Team

When comparing options, focus less on marketing and more on the daily habits that signal quality. The right title company keeps your transaction organized, secure, and moving forward. Clear communication, local experience, and transparent pricing help protect your investment.

If a title company in New Orleans feels responsive and thorough from the first conversation, that usually carries through to closing. A smooth closing is rarely luck. With the right team, it becomes the standard