Hua Hin has long been a beloved seaside escape for Thai royalty and Bangkok elites, but in recent years, it has transformed into a major player on the global stage. It’s no longer just a quiet weekend getaway. Today, it is a growing real estate market with real upside.

Momentum is building as infrastructure projects get closer to the finish line and overseas interest keeps rising. If you’re considering buying, timing matters, particularly before the next wave of demand is fully reflected in prices.

Between lifestyle appeal, government incentives, and active development, Hua Hin is entering a period where buying sooner can make a meaningful difference.

Market Trends: Consistent Growth Without the Hype

The property market in Hua Hin has shown resilience and consistent growth, without the dramatic price swings seen in some other areas. Over the past year, prices have risen around 3–7%, and many expect that pace to continue through next year.

Some segments are performing even better. Since 2020, luxury condos and beachfront homes have posted gains of up to 35%, driven by growing demand for premium, lifestyle-focused homes.

Absorption rates also highlight how steady demand is. Seaside condos, in particular, show an absorption rate of 84.6%, which suggests good-quality units are selling quickly. International demand is a major factor as well, with foreign buyer participation reaching 40%.

Even with that, Hua Hin still looks affordable next to bigger-name markets. Average prices sit around THB 87,434 per sqm for apartments and THB 38,932 per sqm for houses, so buyers often get more space and better locations for the same budget than in places like Phuket or Bangkok.

Major Infrastructure Projects That Support Price Growth

One of the clearest drivers of future price growth is infrastructure, and Hua Hin is seeing major government investment. These upgrades should make the city easier to reach, more practical for frequent Bangkok travel, and more attractive for international visitors.

Airport Expansion

The Hua Hin Airport is currently undergoing a THB 300 million upgrade. This is not just a cosmetic update. The project includes a runway expansion designed to accommodate larger aircraft.

The airport is scheduled to resume full-scale international flights by April. Better air access from regional hubs can increase tourist traffic and raise demand for property for sale in Hua Hin, something that has happened in other destinations after similar upgrades.

Highway and Rail Improvements

Connectivity is improving fast. The Highway 37 expansion, a project valued at 7 billion baht, is adding lanes, interchanges, and U-turns to reduce congestion. Scheduled for completion in late 2026, this should improve traffic flow around the city and make everyday travel easier.

In addition, Phase 1 of the Bangkok to Hua Hin high-speed rail is progressing toward a planned 2032 completion.

Tourism and Lifestyle Appeal

Real estate markets do well when a location stays active and keeps attracting new people. Thailand is targeting 36–39 million visitors in 2025, and Hua Hin is well placed to benefit from that broader growth. The city is also evolving beyond its older image as a quiet retirement base, appealing more to families, remote workers, and long-stay visitors.

You can see that shift in new hospitality projects. Major brands are expanding in the area, including high-end hotels like the NH Hua Hin, expected to open in 2026. Developments like this usually reflect long-term confidence in the destination.

Beyond tourism, everyday comfort plays a big role in demand. Hua Hin has an expat-friendly atmosphere, supported by strong amenities such as international schools, JCI-accredited hospitals, and well-known golf courses. That mix attracts retirees, digital nomads, and families looking for Hua Hin property for sale.

This helps create rental demand throughout the year, not only during holiday peaks. With tourism and higher-end amenities supporting demand, local real estate can offer solid investment potential.

Government Incentives and Policies

For buyers who are still deciding, current government policies may reduce costs. To stimulate the real estate sector, the Thai government has cut transfer fees and mortgage registration fees to 0.01% for properties valued up to 7 million baht. These incentives are valid until June 2026, so closing before that deadline can lower transaction costs.

Foreign ownership rules remain relatively clear. Non-Thai nationals can buy a condo in Hua Hin and own the unit freehold (within the foreign quota of 49% of the building’s unit space).

For villas or land, options such as long-term leaseholds or setting up a Thai company structure remain common routes for buyers who want more flexibility.

Investment Opportunities to Watch

Not all properties perform the same way. In Hua Hin, three categories are showing stronger potential based on current demand:

Luxury Condominiums: Given the absorption rates above, sea-view condos remain among the easiest units to resell and rent, with strong appeal to both short-stay and long-stay tenants.

Pool Villas: The post-pandemic preference for privacy and space has kept demand for pool villas strong. Homes with modern layouts and convenient access to international schools tend to be especially attractive to expat families.

Beachfront Homes: Scarcity matters. As beachfront land becomes harder to find, existing properties in prime coastal spots often have the most room for long-term price growth.

Real estate agents in Hua Hin have many great options available. Whether you want to invest in a new property under construction or buy a ready-to-move-in home, there’s something for everyone.

Expert Opinions and Forecasts

Many analysts expect Hua Hin’s fundamentals, including limited supply in prime areas and rising demand, to support annual growth in the 3–7% range through next year.

One point comes up often. Buyers who enter the market before a major upgrade is fully reflected in prices may benefit from better value. With the airport scheduled to reopen to full international service by April 2026, demand is expected to increase as access improves. Buying before that milestone can mean securing a property closer to current price levels, rather than after demand starts pushing prices higher.

Conclusion

Hua Hin is moving into a period where timing and fundamentals line up. With transport upgrades progressing, government incentives still available, and steady price growth, buyers may find better choices and better entry prices by acting sooner rather than later.

Whether you plan to buy a condo in Hua Hin for your own use, rental income, or a relaxed retirement lifestyle, this can be a practical moment to move. And for those who prefer flexibility, the rental market also offers plenty of options, including properties for rent in Hua Hin.

Working with trusted local professionals can help you evaluate locations, avoid common mistakes, and choose a property that fits your long-term plans.

Purchasing high-end real estate is very different from purchasing a standard home. The stakes are higher, systems are more complex, and the expectations are greater. Whether you’re looking for a waterfront villa, a modern smart home, a penthouse with a view, or a spacious private estate, the process requires careful planning. Here is how to find a luxury home that matches your lifestyle and long-term goals.

Define What ‘Luxury’ Means in Your Market

Luxury looks different depending on the location. A high-end home in Dallas will offer very different features from one in New Jersey. Before starting your search, understand what “luxury” typically includes in your target market. Common features include:

Premium materials like marble, quartz, and hardwood

Smart home technology and energy-efficient systems

Large square footage or open layouts

Resort-style outdoor areas

Secure gated entrances

Top-tier school districts or exclusive neighborhoods

Knowing the market helps you spot genuine value instead of paying for features that don’t justify the price.

Study the Market Before Making Any Decisions

Luxury real estate operates differently from the general market. Inventory can shift quickly, and certain areas stay competitive year-round. You need to track recent sales, pricing trends, and upcoming developments.

Since you are targeting New Jersey, working with a real estate agent in Essex County, NJ can give you access to off-market homes, neighborhood insights, and proper pricing guidance.

The more you know about current demand, the better prepared you’ll be when the right property becomes available.

Get Your Financials Organized Early

Luxury homes often come with stricter lending requirements. Even all-cash buyers benefit from organizing documentation early, since high-value transactions tend to involve more verification. Prepare ahead by:

Checking your credit health

Reviewing recent tax returns

Gathering proof of income

Getting pre-approved for a jumbo loan, if needed

Speaking with lenders who handle high-value properties

Being financially ready puts you in a stronger negotiating position and speeds up the offer process.

Focus on Long-Term Value

Not every expensive property will hold its value. When buying luxury real estate, the lifestyle and long-term potential matter just as much as the home’s features. Ask yourself:

Is the area stable and in demand?

Are the schools strong, even if you don’t need them?

Is the neighborhood improving or declining?

Will the home’s style stay appealing over time?

Is the location convenient for your lifestyle?

A luxury home in a strong area is far more likely to appreciate.

Inspect Craftsmanship Closely

A luxury home should feel solid, well-built, and thoughtfully finished. Stunning photos can hide rushed workmanship, so take your time during walk-throughs. Pay attention to:

Cabinet quality and hardware

Flooring transitions

Window construction and seals

Finish consistency

Water pressure and plumbing

Insulation and noise control

If something feels cheaply done, it often signals deeper issues.

Use an Inspector Experienced With Luxury Homes

Not every inspector understands how to evaluate high-end features, and luxury homes often include advanced systems that require specialized knowledge. An experienced inspector will know how to assess:

Smart home automation

High-end kitchen appliances

Spa features, steam rooms, or saunas

Custom HVAC setups

Wine storage

Pools, outdoor kitchens, and terraces

The right inspector can protect you from expensive surprises later.

You Have to Be Patient

Luxury home buying isn’t usually a quick process. Inventory is lower, and the perfect property might take time to hit the market. Rushing into a property you’re unsure about often leads to regret. Patience helps you wait for:

The right location

A layout that truly fits your lifestyle

A property with long-term value

A price that aligns with the market

In the luxury tier, patience pays off.

Think About How You Actually Live

luxury home should feel effortless, not overwhelming. Focus on the lifestyle you want rather than just size or features. For example:

If you entertain often, focus on kitchens and outdoor spaces.

If you work from home, prioritize office space and privacy.

If you value peace, choose a quieter neighborhood over a busier one.

If convenience matters, consider proximity to key amenities.

Luxury should make your daily life easier, not more complicated.

Having the Purchase in Mind, But Not Rushing it

Buying a luxury property is exciting, but it requires preparation, patience, and a clear understanding of what you want. With the right research, professional support, and attention to detail, you can find a home that feels both impressive and practical for your lifestyle.

Selling a home as-is can feel intimidating, but for many Inland Empire and Los Angeles sellers it’s the most practical move when you’re short on time, cash, or energy for repairs.

Once you know what “as-is” actually means, and how it plays out in Riverside and San Bernardino, you can make clearer decisions and keep things moving.

1. What Does Selling a Home “As-Is” Mean?

You’re listing the home in its current condition, with no agreement to make repairs, upgrades, or improvements before selling. Buyers can still schedule inspections and ask for concessions, and you’re free to say no and keep it simple.

In California, an as-is sale doesn’t erase your disclosure duties, so you still complete the Transfer Disclosure Statement (TDS) and the Natural Hazard Disclosure (NHD), and if you qualify for a limited exemption like an inherited property, you still disclose what you know and provide required reports.

If the buyer is using FHA or VA financing, the appraiser may call out health- or safety-related repairs that must be addressed to close, which can affect timing and pricing even in an as-is deal.

This setup draws buyers who will trade price for sweat equity, and it often fits cash buyers who prefer a quick close.

2. Why Some Sellers Choose an “As-Is” Sale

People sell as-is when the home needs major work they can’t take on, when they’re relocating on a tight timeline, when life gets busy, or when they inherit a property they don’t plan to keep. It’s also common when sellers don’t want to front repair cash, when they’re aiming for a quick cash offer, or when the home’s condition could trip FHA/VA repair calls that slow financing.

Selling as-is skips contractor scheduling and long timelines, so you can focus on your next move instead of managing a punch list.

3. Set Realistic Expectations

Price the home with its current condition in mind, because buyers will bake repair costs and risk into their offers.

You’re trading some top-end value for speed and certainty, which can still pencil out once you skip renovation spend and months of carrying costs (mortgage/interest, taxes, insurance, utilities).

If you need a quick sale, price competitively off recent Inland Empire comps and adjust for condition, location, and lot, and lean on a local agent for a data-backed range. Expect inspections and negotiation even in an as-is deal, and remember financing can still trigger repair calls (FHA/VA) or condition adjustments on the appraisal.

Local pulse check: typical days on market in Riverside County were about 59 days in September 2025, so sharper pricing usually matters more than polish.

Market reality: even in as-is sales, seller concessions have been common lately (rate buydowns, closing-cost help), so plan your net with a little cushion.

4. How Cash Home Buyers Fit In

Cash buyers use their own funds, so they can often close in about one to two weeks with fewer contingencies, which helps when you need a sure thing.

They’ll buy in almost any condition and handle most logistics, but that convenience is priced in—cash offers are typically lower than financed offers (investor offers can be much lower).

If speed and certainty matter most, collect a few offers and verify proof of funds before you sign; you can also check BBB records and reviews to vet a buyer.

5. The Selling Process, Step by Step

Start by gathering key details (year built, permits, recent upgrades), taking clear, well-lit photos, and writing a straight-ahead description that matches the home’s condition. Buyers will schedule a walkthrough and usually still order inspections—even with cash—so everyone avoids surprises.

After the visit, you’ll receive an offer that reflects the market plus likely repair costs, and you can accept, counter, or pass. Once you sign, open escrow with a local title company, pick a closing date, deliver your required disclosures (TDS/NHD), and let escrow coordinate title, payoff, and recording; you collect funds at closing after everything clears.

In California, plan for safety basics like working smoke alarms, carbon-monoxide detectors, and a properly strapped water heater—items that often show up as lender/appraiser checkpoints even in an as-is sale.

6. Benefits of Selling As-Is

Save time because you skip most pre-sale repairs and heavy staging, avoid permit/contractor delays, and if you take a cash offer, you can often close in about 7–14 days.

Save money because you avoid up-front fixes and big staging bills, and you’re not paying extra months of carrying costs like mortgage/interest, taxes, insurance, and utilities while the home sits on the market.

Cut stress with a simpler path to a firm close and fewer lender steps, no required appraisal with an all-cash deal, and fewer appraisal-triggered repair calls (common with FHA/VA financing). That clarity helps during divorce, inheritance, pre-foreclosure, or a job transfer.

7. What to Watch Out For

Work only with buyers who are transparent, ask for proof of funds or lender preapproval up front, and don’t pay any up-front “buyer” or “processing” fees. Verify wire instructions by phone with your title/escrow contact, because wire fraud is rampant.

Read every agreement and consider a California real-estate attorney or a seasoned agent, especially for occupancy/rent-back terms (seller staying after close) and get the deposit, daily rate, and move-out date in writing. Lenders may limit rent-backs to ~60 days before they treat the purchase as non-owner-occupied.

Be honest on disclosures, because hiding known issues can lead to post-closing claims. In California you still owe TDS/NHD even “as-is,” and failure to disclose can create liability.

Confirm earnest money amount, timelines, and contingency-removal dates in writing. Once contingencies are removed, a buyer who walks can forfeit the deposit, so track those dates closely. Also, watch for clauses that reopen repairs after you agreed to sell as-is.

Watch assignment language. If the buyer is an investor or “and/or assigns,” understand whether they can assign the contract to someone else and on what terms (and whether you must consent).

Call out special liens or contracts early (e.g., PACE assessments or leased solar) because they often must be disclosed, transferred, or paid off at closing, and they can derail financing if missed.

8. Final Tips for Success

Tidy up, declutter, and knock out easy wins like yard cleanup or touch-up paint, then get bright, well-lit photos. Small upgrades help first impressions and listing photos land better.

Be straight about condition and spotlight real perks like a big lot, mountain views, freeway access, or ADU potential. All strong draws in the Inland Empire.

Compare multiple offers when you can and weigh net proceeds, timeline, and certainty—not just the sticker price, so you pick what actually works for you. Look at contingencies, rent-backs, and any credits that change your bottom line.

Conclusion

Selling as-is doesn’t have to be complicated, and it’s often the cleanest path when you want a smooth exit. If you’re thinking, “I need to sell my house fast,” consider reaching out to cash buyers and a trusted local agent, line up your disclosures, and pick the offer that balances price with certainty so you can move on with confidence.

For centuries, Greece has captured people’s attention with its ancient history, hospitable climate and friendly culture. In recent years, it has also captured the attention of international property buyers.

Greece’s luxury real estate market has gone from quiet to seriously interesting. What used to be a small niche has turned into one of Europe’s most talked-about investment scenes. And it’s easy to see why. Maybe it’s a villa tucked into a cliff above the Aegean, a sleek penthouse in Athens, or a beachfront hideaway on Corfu. Either way, you’re getting a lifestyle that blends beauty, value, and long-term potential in a way few places can match.

Image Source: fusion-consultancy.net

If you’re considering purchasing a luxury home in Greece, here are some important insights you should know before taking the plunge.

Why Greece Appeals to Luxury Buyers

Greece combines lifestyle appeal with a steadily improving economic environment. The Mediterranean climate, relaxed pace of life, and spectacular natural beauty have always been attractive to international buyers, but new factors are also driving demand:

Lifestyle and culture: Whether island-hopping in the Cyclades or fine dining in Athens, Greece offers a year-round luxury lifestyle that blends modern comfort with cultural depth.

Value for money: Compared with other European hot spots like the French Riviera, Mallorca, or Italy’s Amalfi Coast, luxury properties in Greece tend to be more affordable on a per square meter basis.

Economic recovery: After years of financial uncertainty, Greece’s economy and property market are stabilizing, which in turn is boosting buyer confidence.

Accessibility: Most major cities and islands in Greece are well-connected to international airports, making them a great choice for frequent travelers.

Prime Locations for Luxury Homes

While many people know Greece for its glamorous islands, there’s much more to explore.

Athens: The capital city has been undergoing a significant real estate boom in recent years—thanks in part to the Ellinikon project, one of the largest urban developments in Europe. Neighborhoods like Voula and Glyfada, near the Athens Riviera, attract buyers who want city living combined with spectacular sea and mountain views.

The Aegean Islands: Islands like Mykonos and Santorini are globally recognized luxury destinations. Their whitewashed villas with infinity pools and cliffside views drive strong rental demand.

Crete and Corfu: For buyers seeking space and privacy, these islands provide larger estates at more accessible price points, plus rich cultural heritage and true year-round communities.

There are also many lesser-known islands and areas in pristine natural settings that offer luxury living at more affordable prices.

Each location has its own unique character and caters to different preferences: nightlife, city lifestyle, exclusivity, or serenity.

Foreign ownership: Both EU and non-EU citizens can purchase property in most of Greece. Some border areas need extra permits, but the popular luxury spots generally do not.

Golden Visa program: This is one of Greece’s big draws. Until recently, a €250,000 property was enough for a residency permit. Rules changed in 2024: in many prime areas like Athens, Mykonos, and Santorini, the minimum is €800,000; in other regions, it’s €400,000. The €250,000 option still exists, but only under specific conditions—for example, renovating an older property or converting a commercial building into residential. Always confirm the latest details with an expert before assuming eligibility.

Buying costs: Beyond the purchase price, set aside 5–8% for taxes and fees, typically including the ~3% transfer tax, plus notary and legal costs.

VAT: New-builds in Greece normally carry 24% VAT. But this tax has been suspended until the end of 2026, so many buyers currently only pay the ~3% transfer tax.

Understanding these basics helps avoid surprises during the buying process.

Market Trends and Opportunities

Design and sustainability: It’s increasingly standard for luxury homes to include solar panels, smart systems, and higher energy efficiency. That combination lifts property value and improves day-to-day living. With AI-enabled home tech advancing quickly, adoption is speeding up.

Short-term rentals: Many investors rent out their villas or apartments, making high-value properties both a great place to live and an investment opportunity. That said, Greece has tightened rules in some areas, especially Athens. You’ll see caps and extra taxes in certain zones, so check the specifics with a qualified advisor.

Rising international interest: Investors from the US, Middle East, and Asia are joining Europeans in viewing Greece as both a lifestyle and financial opportunity. This broadening buyer base supports stable future demand.

Image Source: fusion-consultancy.net

Tips for Navigating the Buying Process

Get local expertise. The Greek market is fragmented. A specialist who knows the luxury segment can save you time and help you avoid pitfalls. For instance, Fusion Consultancy helps international buyers find high-end homes and navigate the legal and practical steps.

Conduct legal due diligence. hire a local lawyer early to review title, check for debts, and confirm zoning. This is a crucial step to protect your investment.

Define your long-term goals. Is this mainly a holiday home, a rental investment, or a Golden Visa property? Your answer will shape what and where you should buy. If you’re buying for personal use, imagine daily life there. Is the area well connected? Are there international schools and hospitals nearby? It’s not only about the numbers. Consider the experiences the property will offer..

Think about access. Some islands are easy in summer but tricky off-season. If you want year-round use, consider ferries, flights, and on-the-ground services.

Final Thoughts

Greece’s luxury real estate market is no longer an under-the-radar opportunity. Greece now sits near the top of the Mediterranean wish list, offering real lifestyle upside, a supportive investment backdrop, and approachable entry points, especially heading into 2025. Demand isn’t cooling.

For international buyers, keep the dream in sight but plan like a pro. Enjoy the sunsets; lean on expert help to make the paperwork and closing just as easy.

About the Author

Christina Krik-Bost is a professional whose path brings together business, humanitarian service, and the world of high-end lifestyle industries. Holding a Bachelor in Business Administration and currently pursuing a degree in European Studies in history, literature, and culture, she combines academic curiosity with a strong foundation in strategy, communication, and cultural understanding.

Her early career centered on business and marketing, where she developed the analytical and creative skills to navigate competitive markets. This expertise was further enriched through humanitarian work in emergency locations, where she learned the importance of resilience, adaptability, and empathy. These experiences shaped a professional who not only understands the value of strategy but also the human side of every interaction.

Today, she applies this multifaceted background to luxury real estate, yachting, exclusive travel, and event management. Her marketing knowledge allows her to identify and showcase value, while her humanitarian and academic background bring authenticity and cultural depth to her work. She offers more than professional expertise—she provides a people-first, globally informed approach where precision, vision, and meaningful connection converge.

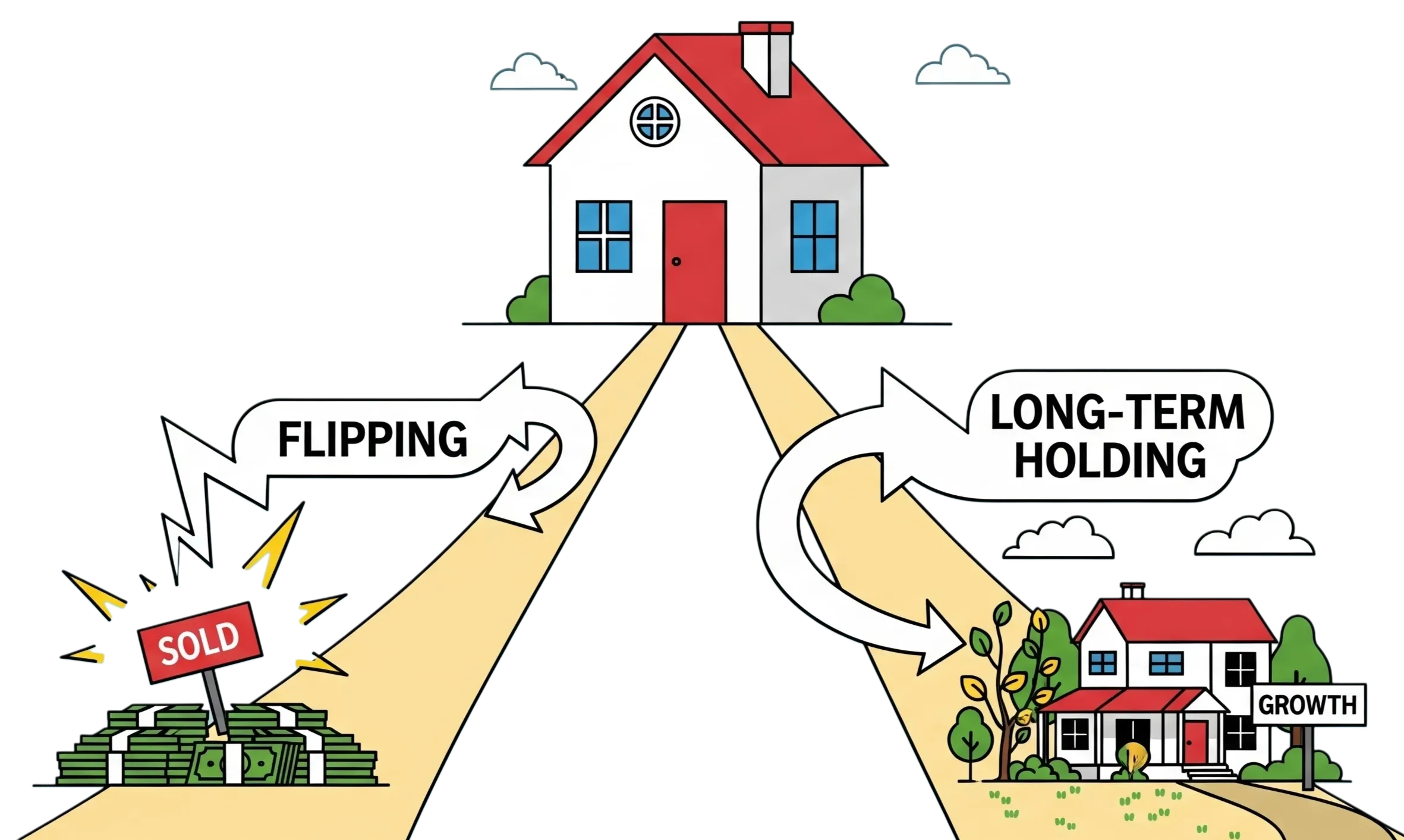

The housing market in the United States and Canada continues to shift with interest rates, local job growth, and supply constraints. If you’re eyeing 2025, the big decision is whether you should flip for quicker profits or hold for steady appreciation and rental income. Both strategies can work. The right call depends on where you buy, how you finance the deal, and how much risk you’re comfortable taking.

This guide provides a practical approach, backed by facts and insights you can apply directly.

The Market Backdrop to Plan Around

You are likely to see a market that is still tight on inventory in many metros, with rates that have eased off peak levels but are not back to the ultra-low era. In the U.S., migration toward affordable, job-rich metros has stayed strong. In Canada, demand remains firm in cities that offer more value than the priciest cores. Think of this moment as a “quality-of-buy” market. The better your entry price, renovation scope, and financing plan, the better your outcome.

Before you choose a lane, narrow your focus to specific neighborhoods. Submarkets inside the same metro can behave very differently. Blocks with new employers, transit improvements, or school upgrades can outperform nearby areas that do not have those catalysts.

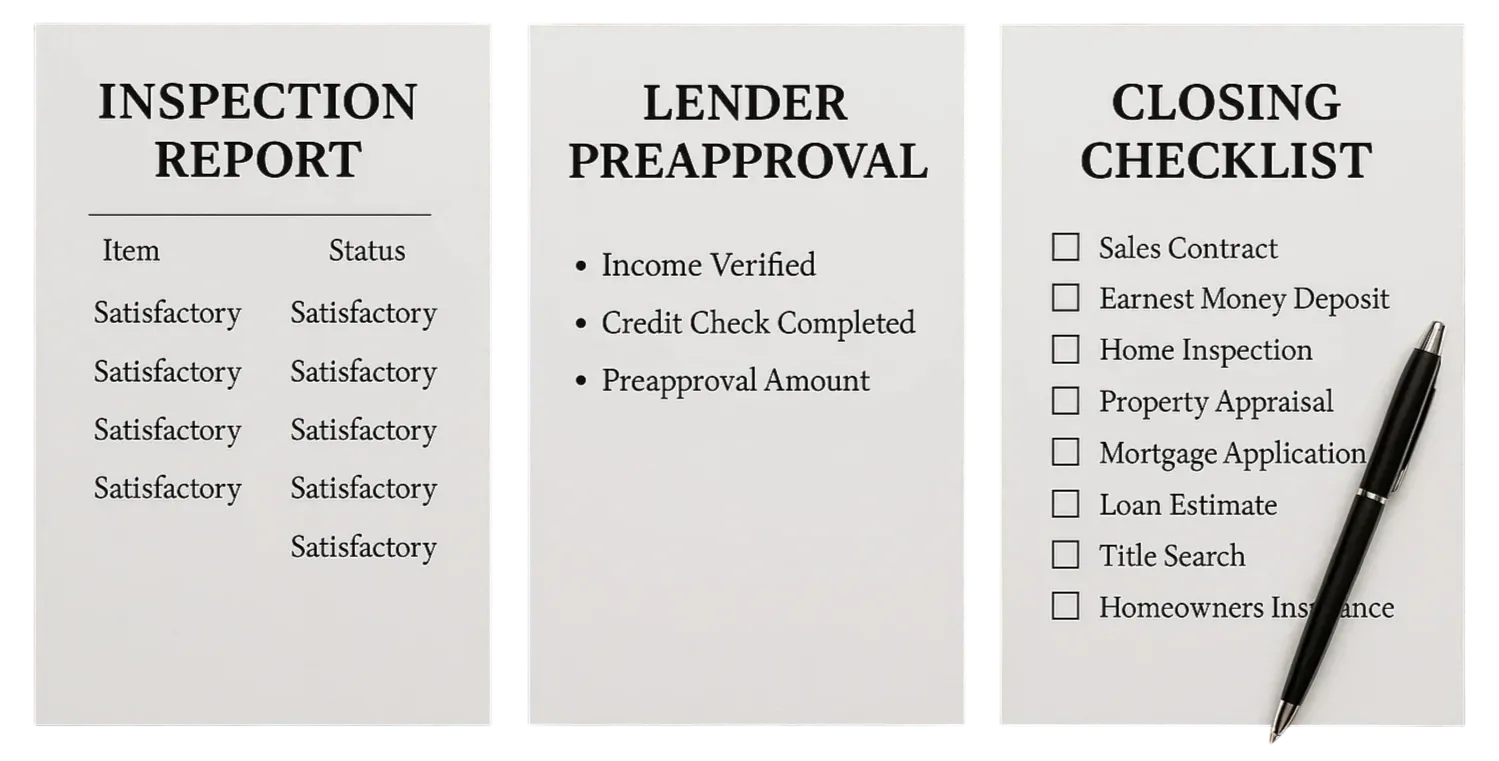

As you evaluate targets, build a closing checklist early. Line up your Closing Disclosure, title documents, and insurance proof so you can move quickly when a good deal appears. That prep work reduces last-minute friction and helps you avoid delays at the table.

Flipping in 2025: Risks, Rewards, and Realities

Flips win when you buy right, keep the renovation tight, and sell into solid demand. It sounds simple enough, yet in 2025 pulling it off will take sharper project management.

Costs and Timing: Material and labor costs remain elevated in many markets, and permit backlogs can push timelines. Build a conservative budget and timeline. Add a 10 to 15 percent cushion for surprises so carrying costs do not eat your spread.

Block-Level Demand: Look for neighborhoods with rising household formation, healthy resale comps, and a clear ceiling price you can hit after improvements. Walk the street at different times of day and talk with property managers and contractors about days on market and buyer must-haves.

What to Renovate: Aim for repairs that unlock buyer confidence and appraisal value. Kitchens, bathrooms, major systems, and curb appeal usually carry more weight than purely cosmetic upgrades.

If you’re writing an offer, protect your downside with a clean inspection playbook. Order a full home inspection right away and be ready to negotiate repairs or credits if issues pop up. Working with a top real estate agent can sharpen your terms and further protect you, especially on repair credits, appraisal gaps, and timeline risks.

Image Source: pexels.com

In a competitive situation, you might shorten the inspection window instead of waiving it outright so you still preserve an exit if a major defect appears. Most buyers work within a 7- to 10-day inspection period, and sellers often respond within a few days after that.

Flips can still pencil if you buy with enough spread, control scope, and move decisively. The biggest risks are timeline slippage, change orders, and a softer resale window that stretches your holding costs.

The Long Hold: Build Wealth Through Time, Rent, and Discipline

A long-term hold combines gradual appreciation with rental income that helps cover the mortgage, taxes, insurance, and maintenance. If you prefer steadier returns and less day-to-day project risk, this lane often fits better.

Durable rental demand: Affordability pressures keep many would-be buyers in the rental pool, which supports occupancy and rent growth in the right neighborhoods.

Tax treatment: In the U.S., long-term capital gains rates are generally lower than short-term rates. In Canada, principal residence rules and other planning strategies can reduce taxes when used appropriately. Consult a licensed tax professional to structure ownership appropriately for your situation.

Compounding effects: Each rent check helps amortize your loan while the property can appreciate over time. Renovations you make are less about a quick retail pop and more about reducing future capex and vacancy.

Your operating checklist matters here too. Keep clean records, budget for repairs, and schedule regular inspections so small issues do not become expensive emergencies. When you eventually sell, you will still go through the same closing process buyers face today, including document prep, insurance verification, and a final walk-through that confirms property condition.

Flip Now or Hold Longer: How to Make the Call

Use side-by-side projections so you can compare cash today against total return over time. Here’s a simple way to frame it for a property you can buy at a fair price in a growth corridor.

Flip scenario

Purchase at a discount.

Tight, value-adding renovation.

Clear exit comps within the next few months.

Short-term, higher-rate financing that magnifies carrying costs.

Execution risk is higher, but cash comes back faster.

Hold scenario

Buy in a school district or job node that renters value.

Stabilize with a targeted refresh that reduces repairs over the next five years.

Traditional mortgage that a good rent can help service.

Returns build through cash flow, principal paydown, and appreciation.

Image Source: pexels.com

Run the numbers both ways, then stress-test them with longer days on market, a lower resale price, or a small rate increase. If you cannot absorb a slower sale or a vacant month, the flip may be too tight. If the cash flow barely covers the mortgage at conservative rents, the hold may need a better buy price.

As you negotiate, keep your inspection contingency and timelines front and center so you can exit or renegotiate if a major issue is uncovered. If the inspection reveals structural or safety problems, you can push for repairs, credits, or decide to walk away without risking your earnest money when the contingency is properly drafted and timed.

Practical Steps to Take

Research the submarket, not just the metro. Track sales on the blocks where you plan to buy. Drive the area, talk to neighbors, and note any public works or new retail.

Get your financing buttoned up early. Preapproval shows strength and keeps closing on schedule. Strong files help you avoid last-minute document chases and let you lock a rate within your lender’s timeline.

Build a reliable team. For flips, you want a contractor who can price scope quickly, an inspector who finds deal-breakers fast, and an agent who understands investor comps. For holds, add a property manager and a tax pro.

Use your inspection period wisely. Order the general inspection first, then add pest and, where relevant, radon testing. Review results promptly so you can negotiate repairs, credits, or price. Keep your deadlines tight enough to stay competitive but long enough to make a smart call.

Prepare for closing day like a pro. Bring your ID, confirm your Closing Disclosure matches the final paperwork, and have proof of homeowners insurance ready. Verify wire details with your title company over a trusted phone number before you send funds. Finish with a thorough final walk-through so the property you receive matches the contract and any agreed repairs.

Keep liquidity. Whether you are flipping or holding, a cash reserve keeps you flexible if a repair runs over budget or a unit sits vacant longer than expected.

So, What Should You Do?

There is no universal play here. If you have renovation experience, a dependable crew, and the appetite for hands-on work, a well-bought flip can deliver quick profits. If you prefer steadier growth and less project volatility, a long-term hold can build wealth through cash flow and time in the market. Many investors blend both approaches by flipping to generate capital and then rolling profits into solid long-term rentals.

Whichever path you choose, let your neighborhood data, your financing terms, and a disciplined closing and inspection plan drive the decision. That combination gives you the best odds of walking out of closing confident—and set up for the results you want.

WWC and its investment partners closed on the 97-unit multifamily community of Park Place Townhomes. The transaction was advantageously purchased off-market with the assistance of Brian Murphy of Newmark Dallas. StepStone Real Estate (“SRE”), the real estate arm of private markets investment firm StepStone Group (Nasdaq: STEP), is a major equity partner in the transaction. Park Place is a follow-on investment into an existing WWC/SRE joint-venture initiated by a broader GP-led portfolio recapitalization in 2024.

Built in 1980, Park Place Townhomes features spacious two-story units with an average size of 1,116 square feet, offering residents a comfortable and well-designed living experience. As part of the acquisition, WWC assumes a 3.07% fixed-rate mortgage from the previous owner, resulting in an estimated $1.6 million in interest savings over the loan term compared to current market rates. The loan assumption was handled by Katie Runyan of Walker & Dunlop.

This Dallas-area acquisition strengthens WWC’s presence in the U.S. multifamily housing market and reflects the firm’s disciplined investment approach. Ideally situated between Dallas and Fort Worth, the property is just six minutes from Dallas-Fort Worth International Airport and within close proximity to major employers such as American Airlines headquarters, Lockheed Martin, and AT&T Stadium—all reachable within a 23-minute drive.

“This acquisition comes at an opportune time in the market cycle,” said Jay O’Connor, Vice President of Acquisitions at WWC. “We’re acquiring this asset at 42% below current replacement cost, which presents a compelling opportunity for equity growth and attractive returns.”

Doug Mather, WWC’s Chief Investment Officer, echoed this sentiment: “We’re seeing clear buying signals in the market, with property values down 30–40% from their peak, rent growth poised to rebound, and job growth remaining strong. Park Place Townhomes offers a rare chance to invest near the bottom of the market in a highly desirable product located in a prime area.”

About Western Wealth Capital

WWC has developed a proven system for investing in multifamily properties in key real estate markets across the U.S. WWC offers investment partners the opportunity to invest in properties with substantial value-add opportunities. Since its inception, WWC has successfully completed more than $6.4 billion in real estate transactions, acquiring 130 multifamily assets representing more than 29,000 total units.

WWC’s vision is to build wealth for its investment partners with exceptional returns. A people-first approach promotes excellence at every point, with highly efficient operations and a true commitment to our communities. The company’s current portfolio of assets under management includes 35 multifamily rental buildings across five different U.S. metropolitan areas located in the Sun Belt region.

Every housing market runs on the same two forces: supply and demand. They’re what push prices up or down, decide how fast homes sell, and influence whether it feels like a buyer’s market or a seller’s market. Once you get a handle on how these forces play out where you live, you’ll be in a much better spot to make the right move, whether you’re a homebuyer, seller, or real estate professional, understanding local market dynamics helps you make smarter decisions.

Right now in 2025, the U.S. housing market is shifting toward balance. Listings are climbing, price growth has cooled, and buyers have more options than they did in the past couple of years. For sellers, it means setting the right price and standing out matters more than ever. For buyers, it opens the door to better choices and more negotiating power.

Analyzing Local Market Dynamics

The easiest way to look at supply and demand is to think about it in plain terms. Supply is the number of homes for sale. Demand is how many people want to buy and how much they can afford. When buyers outnumber listings, sellers usually get multiple offers and higher prices. When there are plenty of homes sitting on the market, buyers have the upper hand and can push harder on price.

The numbers from mid-2025 tell the story. By July, inventory had gone up for 21 months in a row — almost 29% higher than the year before. Homes were also staying on the market about five days longer. That’s a big change from the fast-paced market of the last few years and shows things are shifting toward balance. Still, some regions like the South, Northeast, and Midwest are seeing more sales compared to a year ago.

You don’t need to be an expert to track this. Your local MLS or national sites like Realtor.com make it easy to see how many homes are listed, what the median price looks like, and how long homes are sitting before they sell.

Right now, many listings are sitting on the market without offers, and price growth has slowed to about 1% year over year. For buyers, that means more time and more choices. For sellers, it means pricing your home right and making sure it stands out.

Key Economic Factors Influencing Supply and Demand

What happens in your local economy plays a huge role in housing. When jobs are growing, new businesses are opening, or big projects are underway, more people move in and demand for homes goes up. When the economy slows, buyers can get nervous and hold back.

Mortgage rates also carry a lot of weight. This year, they’re not exactly cheap, but they’ve leveled off. A 15-year loan sits around 5.5%. That steadiness matters. Buyers may stretch their budgets, but they can at least plan without rates jumping week to week.

Other signs are worth tracking. Builder confidence slipped this year, hinting that fewer new homes could hit the market. Rental households are also growing faster than owner-occupied ones, showing that some people are choosing flexibility over long-term commitment.

Then there are the local shifts you notice close to home. A new highway interchange, a big employer setting up shop, or even new schools can drive fresh demand. On the flip side, more “price reduced” signs or delistings in your neighborhood are usually a sign that sellers are testing the market and not finding enough takers.

Leveraging Digital Tools for Market Insights

You don’t have to rely only on monthly reports to know what’s going on in your market. Digital tools give you a way to check the pulse almost in real time.

Start with housing sites. Zillow, Realtor.com, and Redfin all have dashboards that update daily. You can see how many homes are on the market, how prices are trending, and even how long houses are sitting before they sell. Google’s search data is another quick tool, if more people in your area are searching “homes for sale,” demand is picking up.

Social media platforms (Facebook, Instagram, and LinkedIn) can tell a story as well. Local Facebook groups often buzz when a new subdivision breaks ground. Instagram posts can show which neighborhoods buyers are excited about. On LinkedIn, agents share quick market takes that give you a feel for how competitive things are. If you share your own updates, maybe a short note about price cuts in your town or photos of a growing neighborhood, people start seeing you as someone in the know.

Even online ads give away clues. When searches in your zip code spike, it usually means more buyers are circling. Paying attention to those patterns helps you spot shifts before they’re obvious in the headlines.

Mastering Supply and Demand for Success

There isn’t a single formula that works for every market, but keeping tabs on supply and demand gives you a big advantage. Growth is just slower around 3% or less nationwide, which means balance is the theme.

For buyers, that balance shows up as more choices and a little more breathing room. You don’t always have to rush an offer the first weekend a house hits the market. For sellers, it’s about staying realistic. Pricing competitively and making your home stand out online matters more now than it did a couple of years ago.

The key is to check in often. Watch the data from housing sites, pay attention to what’s happening in your own neighborhood, and lean on digital tools and community input to see where interest is heating up. Mix those pieces together and you’ll have a clearer picture of where things are heading. That way, whether you’re buying, selling, or helping others, you’ll be making decisions based on what’s really happening not just headlines.

Scrolling through social media, it’s hard not to stop when you see a garage lined with Ferraris, Lamborghinis, or McLarens. For some people, these cars are a childhood dream come true. For others, they’re a way to build wealth while enjoying something unique. In many cases, exotic car collecting ends up being both, a passion that also carries investment potential.

The Investment Side: Beyond the Look

High-end cars can act like alternative assets, and certain models have shown remarkable growth. A Ferrari F40 that sold for around $400,000 in the early 2000s now trades for well over $1.5 million. And if you’ve ever thought about selling my Ferrari 458, you’d find that some modern exotics can still hold strong demand, depending on mileage and condition.

Rare models such as the McLaren F1, Porsche Carrera GT, and early Lamborghini Miura have also multiplied in value as supply remains limited and demand keeps climbing among global collectors.

That doesn’t mean every exotic car gains value. Mass-produced models often lose money once they leave the dealership. Rarer cars with a strong heritage tend to hold or increase in value. A Porsche 911 GT3 RS or a special-edition Ferrari often attracts buyers years down the road, while a standard version from the same era may not.

The key factors that drive appreciation include:

Rarity and exclusivity. Limited production numbers almost always matter. When only a few hundred cars exist worldwide, collectors tend to compete for them, which pushes values higher.

Historical significance. Cars with racing pedigree, a role in automotive history, or association with a milestone moment in design often carry added weight in the market.

Condition and provenance. A car that has been well maintained, with original parts and clear documentation of ownership, usually commands a premium. Provenance, such as being owned by a notable collector or celebrity, can add even more appeal.

Market demand. Broader trends also play a role. If certain eras or models become popular with new generations of buyers, prices follow that demand. In recent years, 1990s supercars have attracted fresh attention, showing how tastes shift over time.

The Hobby Side: Pure Automotive Joy

For a lot of collectors, the payoff isn’t measured in resale value. It’s the way a Ferrari 812 Superfast sounds when it climbs toward redline, or the way a Porsche GT3 hugs the pavement through a tight corner. These are experiences you don’t get from a stock certificate.

Each car tells a story. A Lexus LFA with its Yamaha-tuned V10 is remembered as one of the last analog supercars. A McLaren P1 represents a turning point for hybrid performance. When you add one of these machines to your garage, you’re tying yourself to that history.

Then there’s the community. Weekend Cars and Coffee meets, private track days, or even a casual drive up the coast put you alongside people who share the same obsession. The atmosphere is less about posing for photos and more about swapping stories, checking out each other’s builds, and appreciating engineering at its highest level.

The Reality Check: Hidden Costs and Risks

Before you start scrolling through Bring a Trailer or calling up a dealer, it’s worth knowing what ownership really looks like on the financial side. Insurance alone can run several thousand dollars a year, even with a clean record. Routine maintenance is on another level. A Ferrari may require a $15,000 service every few years, and sourcing parts for a rare McLaren or Bugatti can mean long waits and premium prices.

Storage is its own challenge. You can’t leave a seven-figure hypercar parked in the driveway and expect it to hold its value. Most serious collectors invest in climate-controlled garages with advanced security, regular detailing, and tire care to keep everything in top shape. Those costs add up quickly.

There’s also the market to think about. Exotic cars don’t always move in one direction. When times are good, demand is strong and prices climb. When the economy slows, buyers step back and even sought-after models can lose momentum. What felt like a safe bet one year might sit unsold or drop in value the next.

Finding Your Balance

For most collectors, the sweet spot is enjoying the cars first and treating any financial upside as a bonus. If you pick models you’re excited to drive and proud to park in your garage, you’ll never feel like you lost, no matter what the market does.

Still, it pays to be thoughtful. Cars built in small numbers, with strong performance specs and a clean history, usually hold up better over time. Don’t put yourself in a financial squeeze hoping for a quick flip. Exotic cars rarely work that way. The longer you own, the better chance you’ll have of seeing real appreciation.

The collectors who do best tend to mix passion with patience. They spend time learning the market, talking to other owners, and waiting for the right opportunities. Over time, that balance often leads to a collection that delivers more than one kind of return, both the joy of ownership and, in many cases, solid long-term value.

The trend of leaving Texas cities for mountain-lake destinations is gaining momentum, as high-end buyers seek privacy, wide-open spaces, and year-round recreation without sacrificing comfort. North Idaho and the Lake Coeur d’Alene area have become favorites. Here, you can pair a country-club lifestyle with lakefront estates, private golf communities, and the kind of small-town warmth rarely found in traditional resort markets.

Knowing how the move works, from travel logistics to what ownership really means, can help you make a confident decision about life on the lake.

Why Dallas Buyers Are Looking North

From Heat Fatigue to Four Seasons Without Losing Luxury

North Idaho delivers all four seasons: warm, sunny summers, golden autumns, snow-filled winters, and bright green springs. For many buyers coming from Dallas, this variety is a refreshing change from the long stretches of Texas heat. Summer highs typically stay in the low 90s, and when winter rolls in, you can be skiing or snowboarding at Schweitzer Mountain Resort in about an hour.

Homes in this market are built to handle year-round living. Heated driveways, professional snow-removal services, and winterized docks keep properties usable even in the coldest months. At the same time, you don’t lose access to the lifestyle amenities you’re used to. Private clubs keep their dining rooms, fitness centers, and spa services open all year, so you won’t run into the seasonal shutdowns that are common in other mountain destinations.

Privacy, Space, and Water: Lakefront Living as the New Backyard

Lake Coeur d’Alene is famous for its sparkling water and lively shoreline, while nearby Hayden Lake offers a quieter setting with luxury estates tucked into wooded coves. In Dallas, luxury homes often showcase elaborate pools, cabanas, and outdoor kitchens. In North Idaho, the equivalent is direct lake access with a private dock, deep-water frontage, and wide-open mountain views right from your back deck.

Many parcels range from two to fifty acres, giving you a level of privacy that’s hard to find in established Dallas neighborhoods.

The Second-Home Equation

For many Dallas buyers, owning in North Idaho isn’t about replacing Texas—it’s about diversifying lifestyle. A lake home becomes the place for long summer stays, extended stretches of remote work, or holidays when family wants to gather in one place. Travel is surprisingly convenient. Coeur d’Alene Airport (Pappy Boyington Field) sits just nine miles northwest of downtown Coeur d’Alene and offers private aviation access, making regular trips back and forth practical.

Multi-generational living comes naturally in this setting. Lake homes turn into gathering points where kids and grandkids spend summers learning to ski, wakeboard, or simply enjoy the outdoors. For many Dallas families, it’s a way to give the next generation a connection to nature and a slower rhythm of life that’s harder to find in urban Texas.

Where Luxury Lives in North Idaho

Lake Coeur d’Alene and Hayden Lake Waterfront Estates

Hayden Lake is the second-largest lake in Kootenai County, surrounded by timbered hills and more than 4,000 acres of open water. Waterfront estates typically include 100–400 feet of shoreline, private docks with boat lifts, and deep-water frontage for larger boats.

Homes range from contemporary glass-and-steel designs that frame the lake to log-and-stone lodges that sit naturally in the landscape. Premium sites are in protected coves with southern exposure, giving owners more sun and calmer water for outdoor living and water sports.

Private Club Communities

North Idaho luxury communities (Black Rock, Gozzer Ranch, CDA National Reserve), offer the same country club lifestyle Dallas buyers know, but in a mountain setting. Gozzer Ranch combines full-service club amenities with the pace of a small-town resort. CDA National Reserve limits membership to property owners, with a $150,000 initiation and $22,500 in annual dues.

The Golf Club at Black Rock, designed by Jim Engh, was the first private club in Coeur d’Alene and remains a flagship. Eighteen holes cut through cliffs, rock outcroppings, and wooded terrain. Each community includes concierge service, marina access, fitness centers, and dining programs comparable to Dallas country clubs.

Downtown Coeur d’Alene Luxury Condos

In the resort district downtown, high-rise condos give buyers waterfront access with full concierge support and marina slips. These lock-and-leave homes appeal to owners who want maintenance-free living close to restaurants, shopping, and seasonal festivals.

Home Typologies Dallas Buyers Compare

Waterfront Estates

Before you can build a dock or similar structure on a navigable lake, the Idaho Department of Lands requires an encroachment permit. Some estates already have grandfathered permits in place, while others may need new applications. Most waterfront homes sit in no-wake zones, which extend 200 feet from the shoreline, dock, pier, or breakwater—important for safe swimming and boating.

Along the shoreline, a 25-foot management area begins at the ordinary high-water mark. This buffer limits how you can landscape or build near the water. Owners also need to think about winter systems. Many docks are either pulled out of the water seasonally or protected with heated devices to prevent ice damage. Covered boat storage is standard in most lakefront properties.

Club and Golf Communities

Membership structures usually divide golf, dining, and marina privileges into separate tiers. At CDA National Reserve, membership is capped at 275, the same number of residential lots. So every property owner has access without tee time restrictions. Guest policies differ by community, but most allow member-sponsored access and offer reciprocal privileges with other Discovery Land Company properties.

Luxury Condos

Downtown luxury condos stack amenities in ways that mirror resort living. Expect fitness centers, spa facilities, wine lockers, and assigned boat slips. HOAs typically cover exterior upkeep, landscaping, snow removal, and shared spaces. Storage is also a focus, with dedicated areas for recreational gear, boating equipment, and seasonal items like skis or patio furniture.

Access and Logistics

Commercial and Private Aviation

Spokane International Airport sits about 40 minutes west of Coeur d’Alene, with nonstop service from major hubs like Chicago, Minneapolis, Denver, Phoenix, Los Angeles, San Francisco, Portland, and Seattle. From there, it’s an easy drive into the lake region with rental cars and private ground services readily available.

For private flyers, Coeur d’Alene Airport (COE) is one of the most active general aviation airports in the West. It offers full ILS approach capability and serves corporate and personal aircraft daily. With private aviation, Dallas buyers can cut total travel time to less than three hours door-to-door from Texas to their lakefront home.

Seasonal Considerations

Winter travel requires some planning. Most luxury homes include professional snow contracts that handle driveways, private access roads, and walkways. Four-wheel-drive or all-wheel-drive vehicles are recommended for visiting in colder months, though the main highways and arterials are consistently plowed and maintained.

Service Ecosystem

North Idaho’s high-end market comes with a strong support network for second-home owners. Property management companies handle winterization, security checks, and year-round maintenance. Within communities, services extend further. Gozzer Ranch operates two marinas and a beach club, with slips allocated by season and membership. Concierge teams in private clubs assist with activity planning, dinner reservations, and local logistics so your time on the lake stays focused on lifestyle, not upkeep.

Ownership Nuances That Affect Enjoyment & Value

HOA and CC&R Considerations

Community covenants typically address boat size restrictions, dock specifications, exterior material requirements, and defensible space maintenance for wildfire protection. Architectural review processes govern modifications and additions, with some communities requiring specific design professionals or pre-approved materials.

Utilities and Infrastructure

Well and septic systems serve many rural luxury properties, requiring inspection records and reserve areas for future expansion or replacement. Lake-draw intakes provide water access but require permitting through Idaho Department of Lands for new installations or modifications.

Fiber internet availability varies by location, with some communities providing dedicated high-speed infrastructure while rural properties may depend on satellite or cellular systems for reliable connectivity.

Insurance and Risk Management

Wildfire interface zones require specific construction materials and defensible space maintenance. Insurance carriers evaluate roof materials, access roads, and fire department response times when setting premiums. Snow load requirements influence roof design and construction costs, particularly for large-span structures with extensive glazing.

Shoreline properties face erosion considerations, with some areas requiring engineered solutions for long-term stability. Professional assessments help buyers understand potential future costs and mitigation strategies.

Short-Term Rental Realities

Many communities prohibit short-term rentals to maintain residential character, while others allow limited rental activity under strict guidelines. Permit caps in some jurisdictions limit new STR licenses, affecting potential income generation and exit strategies.

Lifestyle Translation for Dallas Readers

From Country Club Tee Times to Lake Mornings and Mountain Afternoons

Life shifts from structured club schedules to open-air recreation. At Black Rock and other private clubs, tee times aren’t required—members head out when they choose. Lakefront homes put boating, fishing, and swimming steps away, with no reservations and no waitlists.

Recreation follows the seasons. Summers bring wakeboarding and long days on the water. Fall adds hiking trails, river fishing, and upland hunting. Winter means skiing at Schweitzer or snowshoeing through the woods. Spring delivers early trails, wildlife viewing, and high mountain rivers. National forests and wilderness sit only minutes away, balancing outdoor access with luxury amenities.

Dining, Arts, and Event Calendars

The social calendar runs at a resort-town pace. Summer highlights include outdoor concerts, lake festivals, and weekly farmers markets. Winter slows into smaller dining rooms, gallery shows, and club events. Reservations are easier than Dallas, though fine dining is concentrated in downtown Coeur d’Alene and at resort properties.

Remote Work and Schooling Viability

High-speed internet supports professional remote work in most luxury communities, though backup systems are recommended for critical use. Education options include public schools rated above state averages, local private academies, and distance programs that allow families to stay connected to Texas schools.

A Smart 3-Day Scouting Plan

Day 1: Waterfront Tour

Begin with lakefront properties on both Lake Coeur d’Alene and Hayden Lake. Compare shoreline exposure, wind patterns, and water depth. Hayden Lake offers more protection from wind, with public ramps at Honeysuckle Beach, Sportsman’s Park, and Tobler’s Marina. Schedule time with local marinas to review slip availability, waiting lists, and seasonal dock services.

Day 2: Private Club Communities

Meet with membership coordinators at target communities. Tour practice facilities, fitness centers, and dining venues. Review initiation fees, monthly dues, and transfer requirements. Spend time on the golf course to see course conditions, clubhouse operations, and the overall member environment.

Day 3: Downtown and Trail Systems

Explore downtown luxury condos and lifestyle amenities. The North Idaho Centennial Trail runs along the north side of Lake Coeur d’Alene, popular for cycling, running, and walking. End the day with a sunset cruise to view the lake and its shoreline from the water.

Questions to Ask Checklist

Membership transfer fees and approval timelines

Marina slip availability and waitlist details

Snow management contracts and annual costs

Fiber internet access and backup solutions

HOA and CC&R rules for modifications and rentals

Property management service options and pricing

Quick-Glance Comparison Table

What You Love in Dallas

North Idaho Equivalent

What to Verify

Club life and amenities

Private golf communities with concierge services

Membership transfer process and fees

Pool and cabana culture

Lake access with private docks and beach areas

Dock permits and seasonal maintenance

Valet and concierge services

Club services and property management companies

Service availability and response times

Neighborhood amenities

Trail systems, marina access, and nearby parks

Year-round access and maintenance standards

Large backyard privacy

Lake frontage and acreage parcels

Shoreline setback requirements and CC&Rs

Indoor/outdoor living

Covered decks, outdoor heaters, snow-rated builds

Winter functionality and heating costs

FAQ

Is lake access public or private? Lake Coeur d’Alene has 100+ miles of shoreline. Public beaches and boat launches available. Waterfront owners hold private access from their property line.

How do dock permits work? Dock encroachment permits issued by Idaho Department of Lands. Applications require neighbor notice. Hearings possible if objections filed. Existing docks may carry grandfathered permits. New docks require full approval.

Are there STR restrictions in club communities? Most private clubs ban or heavily restrict STRs. Rules vary by CC&Rs. Verify before purchase if rental income is part of the plan.

What’s winter maintenance like on hillside drives? Snow contracts standard for private roads, driveways, walkways. Regular plowing required. Heated driveways common on higher-end properties.

How do buyers evaluate water quality and invasive species? Testing records available through health departments and state agencies. Hayden Lake supports bass, crappie and perch are indicator of strong ecosystem. Invasive species monitoring active across regional lake systems. Owners expected to follow protocols.

Owning a home in Connecticut means dealing with property taxes every year. They’re not small either, in some towns your tax bill can feel almost like a second mortgage. The money goes to things you use every day, like schools, fire and police protection, trash pickup, and local roads.

Each town sets its own mill rate, so what you pay in Hartford can be very different from what a homeowner pays in Fairfield or Norwich. That’s why two houses with the same value might have very different tax bills.

If you understand how your property is assessed and how the rates are set, you’ll have a much easier time planning your budget. You’ll also know when it makes sense to challenge your assessment or apply for exemptions that can lower your bill.

How Property Taxes Work in Connecticut

Every town in Connecticut sets its own property tax rate, known as the mill rate. Your annual bill is calculated by applying that rate to the assessed value of your home and land. One mill equals $1 in tax for every $1,000 of assessed value.

Because the system is local, tax bills vary widely. For example, Hartford’s mill rate is above 60, which means homeowners there often pay some of the highest property taxes in the state. In contrast, Greenwich’s rate is closer to 11, so even though home values are high, the tax rate itself is lower.

The money collected stays in your community. It pays for schools, police and fire protection, road maintenance, trash collection, and other local services. In short, it’s how towns keep things running.

Who Collects Property Taxes

If you live in Connecticut, the tax bill you get in the mail doesn’t come from the state. It comes straight from your town. Every city and town has its own tax collector’s office that keeps the books, sends the bills, and tracks payments.

If your mortgage includes an escrow account, your lender pays the town on your behalf, so you never see the bill directly.

Depending on where your property is, you might also notice smaller charges for things like fire districts or sewer improvements. These aren’t statewide fees, they’re local add-ons that cover services in specific neighborhoods.

How Property Taxes Are Calculated in Connecticut

Your tax bill in Connecticut comes down to three numbers: the assessed value of your property, the assessment ratio, and the mill rate set by your town.

Assessed Value Every property in Connecticut is assessed at 70% of its fair market value. So if your home could sell for $300,000, the town will set your assessed value at $210,000.

Mill Rate The mill rate is the local tax rate. One mill equals $1 of tax for every $1,000 of assessed value. For example, if your town’s mill rate is 30, and your home’s assessed value is $210,000, your yearly property tax would be $6,300.

Local Adjustments Mill rates vary widely across the state. In 2024, Bridgeport’s mill rate was over 40, while Greenwich kept theirs close to 11. That’s why two homes with the same market value can end up with very different tax bills depending on where they’re located.

How Your Property’s Value Is Assessed in Connecticut

All towns in Connecticut review property values on a regular schedule, generally every five years. The goal is to keep tax bills in line with current market conditions. Between full revaluations, the assessor may still adjust your property’s value if you make major changes, like adding an extension or finishing a basement.

Assessors use a few different methods to figure out your home’s value:

Sales Comparison – Your property is compared to similar homes that recently sold in your area.

Cost Method – The town estimates what it would cost to rebuild your home today, minus depreciation.

Income Method – For rental or commercial properties, value is based on the income the property could generate.

If you live in a hot market like Fairfield County, where home prices have climbed quickly, you’ll probably see higher assessments. On the other hand, towns in eastern Connecticut, where sales prices have risen more slowly, may show smaller jumps in assessed values.

What Affects Your Property Taxes

Your property tax bill can go up or down depending on several factors. Here are the most common ones Connecticut homeowners see:

Market Trends: If home prices in your town go up, your assessed value may increase the next time the assessor updates records.

Home Improvements: Adding a garage, finishing the attic, or expanding living space can raise your property’s assessed value.

Local Tax Rates: Each town sets its own mill rate. When the town budget grows for schools, road work, or public safety, the rate can increase, and so does your bill.

Paying Property Taxes in Connecticut

In most Connecticut towns, property taxes are due twice a year, on July 1 and January 1. Some larger cities, like Hartford and New Haven, also allow quarterly installments.

If you have a mortgage, your lender probably includes property taxes in your monthly payment and sends the money to the town through an escrow account. This way, you don’t have to worry about missing a deadline.

If you pay directly, be careful with due dates. The state charges 1.5% interest per month on late balances. Unpaid bills can lead to a lien on your home and, if ignored, a possible tax sale.

Appealing Your Property Tax Assessment in Connecticut

If you think your home’s assessed value is too high, you can file an appeal. The process is local, handled by the Board of Assessment Appeals in your town.

Here’s how it works in Connecticut:

Check your assessment: Review the details on your property card from the assessor’s office. Mistakes in square footage, number of bedrooms, or lot size can raise your value unfairly.

Gather proof: Collect recent sales of similar homes in your neighborhood or get an appraisal that shows a lower value.

File on time: Appeals are usually due by February or March, depending on the town. You’ll need to submit your request before the deadline to be heard.

Attend the hearing: Bring your evidence and explain why your assessment is too high. The board will decide whether to adjust it.

If you win, your assessed value and your future tax bills will be reduced.

How to Lower Your Property Tax Bill

While you can’t control your town’s mill rate, there are a few steps that may lower what you pay:

Apply for exemptions: Connecticut offers relief programs for seniors, veterans, and homeowners with disabilities. Some towns also give breaks for primary residences.

Check your property record: Errors in square footage, number of rooms, or lot size can lead to higher assessments. Fixing them may reduce your bill.

File an appeal: If your assessment is above market value, bring evidence to the Board of Assessment Appeals.

Stay engaged locally: Following town budget meetings helps you understand and sometimes influence decisions that affect future mill rates.

Property Taxes When You Sell a Home in Connecticut

In Connecticut, property taxes are paid at closing. The bill is split between the seller and the buyer based on the exact date the property changes hands. For example, if you sell your home in mid-April, you’ll pay taxes for January through mid-April, and the buyer covers the rest of the year. This adjustment is handled by the attorney or closing agent so that no one overpays or inherits an unpaid balance.

Be sure your tax records are up to date. If you’ve appealed your assessment or claimed an exemption, keep copies of the decisions and recent bills. Buyers often ask to review this paperwork during negotiations. Having it ready not only avoids delays but can also make your property more appealing, since Connecticut towns vary widely in mill rates. For sellers who need to sell their house fast, keeping tax records and paperwork in order helps the closing stay on track.

Property Taxes and Real Estate Values in Connecticut

Property taxes play a role in how homes are valued across Connecticut. Towns that keep tax rates balanced often attract more buyers, while places with high mill rates can make some buyers think twice, even if the homes themselves are priced fairly.

The effect isn’t always negative, though. In many cases, the services funded by property taxes, like well-rated schools, reliable public safety, and good roads actually help protect or increase property values. That’s why towns in Fairfield County, even with higher home prices, continue to draw strong demand. Buyers see value in what the taxes support.

For homeowners, the takeaway is that property taxes are part of the overall picture of affordability. A lower sticker price on a house doesn’t always mean lower costs if the town’s mill rate is high. When you compare communities, it helps to look at both the home price and the yearly tax bill to get a true sense of what you’ll spend to live there.

Final Thoughts

Property taxes aren’t set once and forgotten. Towns revalue homes every five years, and mill rates change with each local budget. If you keep an eye on those two factors and know when to claim exemptions or file an appeal, you’ll be better prepared for the next tax bill.

For many homeowners, the difference comes down to paying attention. Review your assessment, show up at budget hearings if you can, and take advantage of any relief programs you qualify for. A little preparation can make property taxes easier to manage year after year.