The Dallas-Fort Worth metroplex is adding thousands of new residents every year, and 2026 will likely be no different. Whether you’re moving for a new job, a more affordable cost of living, or just a change of scenery, this guide will help you get up and running.

Here’s what you need to know about the local market, neighborhoods, and logistics before you pack your bags.

Why People Are Moving to DFW

The DFW area consistently ranks as one of the fastest-growing metros in the country. The reasons are simple: Texas has no state income tax, which can put more money in your pocket from day one.

The job market is diverse, from tech and healthcare, to finance, logistics and manufacturing. Big companies like Toyota, AT&T and American Airlines have a strong presence in the area and the startup scene is booming. For anyone moving here, the economic opportunity is a major draw.

Choosing a City in the Metroplex

DFW is sprawling—covering more than 9,000 square miles across 11 counties—so your first big decision is where to put down roots. Every city has its own distinct vibe.

Dallas is more city-like with great food, arts and nightlife. It’s a good fit if you want walkable areas and city energy.

The culture in Fort Worth is more laid back western type, with a strong community. Housing can also be slightly more affordable.

Plano and Frisco are top choices for families because of their highly rated schools and newer suburban neighborhoods.

Located between Dallas and Fort Worth, Arlington makes it easier to commute to either side of the metroplex.

If you’re a frequent traveler who needs fast access to DFW Airport, Irving and Coppell are worth considering.

Before signing a lease or buying a home, do research on which city will suit your lifestyle, commute and budget.

DFW Cost of Living in 2026

DFW remains cheaper than many large cities on the coast, but housing costs have gone up. Home prices vary widely by ZIP code, so budget wisely. Everyday expenses like groceries and utilities tend to stay relatively close to the national average, but your exact costs will depend on where you live and how far you commute.

Getting Around the Metroplex

Owning a car is practically a must. The highway system is massive, and the metroplex is spread out. While DART (Dallas Area Rapid Transit), provides rail and bus service within Dallas and some suburbs, it doesn’t cover the entire metro area. If you’re commuting, map out your drive during peak hours before signing a lease. Traffic on major corridors like I-35E, I-635, and the Dallas North Tollway gets notoriously heavy during rush hour.

Planning Your Move

If you’re coming from out of state, visit first to tour neighborhoods in person instead of relying strictly on photos.

Many newcomers who are moving to Dallas find it helpful to hire professionals familiar with the city’s layout, building access policies, and high-rise move-in procedures, if applicable.

Things to Do After You Move

Get your Texas driver license through the Texas Department of Public Safety within 90 days of moving.

Set up utilities like electricity, water, gas, and internet as soon as you have a move-in date. Since much of Texas has a deregulated energy market, you may need to choose a retail electric provider depending on your address.

Find nearby healthcare providers, including a primary care doctor and a dentist.

Explore your neighborhood to find the closest grocery stores, pharmacies, and parks.

Finding Community

If you are moving to DFW, you will want to find your tribe. Check out community groups, neighborhood associations, and professional groups. Most cities in the metroplex have regular events such as farmers markets and outdoor concerts where you can meet people.

If you have children, joining their school or sports teams is a quick way to grow your social network. Volunteer groups and local hobby clubs are also good ways to meet new people.

Making DFW Your New Home

Moving is a big adjustment, but a good plan makes the transition much easier. Check out the different neighborhoods at your own pace, and you’ll be settling into your new DFW life in no time.

Congratulations on finding the right home for your family. Now comes the part most people do not exactly love: moving.

Hiring professional movers can take a lot of stress off your plate, but there are still several things you should do before moving day. A little planning can help protect your belongings, keep the day organized, and make the transition into your new home much smoother.

Here are practical steps to help you prepare.

Start Packing and Sorting Early

Packing is not the most exciting part of moving, but starting early makes a big difference. If you have a few weeks before the move, begin by going room by room and sorting your belongings into four categories: keep, sell, donate, and throw away.

The less you move, the less you have to pack, carry, unload, and unpack later.

Start with items you do not use every day, such as seasonal clothing, books, decorations, extra linens, and rarely used kitchen items. Save daily essentials for last.

As you pack, label each box clearly. Include the destination room, a short list of contents, and notes such as “fragile,” “heavy,” or “open first.” It may feel tedious while you are doing it, but it saves a lot of time when you are trying to find your clothes iron, phone charger, towels, or coffee maker after the move.

It also helps to pack one essentials box or bag with items you will need right away, such as toiletries, medications, chargers, basic tools, paper towels, snacks, important documents, and a change of clothes.

Confirm Details Before Moving Day

A few days before the move, confirm the schedule with your movers and anyone else helping you. Make sure everyone knows the arrival time, addresses, parking instructions, gate codes, elevator access, and any special details about the home.

You should also take photos of furniture, electronics, appliances, and fragile items before they are moved. These photos can help if anything is damaged or needs to be reassembled later.

Before the crew arrives, clear walkways in both homes. Remove tripping hazards, secure loose rugs, and make sure doors, hallways, stairs, and driveways are easy to access.

Prepare the Home for Movers

Moving day goes faster when your home is ready before the first box leaves the house.

If possible, disassemble large furniture ahead of time or confirm whether the movers will handle it. Tape hardware in a labeled bag and attach it to the furniture it belongs to. Unplug appliances and electronics, wrap cords, and label cables so setup is easier later.

Keep valuables, passports, financial documents, jewelry, medication, and personal records with you instead of loading them onto the moving truck.

You should also set aside items that movers may not be allowed to transport, such as paint, propane tanks, gasoline, certain cleaners, pesticides, and other hazardous materials. Dispose of these items safely according to local rules before moving day.

Keep Moving Day Organized

Moving day can get hectic fast, so it helps to have one person directing traffic. This person can answer questions, tell movers where items go, and make sure boxes are loaded and unloaded in the right order.

Here are a few smart moving-day tips:

Keep children and pets away from the work area.

Have water and simple snacks available.

Keep your phone charged.

Make sure the essentials box stays with you.

Do one final walk-through before leaving the old home.

Check closets, cabinets, drawers, the garage, the attic, and outdoor storage areas.

Even with a solid plan, small things may go wrong. A box may end up in the wrong room, or a piece of furniture may need to be moved twice. Stay flexible. Protecting your floors, walls, furniture, and people matters more than making every detail perfect.

Consider Portable Moving Containers

If you want more flexibility, a portable moving container can be a helpful option. Services such as you pack we move deliver a mobile container at your door step and allow homeowners to pack their belongings at their pace. Once it is loaded, the company picks it up and transports it to your new home or stores it until you are ready.

This can be useful if you need more time to pack, want to avoid driving a rental truck, or prefer to spread the work over several days instead of doing everything at once.

Unload With a Plan

Once you arrive at your new home, focus on the essentials first. You do not need to unpack everything all at once.

Start with the rooms you will need right away: bedrooms, bathrooms, and the kitchen. Set up beds, towels, toiletries, basic kitchen items, and anything you need for the first night.

Before opening every box, check the locks, utilities, appliances, lights, plumbing, and major systems. Make sure everything is working as it should.

As boxes come in, keep them grouped by room. This makes unpacking faster and helps prevent clutter from spreading through the whole house.

Take Care of Yourself During the Move

Moving is physically and mentally draining, even when everything goes well. Take short breaks, drink water, eat something simple, and stretch when you can.

Do not feel pressured to finish the entire house in one day. Start with what you need to sleep, shower, eat, and function. The rest can happen step by step.

Final Thoughts

Moving to a new home can be stressful, but it becomes much easier with the right preparation. Pack early, label boxes clearly, confirm details with your movers, keep important items with you, and focus on the essentials when you arrive.

A move is not just about getting your belongings from one place to another. It is the start of a new chapter, and a little planning can help you begin it with less stress and more confidence.

When you’re looking to buy a house, a new kitchen, fresh paint, and modern finishes are easy to notice. But foundation problems are much easier to miss, and they can be far more expensive to ignore.

The foundation affects the entire structure of a home. Cracks, settlement, drainage problems or movement can mean expensive repairs after closing. Having the foundation inspected before you buy can help you catch red flags early.

Foundation Problems Can Spread Over Time

Foundation issues don’t always stay put. Movement in the foundation can show up in walls, floors, ceilings, doors, windows, and even plumbing systems. A small crack may not seem like a big deal at first. But if you see it with uneven floors, sticking doors, gaps around windows, or cracked drywall, it could be a sign of a more serious structural problem.

These warning signs don’t necessarily mean the home has serious foundation damage. Still, they shouldn’t be overlooked. As the problem gets worse, the damage can spread to other parts of the home.

Catching Problems Early Can Lower Repair Costs

Some buyers assume foundation concerns can wait until after closing. That can be a costly mistake. Minor settlement, drainage problems, or small cracks are often easier to address when they are found early.

More serious repairs might involve installing piers, stabilizing slabs, improving drainage, or doing crawlspace work, all of which can quickly add up, especially if the damage has already impacted floors, walls, or plumbing. Finding these problems before buying gives you a clearer picture of what the home may really cost.

Inspections Give Buyers More Negotiating Power

A foundation inspection gives buyers facts to work with instead of guesswork. If the report shows movement, damage, drainage problems, you can use that to negotiate.

The seller may agree to do repairs, lower the purchase price or give a credit at closing. You also may opt to have a structural engineer or foundation specialist come in for a more in-depth look. Sometimes, the inspection confirms that the problem is manageable. Other times, it helps you steer clear of a home that has more risk than you’re willing to take on.

Don’t Overlook Peace of Mind

When you buy a home with unresolved foundation issues, it can leave you worrying about every new crack, sloped floor, or sticking door. A foundation inspection doesn’t guarantee a perfect home, but it does give you more clarity. It gives you an idea of the structure’s condition, whether repairs might be needed, and whether the purchase is still within your budget.

That kind of clarity can save you money and stress long after closing. Checking a home’s foundation before buying is one of the smartest ways to avoid expensive surprises. In Dallas and across North Texas, where expansive clay soils and moisture changes can put added stress on foundations, structural concerns are especially important to catch early.

Before you commit to a home, take the time to understand what is happening beneath it. A solid foundation protects more than the house. It can help protect your budget.

If you have foundation problems or you want a professional opinion before buying a home, visit pinnaclefoundationrepair.com for professional guidance and support.

Moving to a new city? One of the first things to figure out is whether to rent or buy. It depends on your budget, timeline, and long-term plans, here’s how to weigh your options and make the smartest move for your current situation.

Figure Out Your Immediate Needs

Before you start browsing listings, figure out what you actually need from this move.

Temporary versus long-term: Are you just trying out a city, or are you putting down roots for several years?

Job security: Is your role stable, or are you in a probationary period where things could change?

Family and lifestyle: School districts, commute times, walkability, and access to parks or nightlife can heavily influence your housing choice.

The Case for Renting First

There is a reason many people choose to rent for at least 6 to 12 months after a move. The benefits are hard to beat.

Flexibility: Renting lets you change neighborhoods or jobs without dealing with a stressful home sale.

Lower upfront costs: Renters usually face lower upfront costs, such as a security deposit, application fees, and the first month’s rent, while buyers need to plan for a down payment, inspections, appraisals, and closing costs.

Time to explore: Take the city for a test drive and get a feel for traffic patterns and local hotspots before you buy.

A clean break: If the city or job doesn’t work out, breaking a lease is usually easier than trying to sell a house in a pinch.

Why Buy Soon After Moving?

If you are 100% sure about your move, buying soon after moving makes sense, if you have stable income, and plan to stay long enough to justify the transaction costs.

Building equity: Part of each mortgage payment can help build equity over time, though homeowners also need to budget for interest, taxes, insurance, maintenance, and other ownership costs.

Locked-in stability: With a fixed-rate mortgage, your principal and interest payment stays predictable, though property taxes, homeowners insurance, HOA fees, and maintenance costs can still change.

Complete control: You can renovate and customize your home without the approval of a property manager.

Cost Comparison: Renting versus Buying

The sticker price is never the whole story. You have to look at the total financial picture.

Monthly cost: Compare rent and renter’s insurance against a homeowner’s full monthly cost, including principal, interest, property taxes, homeowners insurance, utilities, maintenance, and any HOA fees.

Upfront payment: Renters pay deposits and application fees, while buyers pay down payments, appraisals, inspections, and closing costs.

The hidden carrying costs: If the HVAC dies, renters call the landlord. Buyers call a repairman and write a big check.

Market Conditions in Your New Location

Local conditions can tip the scale very quickly.

Home prices and trends: Is the market cooling off, or are you walking into a bidding war?

Interest rates: Higher mortgage rates reduce buying power because they make borrowing more expensive, which can lower the price range a buyer can afford.

Rental supply: A historically tight rental market may push you to buy sooner, while abundant rentals give you time to explore.

How Long Do You Plan to Stay?

Your time horizon is the golden rule of real estate.

Short-term: Renting often makes more financial sense if you expect to stay only one to three years, because buying and selling costs can outweigh the equity you build.

Long-term: Owning may become more financially attractive if you plan to stay several years beyond your local break-even point.

The break-even point: There are online calculators that can help you figure out when buying becomes more economical than renting within your specific zip code.

Know Your Credit Score and Financial Status

Before buying anything, take stock of your financial situation.

Credit history: Your credit profile can affect whether you qualify for a mortgage and the rate you are offered.

Debt-to-income ratio: Your existing debts affect exactly how much house you can afford.

Emergency savings: Buying a home can drain your savings at the same time you need a cushion for repairs, moving costs, and other unexpected expenses.

Lifestyle and Personal Preferences

Your personality is just as important as the math.

Flexibility versus roots: If you like to move around, renting can be liberating. If you want to put down roots, buying may be more satisfying.

Maintenance: Are you willing to mow the lawn and fix a leaky sink, or do you want a maintenance-free weekend?

Community: Some rentals have gyms, pools, and common areas, but with a home, you are more likely to be tied to a stronger, long-term neighborhood community.

Rent First, Buy Later

A common strategy is to rent first, then buy after you know the area better. This lets you test commute times, schools, and neighborhoods in real life. Working with a trusted local moving company can simplify that first relocation so you can focus on scouting where you might eventually purchase.

Tips for Making the Right Decision

Consult both a real estate professional and a financial advisor.

Use rent-vs-buy calculators and a detailed budget.

Visit potential neighborhoods at different times of day and talk to residents.

Common Mistakes to Avoid

Rushing into a purchase before understanding the local market.

Ignoring long-term career or family plans when choosing a location or property type.

The Bottom Line

Choosing between renting and buying after a relocation comes down to your timeline, your wallet, and the kind of lifestyle you want. There is no universal right answer. Take a breath, run the numbers, and choose the path that makes your move a little less stressful and supports the life you’re building in your new city.

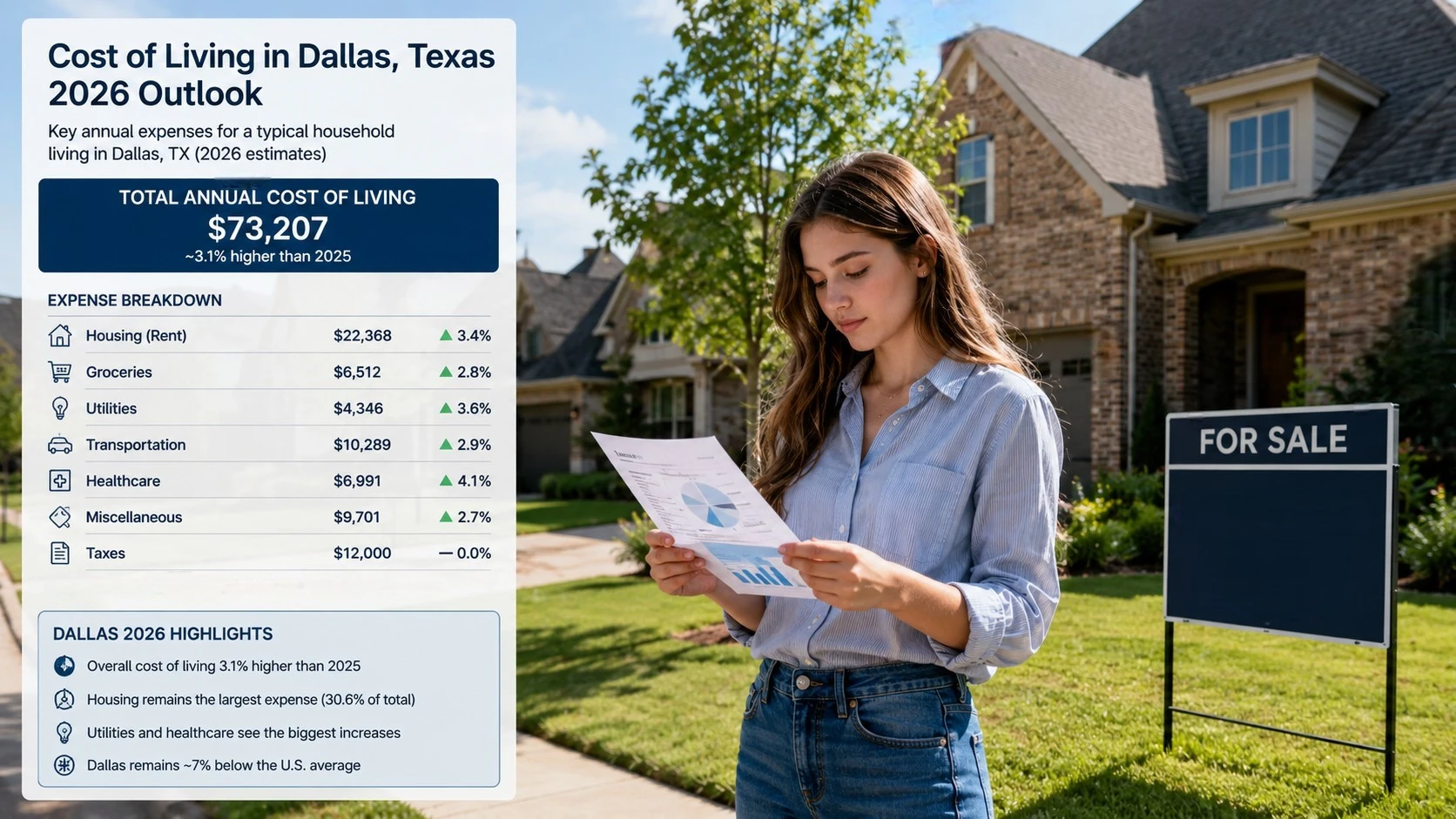

Everyone assumes Texas is cheaper. It shapes relocation conversations, “leaving California” headlines, and every TikTok about Texas freedom. But the reality is more layered, especially after two years of shifting home prices, higher insurance premiums, and bigger property-tax exemptions.

Dallas is generally more affordable than Los Angeles, New York City, San Francisco, Boston, and Seattle. But the gap is not as wide as many newcomers expect. For some buyers, the savings shrink quickly once property taxes and insurance are added to the monthly payment.

Here is what the numbers actually look like in 2026.

The Short Version on Dallas Affordability

Dallas’s overall cost of living is roughly in line with the national average. That sounds modest until you compare it with the cities people are usually leaving. Dallas still remains meaningfully more affordable than most major coastal markets.

The four numbers that really move the relocation math are state income tax, property tax, insurance, and housing prices. Get those four right and you can usually tell whether the move actually pencils out.

What Zero State Income Tax Actually Means

This is the part that does live up to the hype. Texas has no state income tax. There is no progressive bracket, no flat income-tax rate, and no surcharge on high earners because the Texas Constitution prohibits a tax on individual net income.

For someone moving from California, the difference can be substantial. Using current California tax structures and including the 2026 SDI withholding, the rough savings look like this:

At $100K income: about $5,000 to $7,000 per year versus California

At $150K income: about $10,000 to $13,000 per year

At $250K income: about $22,000 to $25,000 per year

At $500K income: roughly $50,000+ per year

California also has something many people miss: State Disability Insurance. In 2026, the SDI rate is 1.3%, and there is no taxable wage ceiling. That means a $200K California earner pays about $2,600 in SDI alone, on top of state income tax. Texas has no equivalent.

The New York comparison can be just as dramatic. NYC residents pay city income tax on top of New York State income tax, and a $200K taxable income can produce roughly $19,000 in combined state and city income tax before federal taxes.

Illinois is closer to a wash, but not completely. Illinois uses a flat 4.95% income-tax rate, so someone earning $150K still gives up roughly $7,000+ in state income tax before exemptions.

This is the foundation of every claim that Texas is more affordable. It is true, but it leaves out several major costs.

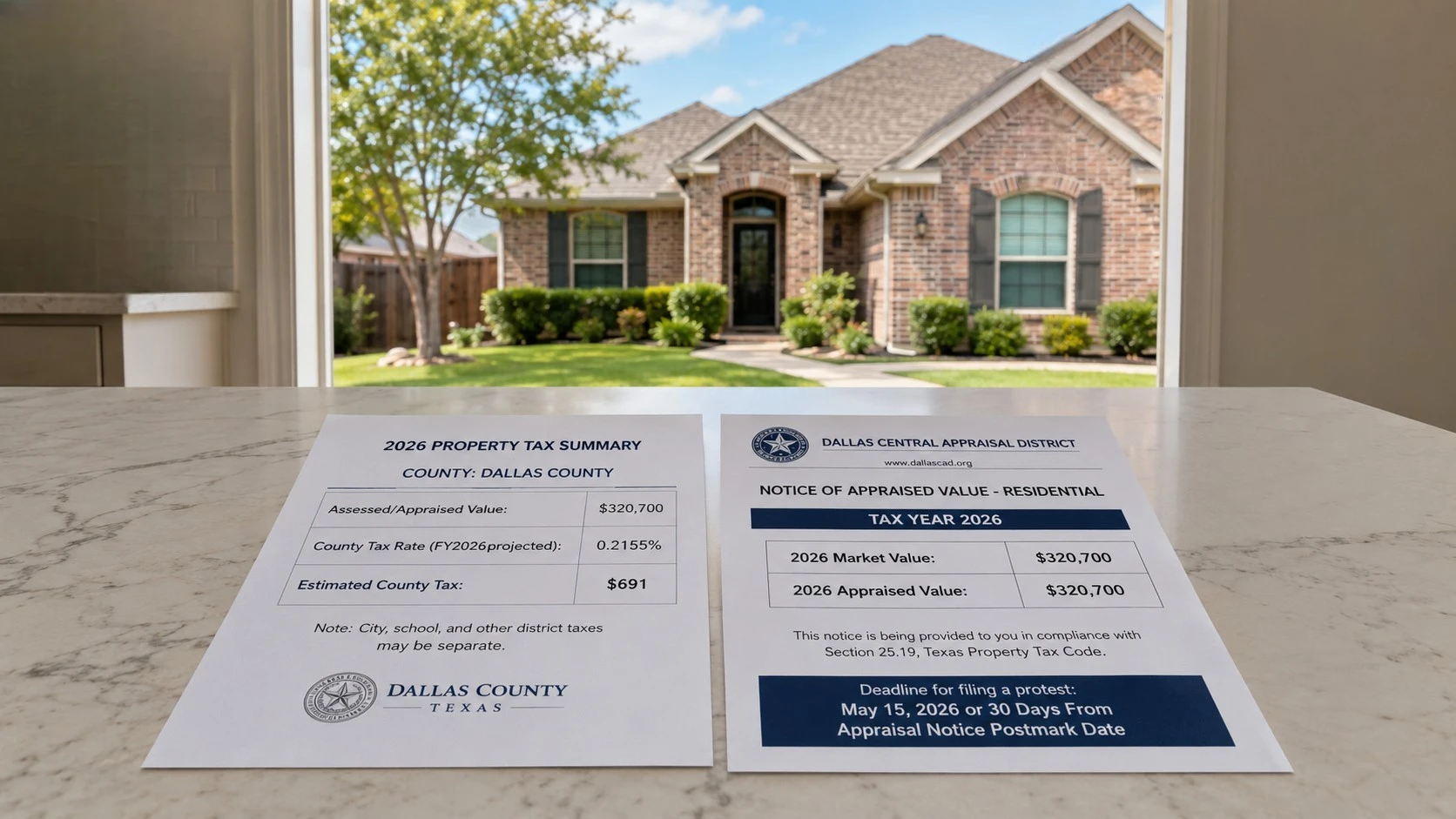

The Hidden Impact of Texas Property Taxes

Texas funds local government heavily through property taxes, and the rates are high. In many DFW cities, buyers should expect an effective property-tax burden somewhere around the high-1% to low-2% range, depending on the city, school district, exemptions, and the home’s assessed value.

In practical terms, the math can look like this:

A $500,000 home in Plano: roughly $9,000 to $11,000 per year in property tax

A $750,000 home in Frisco: roughly $13,500 to $16,500 per year

A $1,000,000 home in Southlake: roughly $18,000 to $22,000 per year, sometimes more depending on exemptions and tax rates

Now compare that with California. Proposition 13 limits the general property-tax levy to 1% of assessed value, though voter-approved local assessments can push the total above that. For long-term California homeowners, the tax bill may be far below current market value because assessed value is capped. That is why a person selling a long-held California home and buying a newer Texas home can be surprised by the property-tax reset.

Recent Texas changes help, but they do not erase the issue. SB 4 raised the school district homestead exemption from $100,000 to $140,000, and voters approved that increase through Proposition 13. Homeowners who are 65 or older, or disabled, now receive an additional $60,000 school district exemption, bringing the school exemption total to $200,000 for those homeowners.

Texas also has a 10% annual cap on increases to the appraised value of a qualified residence homestead. That cap helps long-term owners, but it does not prevent taxes from feeling expensive when someone buys into the market at today’s prices.

One practical point matters: homeowners generally need to apply for exemptions with the county appraisal district, and the usual deadline is before May 1. Missing or delaying that filing can mean paying more than necessary for a year.

Rising Insurance Premiums in 2026

Nobody talked about this much a few years ago, but Texas homeowners insurance is now one of the biggest affordability issues in the state. Dallas-Fort Worth has one of the highest insurance burdens in Texas, behind or alongside Amarillo depending on the measure.

The numbers are not small:

The average Texas home insurance premium in 2026 is about $4,085 per year

The national average is about $2,543 per year

Dallas-area quotes vary widely, but many buyers should budget roughly $3,500 to $5,000+ per year, depending on the home, roof age, deductible, carrier, coverage level, and ZIP code.

The drivers are severe weather, hail, wind claims, roof losses, and rising rebuilding costs. DFW sits in a major hail-risk region, and roof claims are a huge part of the insurance story. Some older homes can be harder or more expensive to insure, especially if the roof is aging or the carrier sees repeated storm risk.

Auto insurance follows a similar pattern. DFW drivers deal with heavy traffic, hail exposure, uninsured motorists, and vehicle-theft risk in certain ZIP codes. For many households, the combined home and auto insurance bill can eat into the income-tax savings faster than expected.

For a household budget, that means adding roughly $2,000 to $3,000 per year compared with a similar home in a lower-risk state. The income-tax savings often absorb it, but the margin is not as clean as the headline sounds.

Housing Costs Compared With Coastal Markets

The “Dallas is cheap” narrative still leans on old prices. The 2026 market is different.

In Dallas, recent market data shows:

The median sold price is about $408,000

The median listing price is about $435,000

The median rent is about $1,665 per month

The average one-bedroom apartment rent is about $1,400 per month, depending on source and neighborhood

The suburbs can be much higher. Collin County’s median listing price is around $500,000, Frisco is around $700,000, Plano is around $538,000, and Celina is around $585,000.

Compare that with other markets:

Los Angeles County median listing price is about $950,000

New York City average one-bedroom rent is about $4,100 per month

Chicago median listing price is about $355,000

Denver median listing price is about $541,000

Dallas is genuinely cheaper than Los Angeles, New York City, San Francisco, and Denver on most housing comparisons. Chicago is the tricky one. Chicago can still be cheaper for buyers, depending on the neighborhood, although property taxes and state income tax change the full picture.

For renters, Dallas is much easier to defend. Renters get most of the Dallas affordability advantage without taking on property tax, roof risk, or homeowners insurance. A renter moving from New York or Los Angeles to Dallas can see the savings immediately in the monthly budget.

Utilities, Groceries, and Daily Living Expenses

The smaller categories matter too. Dallas is not expensive across the board, but it is not low-cost in every category.

Here is where Dallas lands relative to the national average:

Housing: 8% below national average

Utilities: 16% above national average

Groceries: 1% below national average

Healthcare: 4% above national average

Clothing: 6% above national average

Entertainment and personal services: 6% above national average

Transportation: below the national average in this dataset, though car dependency still matters

The utility number deserves attention. Texas summers are long, hot, and expensive. Air conditioning can run hard from June through September, and many households see summer electric bills jump sharply.. Texas does have a deregulated electricity market, so you can shop providers. Choosing the wrong plan can cost hundreds of dollars a year. Choosing the right one can soften the summer-bill shock.

Sales tax is also part of the equation. Dallas has an 8.25% combined sales tax rate in 2026. That is not unusual for a big U.S. city, but it still matters because Texas relies more heavily on consumption taxes and property taxes instead of state income tax.

Comparing Dallas to Los Angeles

For a single filer earning $150K and buying around a $500K home, Dallas usually wins, but not by as much as people expect.

Category

Los Angeles

Dallas

State income tax

High, based on California brackets

$0

SDI charge

1.3% of wages, no wage ceiling

$0

Property tax

Often lower for long-term owners under Prop 13

Often higher as a percentage of value

Home insurance

Varies, but often lower than North Texas for standard risk

Often higher because of hail and storm risk

Auto insurance

Expensive

Also expensive in many ZIP codes

Bottom line

Baseline

Usually cheaper, but not automatic

Renters moving from Los Angeles to Dallas usually save much more. A Dallas one-bedroom averages around $1,400, while Los Angeles averages around $2,180 for a one-bedroom apartment. That alone can save roughly $9,000+ per year before taxes.

Comparing Dallas to New York City

New York City to Dallas is the clearest cost drop for many households. NYC rent, city income tax, state income tax, and daily living costs are all heavy.

A New York renter moving to Dallas can often cut rent by thousands per month. But there is a lifestyle trade-off. New York offers walkability and transit. Dallas is far more car-dependent, so newcomers may add a car payment, insurance, gas, tolls, parking, and maintenance.

Even with that added car cost, Dallas usually comes out ahead financially for most NYC movers. The bigger question is whether the lifestyle change works.

Comparing Dallas to Chicago

This is the comparison that surprises people. Chicago has lower median listing prices than Dallas, stronger public transit, and many neighborhoods where buyers can get more home for less money.

But Illinois has a 4.95% flat income tax, and property taxes in the Chicago area can be high. The savings from moving to Dallas are smaller here than they are for someone leaving California or New York. For some households, Chicago may actually be cheaper on pure housing cost. Dallas wins more often on job growth, taxes, newer housing stock, and long-term metro growth.

Comparing Dallas to Denver

Denver is a more straightforward comparison. Colorado has a flat 4.4% income tax, and Denver home prices remain higher than Dallas in many comparable areas. A $150K earner can save about $6,600 per year in Colorado state income tax alone by moving to Texas, before property tax and insurance differences.

Insurance is not a clean win either way because both regions deal with hail. But for many buyers, Dallas still comes out cheaper because the housing entry point is lower.

Who Benefits Most From Moving to Dallas

Here is who tends to save the most:

Big winners:

Renters at almost any income level, especially those leaving coastal markets

High earners buying homes under about $600K

Remote workers keeping coastal salaries

Business owners with pass-through income

Retirees with modest taxable income, since Texas does not tax Social Security or retirement income at the state level

Moderate beneficiaries:

Middle-income families buying homes between $400K and $700K

People moving from California, New York, or Illinois for a similar salary

Buyers who file their homestead exemption on time

Households that shop insurance and electricity plans carefully

Likely break-even cases:

Buyers purchasing homes above $800K

Long-term California homeowners protected by Prop 13 who sell and rebuy in Texas

People moving from Chicago or other relatively affordable Midwest metros

Households with multiple cars and high insurance costs

Potentially higher-cost cases:

Retirees with expensive paid-off California homes who buy expensive Texas homes

Buyers who forget to file the homestead exemption

Buyers purchasing older homes with roof, foundation, or insurance issues

Luxury buyers who assume Texas property taxes will be low because the state has no income tax

The Final Verdict on Relocation Costs

Dallas is cheaper than the coastal markets people are usually leaving, but the savings are not automatic. The income-tax advantage is the biggest reason the math works. Property tax and insurance are the biggest offsets.

A simple way to estimate it:

Take your projected income.

Subtract what you would pay in your current state income tax.

Add back the higher Texas property-tax burden.

Add the likely insurance difference.

Then compare housing costs honestly, not emotionally.

For most households earning above $100,000 and buying under $600,000 to $700,000, Dallas still pencils out. For renters, the move is usually strongly favorable. For buyers above $1 million, the math gets much closer than the headlines suggest.

The good news is that none of this requires guessing. County appraisal districts publish tax information. Insurance quotes are free. Electricity plans can be compared before move-in. Take-home-pay calculators are easy to run. The people who get burned are usually the ones who trust the “Texas is cheap” narrative instead of doing the math.

Once the numbers work on paper, the next variable is execution. A move to Dallas is not just a truck and a closing date. It can involve HOA rules, elevator reservations, gated-community access, storage timing, utility setup, and a few days of overlap between homes. Hiring a Dallas moving company that understands both interstate relocations and local DFW moves can make that transition much less stressful.

Texas is probably cheaper than where you came from. But the margin is smaller than the internet makes it sound, and the savings only happen when the numbers are handled carefully.

Buying a home in 2026 is different than it was just a few years ago. While everyone is focused on mortgage rates and cosmetic upgrades, the real financial impact comes from elsewhere. Insurance costs, tax assessments, and local policy changes are now the deciding factors in what you’ll really pay and what that asset is worth five years from now.

Climate risks impact insurance costs. Tax structures and infrastructure demands affect monthly payments. Local zoning decisions can change entire neighborhoods. A house may look perfect during a showing, but the infrastructure behind it matters just as much.

Water lines, risk maps, development plans, and policy changes all carry long-term consequences. Smart buyers look beyond surface appeal and ask the hard questions.

Before you make an offer this year, consider these four practical realities that could determine whether your purchase remains secure and a good long-term investment.

Climate Risk Is Now a Pricing Factor

For years, climate risk was an afterthought in real estate decisions. Buyers focused on location, schools, and square footage, while environmental exposure felt distant. That is changing fast as new data impacts home values.

A recent CNBC report paints a tough picture. By 2055, climate change could cut nearly $1.47 trillion from total U.S. home values. The impact isn’t limited to beachfront properties. About 84 percent of homes nationwide are expected to see at least some decline in value as climate risks become more visible.

This shift is already underway. Properties in wildfire-prone regions, coastal flood zones, and areas facing extreme heat are seeing insurance premiums rise sharply. In some markets, insurers have pulled out entirely. This forces homeowners into much more expensive coverage options.

What this means for buyers is that climate exposure is now a financial factor, not just an environmental one. Two similar homes can carry very different long-term costs depending on flood history, fire risk, and storm frequency.

Don’t even think about making an offer until you’ve checked the flood maps and secured a firm insurance quote. If premiums are sky-high or coverage is limited, consider that a major warning sign. Expensive or unstable coverage can make the home harder to sell down the road.

Aging Water Infrastructure

Drinking water infrastructure, particularly aging pipes, is a critical factor in older cities and suburbs. Across the United States, much of the water system was built decades ago and is now approaching or exceeding its intended lifespan. Experts warn that aging pipes, insufficient funding for maintenance, and old lead service lines continue to pose risks to public health.

Lead contamination remains a real issue in older neighborhoods. Replacing service lines is expensive, and responsibility sometimes falls partly on homeowners. Breaks in aging mains can also cause service interruptions and emergency repairs that impact entire blocks.

Recent local reporting in Nashville highlighted ongoing efforts by Metro Water Services to identify and replace remaining lead water lines. That example illustrates how cities are grappling with infrastructure built generations ago.

In areas undergoing upgrades, homeowners may consider options such as water filter installation in Nashville as a better safeguard. Similar protective measures may also be explored in other cities while replacement programs move forward.

On the other hand, before purchasing, review the city’s annual water quality report and ask about the age of the neighborhood water mains. Confirm whether the property has a lead service line and whether replacement is scheduled. Infrastructure reliability directly affects both health and property value.

Older Homes vs. New Builds in a Tight Market

New residential construction has not kept pace with buyer demand. As reported by National Mortgage Professional, builders are not launching enough new projects.

On top of that, ongoing affordability pressures are keeping many potential buyers on the sidelines. As a result, shoppers are increasingly turning toward older homes, not necessarily by preference, but by necessity.

The data shows that existing homes, particularly those built decades ago, now make up a growing share of transactions. Inventory in the new build segment remains limited. Higher construction costs and elevated mortgage rates have pushed many newly built homes out of reach for a large number of households.

Older homes often offer established neighborhoods, larger lots, and central locations that newer developments cannot always match. At the same time, they may carry aging systems, outdated wiring, or plumbing that requires significant upgrades.

The bottom line is that in today’s low-inventory market, age alone should not guide your decision. Careful inspection and realistic budgeting matter more than ever.

Zoning Changes and Future Development

Housing shortages are forcing policymakers to reconsider long-standing zoning rules. As reported by HousingWire, Texas offers a clear example of this shift. Like other parts of the Southeast, the state has experienced a major population surge.

U.S. Census data shows that between 2023 and 2024, Texas recorded the highest absolute population growth in the country. That rapid expansion has intensified pressure on housing supply and affordability.

In response, lawmakers and local officials are exploring zoning reforms that allow greater density. These changes include permitting duplexes, smaller lot sizes, and alternative housing types in areas once reserved for single-family homes. The idea is to unlock more supply without waiting for large-scale suburban expansion.

Zoning changes aren’t just paperwork, they hit your wallet. Sure, more density usually drives up property values and brings in better amenities. But it also changes the vibe of a street overnight. Don’t fly blind: pull the city’s master plan and check pending proposals before you commit. You don’t want a four-story complex popping up next door right after you move in.

FAQs

What is the biggest challenge in real estate right now?

The biggest challenge is affordability. Home prices, insurance premiums, property taxes, and borrowing costs have risen faster than incomes in many regions. This gap limits access for first-time buyers and increases financial strain for existing homeowners.

What does rezoning mean for homeowners?

Rezoning refers to a shift in how a piece of land is legally classified by local government. Zoning determines what can be built on a property like single-family homes, duplexes, or apartments. When zoning changes, the permitted use of that land changes as well.

How old is most US water infrastructure?

Much of the United States drinking water infrastructure was constructed in the late 19th and mid-20th centuries. Many pipes still in operation today are between 50 and 100 years old, and some systems in older cities are even older.

At the end of the day, buying a home in 2026 demands doing your homework. The decision stretches far beyond layout and location. A home’s long-term value now depends on factors that are easy to overlook but carry real consequences over time.

Homes do not exist in a bubble. Local regulations, city infrastructure, and regional growth all play a huge role in future property values.

The strongest purchases are made by those who examine the full context, not just the listing details. Careful research today reduces unpleasant surprises tomorrow. In this market, doing your research isn’t just extra work. It is the foundation of a solid investment.

Buying a house is a huge decision that entails a lot of due diligence. In fact, looking at a residential property for sale in Sydney is just a small part of the process of the homebuying process, which is why it’s also not uncommon to experience these common fears if you’re a first-time homebuyer.

You’re worried you won’t be able to afford a home

The average price of a house in Australia is at $1.045 million, according to the latest date from the Australian Bureau of Statistics. That number sounds like a lot, and unfortunately, not everyone can afford it, especially in a tough economy. But this is why buying a house is a decision that you don’t make overnight.

It’s something that you think about, save up for and really do your homework on before you make a move. Buying a house is one of the biggest purchases that you’ll ever make in your life, and that thought could be overwhelming. But if you have the right plan, you can definitely afford your first home over time.

You’re worried about taking on debt

The truth is, only a handful of people buy their houses in cash outright. Even the richest people still choose to buy their house with a loan because it gives them time to pay off the price instead of making one huge purchase, which could drain their savings. Now, there’s nothing wrong with taking on a mortgage if you don’t have the means to pay in cash.

You just need to make sure that you can afford the monthly payments without destroying the rest of your budget. This is also why you should only purchase a property when you’re already financially stable, because you won’t have a hard time sticking to your budget while making payments.

You’re worried about choosing the wrong home

Buying a home isn’t easy. You need to consider a lot of things before you can make that final decision, and even then, you might still choose the wrong property. Now if you want to avoid this mistake, it’s very important that you know what you want in a house first. You’ll have a lot of options once you start looking, so you need the right direction to avoid getting sidetracked from what matters most to you. Never rush the homebuying process.

Take as much time as you need and don’t look for a house when you’re not in the right headspace. Do your research, compare prices, look at different options and work with the pros to ensure that you land on a property that fits your exact needs.

You feel anxious about commitment

Buying a property is a long-term commitment. After all, you’re spending a lot of your money on a house that you plan to live in for years to come. As a first-time buyer, it’s normal to feel anxious about commitment, which is why it’s also very important to take your time. Trust your instincts, but don’t second-guess yourself.

There is no perfect time to buy a house. If you feel like it’s the right time to commit to a property, then by all means go for it.

You’re afraid you’re paying more than the home is worth

There are many properties out there that you can buy. Some are affordable, and some are way out of your budget. Now it’s not easy to commit to paying such a huge amount of money, even if you’re buying the cheapest house on the lot.

You’ve worked hard for your money, after all. But if you’re afraid that you could be paying more than a home is worth, you can take comfort in the fact that each home is carefully appraised and inspected before it goes on the market.

This is also why it pays to work with professionals like us who have a strong inventory of residential properties that are fairly priced. We don’t sugarcoat things because we know how important buying a house is for clients. So if you’re looking for a property that offers the right value, get in touch with us.

Buying a home is likely the biggest financial decision you will ever make. The excitement of finding your dream property can quickly turn to stress when you realize how complicated the financing process actually is.

Most buyers spend hours researching neighborhoods, school districts, and property features. Yet many spend surprisingly little time understanding their mortgage options. This oversight can cost thousands of dollars over the life of a loan.

Working with the right professionals makes all the difference. A skilled mortgage broker can navigate the lending landscape on your behalf, potentially saving you both money and headaches along the way.

Understanding the Role of a Mortgage Broker

Mortgage brokers act as intermediaries between you and potential lenders. Unlike bank loan officers who can only offer their institution’s products, brokers have access to multiple lenders and loan programs.

This access translates into options. Different lenders specialize in different borrower profiles. Some excel with first-time buyers, others with self-employed individuals, and still others with investment property financing.

A broker’s job is to match your unique situation with the most appropriate lending solution. They evaluate your financial picture, understand your goals, and then shop the market on your behalf.

The relationship works similarly to how a real estate agent represents you in property transactions. You benefit from their expertise, relationships, and market knowledge without having to develop these yourself.

Why More Buyers Are Choosing Brokers

The mortgage industry has grown increasingly complex. New loan products emerge regularly, and qualification requirements vary significantly between lenders.

Trying to navigate this landscape alone is like exploring a foreign city without a map. You might eventually find your destination, but you will waste time and probably miss better routes along the way.

When you work with a Go mortgage broker instead of going directly to a single bank, you gain access to wholesale rates that are often unavailable to individual consumers. Brokers leverage their volume relationships to negotiate better terms.

The time savings alone justify working with a professional. Instead of completing multiple applications and gathering documents repeatedly, you work with one broker who handles distribution to various lenders.

Communication also tends to get a lot easier. A good broker keeps you informed throughout the process, translating industry jargon into plain language and setting realistic expectations.

What to Look for in a Mortgage Professional

Not all brokers offer the same value. Experience matters, but so does specialization and communication style. Finding the right fit requires some homework.

Start by asking about their lender relationships. A broker with access to dozens of lenders offers more options than one working with just a handful. More options generally mean better chances of finding ideal terms for your situation.

Image Source: freepik.com

Inquire about their experience with borrowers like you. First-time buyers have different needs than seasoned investors. Self-employed applicants face unique documentation challenges. You want someone who has successfully navigated situations similar to yours.

Check reviews and ask for references. Past client experiences reveal how brokers handle challenges, communicate during stressful moments, and deliver on their promises.

Transparency about fees should be non-negotiable. Reputable brokers explain exactly how they are compensated and disclose any potential conflicts of interest upfront.

The Importance of Local Market Knowledge

Real estate markets vary dramatically from one area to another. Property values, buyer competition, and lending conditions all differ based on location.

Brokers with strong local presence understand these nuances. They know which lenders perform well in specific markets and which ones tend to cause delays or complications.

This localized expertise extends to relationships with other professionals. You might consider a well-connected Mortgage Broker Hawthorn, for example, would have established connections with local real estate agents, attorneys, and appraisers.

These relationships smooth the transaction process. When professionals know and trust each other, communication flows better and problems get resolved faster.

Local brokers also understand regional economic factors that affect lending decisions. Employment trends, development plans, and market cycles all influence how lenders evaluate properties in specific areas.

Timing Your Mortgage Application

When you apply for financing matters more than most buyers realize. Interest rates fluctuate daily, and your personal financial situation can change quickly.

Getting pre-approved before seriously shopping gives you several advantages. You know exactly what you can afford, sellers take your offers more seriously, and you can move quickly when the right property appears.

Pre-approval also reveals any issues with your credit profile or documentation. Discovering problems early leaves time to address them before they derail a purchase.

Image Source: freepik.com

However, pre-approval letters typically expire after 60 to 90 days. If your home search extends longer, you may need to refresh your approval and potentially lock in different terms.

Work with your broker to develop a timeline that aligns with your search plans. They can advise on rate lock strategies and help you understand market conditions.

Common Mistakes to Avoid

Many homebuyers undermine their own mortgage applications without realizing it. Simple mistakes can delay closings or result in less favorable terms.

Avoid major purchases before closing. That new car or furniture set might seem exciting, but the additional debt affects your qualification ratios. Wait until after closing to make big purchases.

Do not change jobs during the mortgage process unless absolutely necessary. Lenders want to see stable employment history. Even a lateral move to a similar position can complicate verification.

Keep cash deposits traceable. Large deposits that cannot be documented raise red flags for underwriters. If someone gives you money for a down payment, work with your broker to handle it properly.

Stay responsive to document requests. Delays in providing paperwork slow down the entire process. When your broker or lender asks for something, prioritize getting it to them quickly.

Building Long-Term Relationships

The best mortgage professionals think beyond single transactions. They want to help you build wealth through strategic real estate decisions over time.

As your circumstances evolve, your financing needs will change too. Growing families need different homes than young professionals. Investors seek different terms than primary residence buyers.

A broker who understands your long-term goals can advise on refinancing opportunities, investment property financing, and equity strategies. For instance, For instance, working with a mortgage broker East Tamaki could provide ongoing guidance as your portfolio expands.

These relationships also pay dividends through referrals. When friends and family need mortgage help, you can confidently point them toward someone you trust.

Stay in touch with your broker even after closing. Market conditions change, and opportunities to improve your position may arise. A quick annual check-in keeps the relationship going and keeps you informed.

Questions to Ask Before Committing

Before selecting a mortgage professional, conduct thorough interviews. The answers reveal both competence and compatibility.

Ask how they will communicate with you throughout the process. Some buyers prefer frequent updates while others want to hear only about major developments. Make sure styles match.

Inquire about their typical timeline from application to closing. Experienced brokers can provide realistic estimates based on current market conditions and your specific situation.

Request a breakdown of all costs involved. Beyond the interest rate, understand origination fees, discount points, and third-party charges. The lowest rate does not always mean the lowest total cost.

Ask what happens if problems arise. Every transaction hits bumps. How the broker handles challenges reveals their true value.

Making Your Decision

Choosing the right mortgage broker sets the tone for your entire home buying experience. Take this decision seriously, but do not let it paralyze you.

Trust your instincts about communication and professionalism. You will be sharing sensitive financial information and relying on this person during stressful moments. Comfort and confidence matter.

Compare multiple options before committing. Even a brief conversation with two or three brokers helps you get a feel for what good service looks like.

Remember that the cheapest option is not always the best value. Expertise, responsiveness, and problem-solving ability often prove more valuable than small fee differences.

Moving Forward With Confidence

The mortgage process does not have to be overwhelming. With the right professional guidance, it becomes manageable and even educational.

Take time to understand your options before jumping in. Knowledge empowers you to ask better questions and recognize good advice when you hear it.

Your home purchase deserves the same careful attention to financing that you give to choosing the property itself. Both decisions affect your financial future for years to come.

The right broker makes this journey smoother, more successful, and far less stressful. Start your search today and take the first step toward your new home.

Purchasing high-end real estate is very different from purchasing a standard home. The stakes are higher, systems are more complex, and the expectations are greater. Whether you’re looking for a waterfront villa, a modern smart home, a penthouse with a view, or a spacious private estate, the process requires careful planning. Here is how to find a luxury home that matches your lifestyle and long-term goals.

Define What ‘Luxury’ Means in Your Market

Luxury looks different depending on the location. A high-end home in Dallas will offer very different features from one in New Jersey. Before starting your search, understand what “luxury” typically includes in your target market. Common features include:

Premium materials like marble, quartz, and hardwood

Smart home technology and energy-efficient systems

Large square footage or open layouts

Resort-style outdoor areas

Secure gated entrances

Top-tier school districts or exclusive neighborhoods

Knowing the market helps you spot genuine value instead of paying for features that don’t justify the price.

Study the Market Before Making Any Decisions

Luxury real estate operates differently from the general market. Inventory can shift quickly, and certain areas stay competitive year-round. You need to track recent sales, pricing trends, and upcoming developments.

Since you are targeting New Jersey, working with a real estate agent in Essex County, NJ can give you access to off-market homes, neighborhood insights, and proper pricing guidance.

The more you know about current demand, the better prepared you’ll be when the right property becomes available.

Get Your Financials Organized Early

Luxury homes often come with stricter lending requirements. Even all-cash buyers benefit from organizing documentation early, since high-value transactions tend to involve more verification. Prepare ahead by:

Checking your credit health

Reviewing recent tax returns

Gathering proof of income

Getting pre-approved for a jumbo loan, if needed

Speaking with lenders who handle high-value properties

Being financially ready puts you in a stronger negotiating position and speeds up the offer process.

Focus on Long-Term Value

Not every expensive property will hold its value. When buying luxury real estate, the lifestyle and long-term potential matter just as much as the home’s features. Ask yourself:

Is the area stable and in demand?

Are the schools strong, even if you don’t need them?

Is the neighborhood improving or declining?

Will the home’s style stay appealing over time?

Is the location convenient for your lifestyle?

A luxury home in a strong area is far more likely to appreciate.

Inspect Craftsmanship Closely

A luxury home should feel solid, well-built, and thoughtfully finished. Stunning photos can hide rushed workmanship, so take your time during walk-throughs. Pay attention to:

Cabinet quality and hardware

Flooring transitions

Window construction and seals

Finish consistency

Water pressure and plumbing

Insulation and noise control

If something feels cheaply done, it often signals deeper issues.

Use an Inspector Experienced With Luxury Homes

Not every inspector understands how to evaluate high-end features, and luxury homes often include advanced systems that require specialized knowledge. An experienced inspector will know how to assess:

Smart home automation

High-end kitchen appliances

Spa features, steam rooms, or saunas

Custom HVAC setups

Wine storage

Pools, outdoor kitchens, and terraces

The right inspector can protect you from expensive surprises later.

You Have to Be Patient

Luxury home buying isn’t usually a quick process. Inventory is lower, and the perfect property might take time to hit the market. Rushing into a property you’re unsure about often leads to regret. Patience helps you wait for:

The right location

A layout that truly fits your lifestyle

A property with long-term value

A price that aligns with the market

In the luxury tier, patience pays off.

Think About How You Actually Live

luxury home should feel effortless, not overwhelming. Focus on the lifestyle you want rather than just size or features. For example:

If you entertain often, focus on kitchens and outdoor spaces.

If you work from home, prioritize office space and privacy.

If you value peace, choose a quieter neighborhood over a busier one.

If convenience matters, consider proximity to key amenities.

Luxury should make your daily life easier, not more complicated.

Having the Purchase in Mind, But Not Rushing it

Buying a luxury property is exciting, but it requires preparation, patience, and a clear understanding of what you want. With the right research, professional support, and attention to detail, you can find a home that feels both impressive and practical for your lifestyle.

With the VA OTC Construction Loan benefit, qualified active-duty and military Veterans can apply for a home mortgage loan to finance the construction of a new home. The VA One-Time Close (OTC) Construction Loan process is designed to simplify and expedite the home construction process for eligible Veterans by combining the financing for the lot, the construction phase, and the permanent mortgage into a single loan and a single closing.

Here is what you can expect from conversion to permanent loan, when Security America Mortgage is your lender:

Phase 1: Qualification & Pre-Approval

The initial steps are to determine the Veteran’s eligibility and ensure the builder and project qualify.

Step

Summary

Security America Mortgage Focus

Application

Focus on submitting the initial mortgage application.

Expediting the pre-qualification process.

Provide COE

The Veteran’s Certificate of Eligibility (COE) shows their VA home loan entitlement.

Determine the Veteran’s entitlement to VA benefits.

Borrower Qualification

Review of the borrower’s financial situation, including income, credit score (typically 620+ FICO), and DTI ratio, to determine the maximum loan amount.

Utilizing automatic underwriting to expedite the pre-qualification process.

Builder Acceptance

The builder must meet VA standards and be approved by the lender.

Approving the builder based on the lender’s experience and financial stability requirements, using clear checklists and guidelines.

Contract & Budget

Borrower and builder establish a contract including the project budget plan (cost for lot purchase and/or cost to build the home).

Reviewing and approving all signed contracts and plans.

Phase 2: The Single Closing

This is the important point of the “One-Time Close.”

Process

Description

Security America Mortgage Focus

Appraisal & Valuation

Your home’s value is appraised by a VA-approved professional based on the finished value (after construction). The VA issues a Notice of Value (NOV).

There is no cost to apply.

Loan Underwriting

The lender reviews all documents (COE, contract, plans, title, borrower financials) and issues the final loan commitment.

Locking-in the construction loan permanent terms (rate, term, payment) prior to construction start.

Closing

The borrower executes a single set of closing documentation for both the construction and permanent loans. The VA funding fee is charged at closing.

Originating the loan and ensuring construction draws are disbursed from escrow.

Phase 3: Construction and Permanent Loan Terms

Following closing, the home is built, and the loan automatically converts from a construction loan to a permanent mortgage.

Step

Description

Security America Mortgage Focus

Loan Draws

Loan proceeds are disbursed to the builder in scheduled draws as construction advances (e.g., foundation, roof on), paid through an escrow account.

Accessing and monitoring the builder’s progress at each point of completion before any funds are released.

Construction Period Payments

The borrower is not required to make principal & in many cases interest payments on the construction loan during this time period (though they may choose to).

Managing the escrow and draw process to facilitate timely withdrawals and allocations.

Final Completion & Conversion

Once construction is complete, a final inspection confirms all work complies with VA standards and the approved plans. There is no second closing.

Ensuring a smooth transition to the permanent mortgage terms without modification to the final loan amount based on the Loan-to-Value (LTV).

The Advantages of Security America Mortgage Program:

One-Time Close: Pay once– saving you money and the headaches of a second closing.

Rate Lock: The long-term rate is locked in at the initial closing, so you’ll know what your permanent payment will be.

Rate Change Option: Security America Mortgage can offer a velocity change rate if market conditions improve during the construction period, potentially allowing you to secure a lower interest rate without refinancing (this is subject to current lending guidelines).

Why Veterans Like This Program

Streamlining: One loan, one closing, one transaction.

VA Benefit Eligible: Access to Veteran-friendly terms and cost savings associated with the VA benefit.

Predictability: The final price tag is established upfront with a pre-approved builder and a fixed-price contract (subject to builder contract terms).

Personalized Service: As a Veteran, you receive custom underwriting and dedicated service from an experienced lender like Security America Mortgage.

Next Steps

If you’re a Veteran that wants to build the house of your dreams:

Contact Security America Mortgage to verify you qualify and select a builder.

Choose a VA-Approved Builder and finalize your Plans, Budget, & Contract.

Submit your COE, plans, and builder for approval as required by lender.

Close once, and proceed with construction knowing the permanent financing is ready.