When veterans return from service, many find themselves navigating a new battlefield, which is the challenge of civilian life. One of the most empowering transitions a veteran can make is moving from renting to owning, and for those with a vision for financial stability and long-term wealth, purchasing a multi-unit property can be a powerful step. What many veterans don’t realize is that they may be able to take that step with no money down.

Owning a multi-unit property isn’t just about having a place to call home. It’s also about creating a passive income stream and taking charge of your financial future. For veterans, the opportunities are even better than for most people.

Just like an individual took advantage of a purchasing a duplex, living in one unit and then years later, having the property quadruple in value.

The VA Loan Advantage – More Than Just a Single Family Home

The U.S. Department of Veterans Affairs (VA) loan is one of the most powerful tools available to eligible service members, veterans, and some surviving spouses. The hallmark of the VA loan is the ability to purchase a home with a zero-down payment and no private mortgage insurance (PMI). One point that’s often overlooked is that the VA loan isn’t just for single-family homes.

Many are unaware that VA loans can be used to purchase properties with up to four residential units, as long as the veteran intends to live in one of them. That opens the door to acquiring a duplex, triplex, or even a fourplex with no down payment required.

Think about what that means in practice. A veteran could purchase a fourplex, live in one unit, and rent out the other three. The rental income from those units could potentially cover the mortgage, taxes, insurance, and even provide additional cash flow. It’s a classic real-estate investing strategy called “house hacking,” and the VA loan makes it uniquely accessible to veterans without needing to first accumulate tens of thousands of dollars in savings.

Requirements and Realities

Of course, there are still rules and requirements. The property’s gotta be your primary residence, meaning you’ll need to live in one of the units for at least a year. It also has to pass the VA appraisal for safety, livability, and resale value.

Another important consideration is debt-to-income ratio (DTI). While the VA is generally flexible compared to conventional lenders, a veteran’s DTI still needs to be within acceptable limits.

If you’re purchasing a multi-unit property and can show that it will generate rental income, that income can be used to help qualify for the loan. VA guidelines allow a portion of the projected rental income from the other units to be counted toward your income, which may help you qualify for a larger loan amount.

This gives veterans a strong foundation for entering the world of real estate investing, allowing them to live affordably while building equity in a property that also generates income.

Already Own a Home? There’s Another Path

What about veterans who already own a primary residence?

This is where alternative financing options come into play. One of the most relevant tools for veterans (or anyone) looking to grow their real estate portfolio is the Debt Service Coverage Ratio (DSCR) loan.

Unlike traditional mortgages that focus on tax returns, pay stubs, and employment history, a DSCR loan looks at the property’s income potential. If the projected rent covers the monthly mortgage (usually a DSCR of 1.0 or higher), you’re in business, even without W-2 income.

For veterans who already have a home but want to build a rental portfolio, this can be a game changer. It opens the door to buying single-family rentals or multifamily properties without jumping through all the hoops of conventional lending. That’s especially valuable for vets who are retired, self-employed, or relying on pension income.

Building Wealth with a Mission

For many veterans, there’s a desire not just to live securely but to thrive. That starts with financial freedom. Real estate is one of the most proven vehicles for building long-term wealth, and veterans have a serious head start thanks to the VA loan.

Imagine a scenario where a veteran purchases a four-unit property with no down payment. They move into one apartment, rent out the other three, and within a few years have built up equity, improved the property, and perhaps even used the income to fund another investment. Thanks to the VA loan, and later shifting into DSCR or other investor-friendly financing, that same veteran can move from simply living in the property to owning a portfolio of them over time.

Points to Keep in Mind

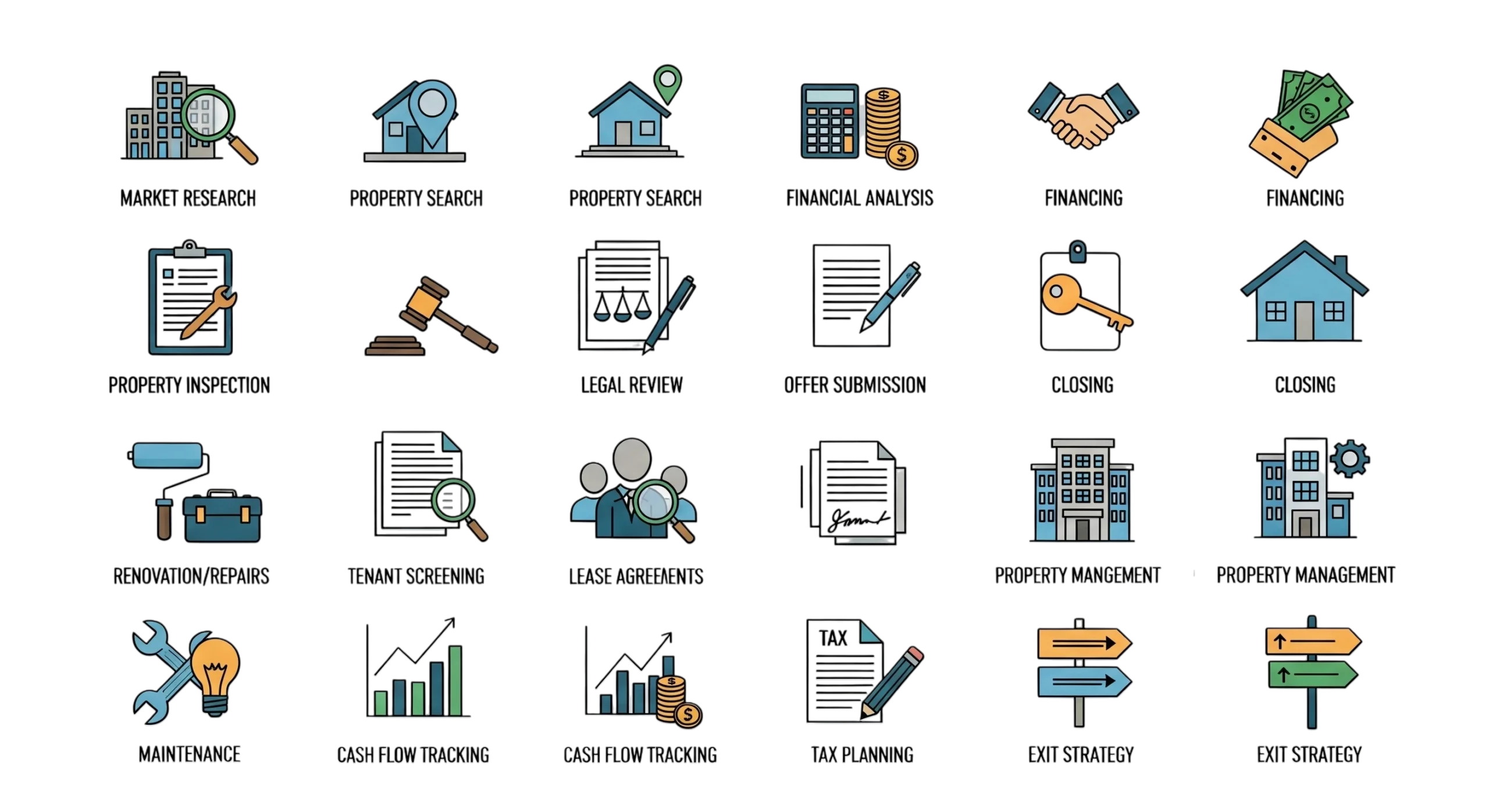

- Do your homework on the local rental market. Not all multi-unit properties are good investments.

- Partner with a lender and real estate agent who understand VA loans and DSCR loans. Experience matters.

- Factor in maintenance and vacancies. Even with multiple units, there will be unexpected costs and income gaps.

- Get preapproved early so you understand your borrowing power and what properties make sense for your situation.

Veterans have given so much through their service. It’s only fitting that they have access to tools that help them create stable, prosperous futures. Whether it’s buying a fourplex to live in with no money down or leveraging rental income through a DSCR loan for an investment property, the pathway to real estate success is wide open.

The first step is recognizing that these opportunities exist and then taking action. With the right strategy and support, real estate can become more than a dream for veterans, and turn into a reality that pays dividends for decades to come.