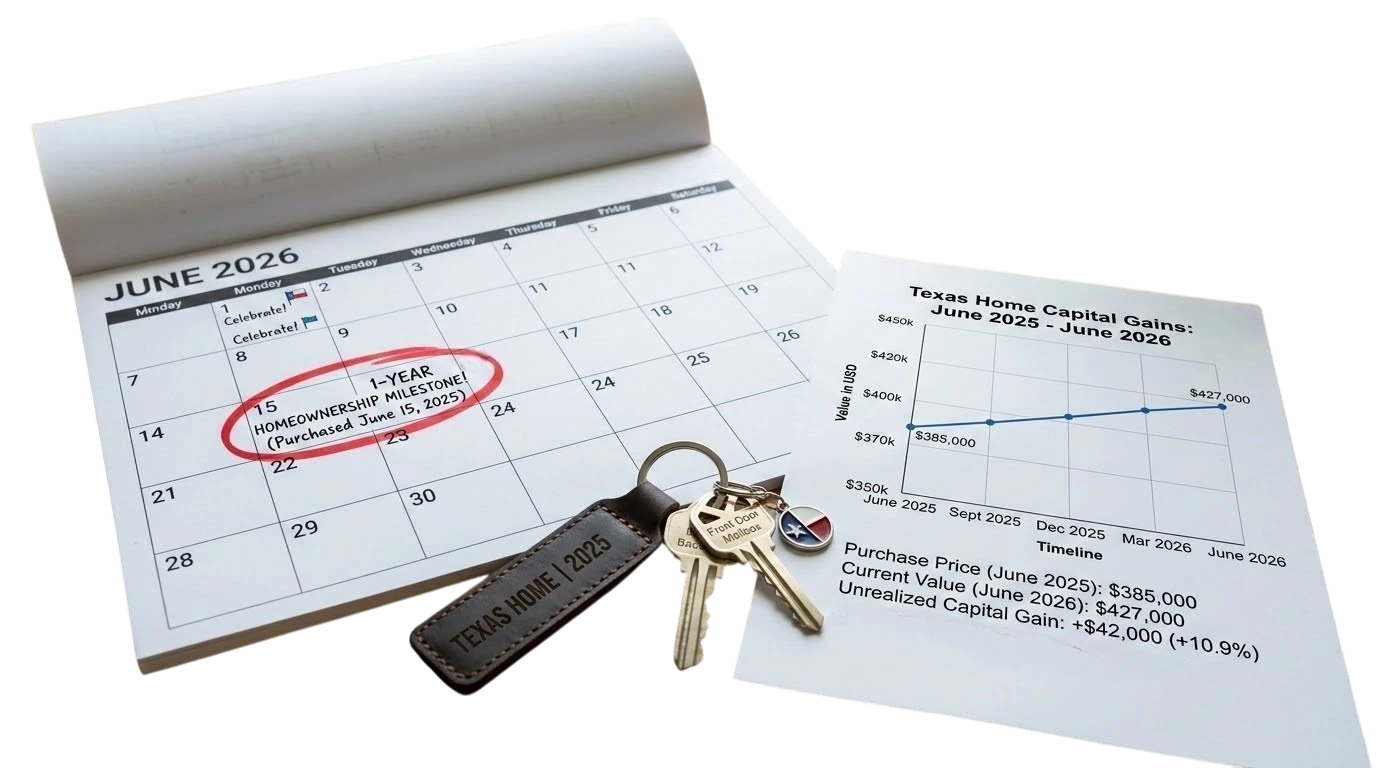

Dallas property values have shot up, leaving many owners with bigger gains than they expected. That can be great for your net worth, but it can also create a serious tax bill if you are not prepared. To keep more of your equity, you need to be just as smart about taxes as you are about the market.

Here’s how Dallas investors and homeowners can reduce their tax hit.

Use 1031 Exchanges

One of the most common strategies is using 1031 exchange services when selling an investment property. It allows you to defer capital gains taxes by rolling your sale proceeds into another investment property. In a fast-moving market like Dallas, that keeps more of your money working for you instead of sending a large chunk to the IRS right away.

The catch is the timeline. You have 45 days to identify a replacement property and 180 days to close. Because the Dallas market moves quickly, many investors start looking for their next property before they even list the one they plan to sell.

Track Every Improvement

Many owners leave money on the table by losing track of capital improvements. A new roof, HVAC system, kitchen remodel, or major repair can increase your cost basis. A higher basis can reduce your taxable gain when you sell.

Therefore, you should document everything and keep digital copies of invoices, permits, contractor bids, and receipts. Don’t guess, without a paper trail, the IRS may reject those costs, which means you could end up paying taxes on money you already spent.

Time Your Sale for Long-Term Rates

Timing can be the difference between a painful tax bill and a manageable one. If you sell a property you have held for less than a year, your gain is usually taxed at short-term capital gains rates, which are generally tied to your ordinary income rate. Holding the property for at least one year and one day can qualify you for long-term capital gains rates, which are often lower.

If you are only a month or two away from that one-year mark, waiting may be the smarter move, even if the market shifts a little in the meantime.

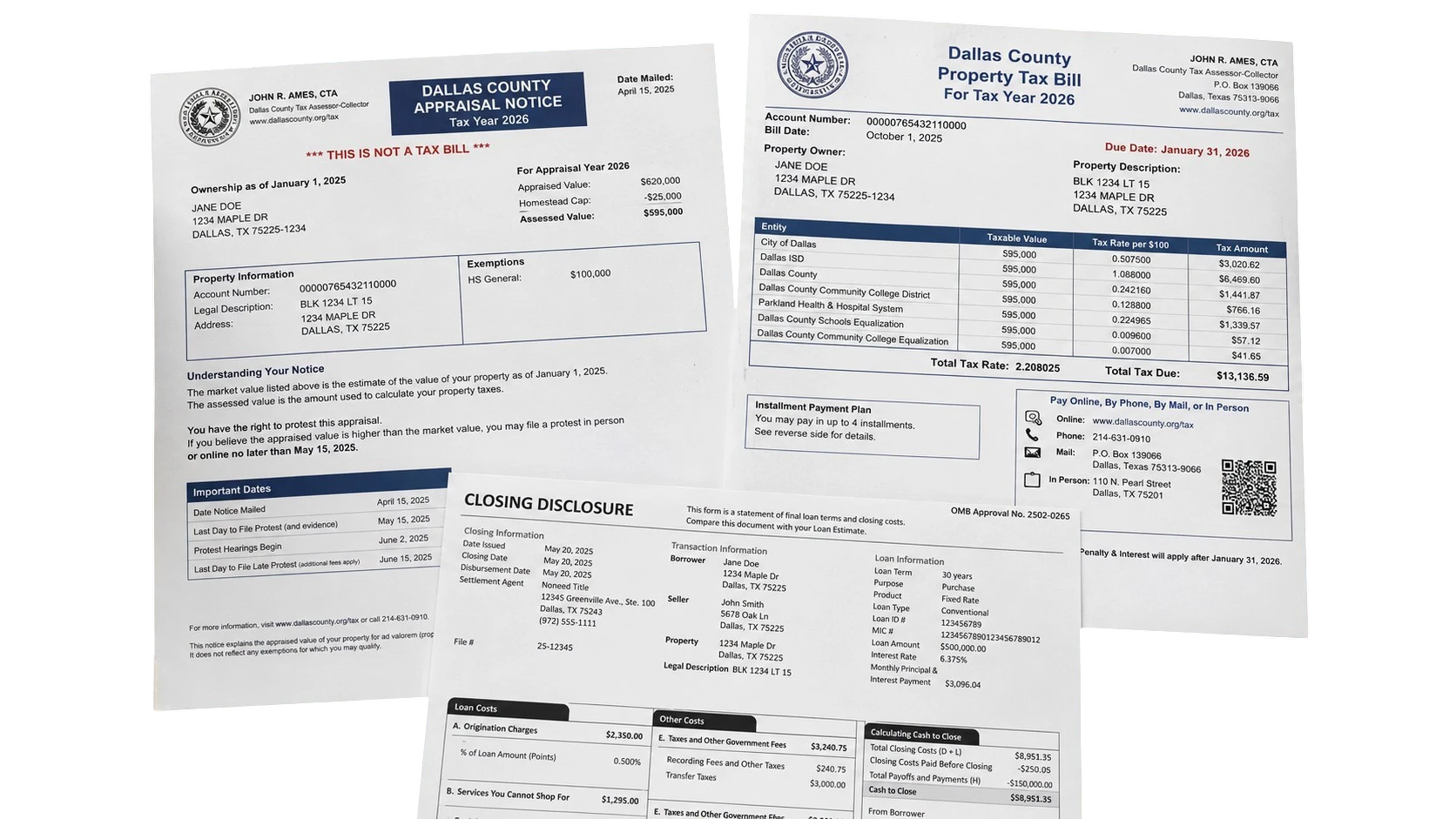

Understand Dallas Property Tax Cycles

Texas has no state income tax, but property taxes can still take a serious bite out of your cash flow. Dallas County values are reviewed regularly as part of the annual property tax cycle, and a sudden jump in appraised value can affect your numbers, especially if you own rental or investment property.

When selling, pay close attention to how property taxes are prorated at closing. Appraisal notices, protest deadlines, tax bills, and payment dates can all affect your bottom line. A poorly timed closing can leave you covering more of the year’s tax burden than expected.

Use Primary Residence Exclusion

If you are selling your home, the Section 121 exclusion may be your strongest tax break. If you have owned and lived in the home as your main residence for at least two of the last five years, you may be able to exclude up to $250,000 of gain if you are single, or up to $500,000 if you are married filing jointly.

With Dallas home prices climbing, many long-term homeowners are getting closer to those limits. If your gain exceeds the exclusion, review your improvement records, selling costs, and any business or rental use of the home with a tax professional before you sell.

Plan for Depreciation Recapture

Depreciation can be a valuable tax shield while you own a rental property, but it can come back into play when you sell. Depreciation recapture often catches investors off guard because it can reduce how much they actually walk away with after closing.

To manage this, you should budget for the hit by knowing your cumulative depreciation before you set your asking price. You might also consider a 1031 exchange because, in the right situation, a properly structured exchange can help defer depreciation recapture along with capital gains.

Work With Local Experts

The Dallas market moves fast, and the tax impact can move just as quickly. A strong sale price is only part of the win. What really matters is how much you keep after taxes, closing costs, and planning mistakes.

Before you sell, work with a CPA and a real estate professional who understand Dallas County tax rules, 1031 exchange timelines, and local closing practices. The right plan can help you protect more of your profit and avoid surprises at the closing table.