Before closing on your home, don’t forget about IRS Form 1099-S. It’s used to report real estate sales over $600 to the IRS. Sellers should know about possible tax implications, and agents need to understand what counts as “real property” to help avoid surprises. This guide explains when the form is needed, who files it, and common mistakes to watch for, and a checklist to keep things on track. Ensure your closings are done the right way.

Understanding Form 1099-S in Real Estate Transactions

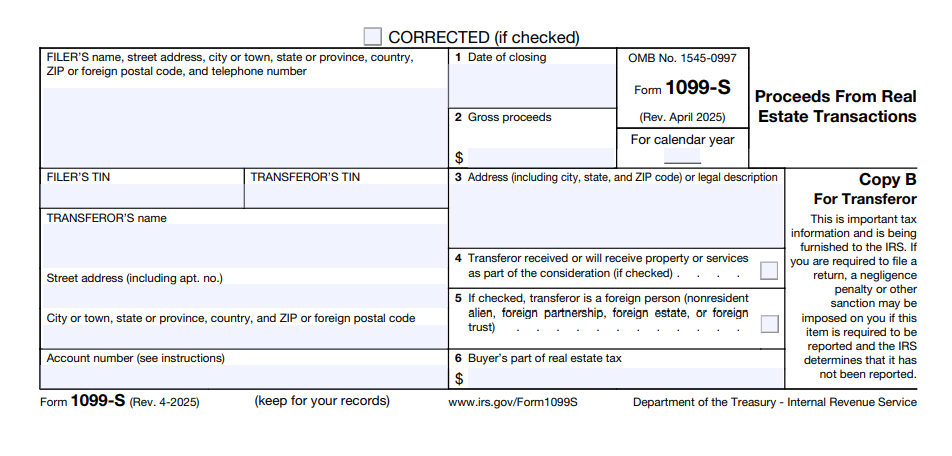

Form 1099-S, officially called Proceeds From Real Estate Transactions, is an important document used to report property sales or exchanges to the IRS. If you work in real estate closings as a broker, attorney, title agent, or escrow officer, you might be the one responsible for filing it. Put simply, the IRS wants to make sure income from real estate sales is properly reported and taxed.

The form covers various types of property, including:

- Land: This includes both developed and undeveloped land, as well as airspace rights.

- Permanent Structure: Residential, commercial, or industrial buildings that are considered inherently permanent.

- Condominium Units: This includes the unit itself, its fixtures, and any shared interest in common areas or land.

- Cooperative Housing Stock: If a buyer purchases shares in a cooperative housing corporation (as defined under Internal Revenue Service Section 216), the transaction must be reported.

- Standing Timber: Sales involving full ownership of standing timber must be reported.

When Is Form 1099-S Needed?

Form 1099-S must be filed for most real estate sales or exchanges considered reportable transactions under federal tax rules. Examples include:

- Sale of a principal residence (even if the gain may be excluded under Section 121).

- Sales made through land contracts.

- Forced sales due to foreclosure risk.

- Deals involving full ownership, leases longer than 30 years, or permanent easements.

However, there are key exceptions:

- Principal Residence Exclusion: Form 1099-S is not required if the property sold was the seller’s principal residence and the gain is fully excluded under Section 121 of the Internal Revenue Code.

Here’s what qualifies:

1. The sale price must be ≤ $250,000 for individuals or ≤ $500,000 for married couples filing jointly.

2. The seller must certify that the property was their principal residence and that there was no disqualifying use after December 31, 2008.

3. The seller must get this certification by January 31 of the next year and keep it for four years.

Even if Form 1099-S is issued, the seller may still exclude the gain on their tax return. In such cases, the transaction should be reported on Schedule D, and the exclusion claimed accordingly. - Corporate or Government Transfers: Sales by corporations, government entities, foreign governments, or international organizations are exempt.

- Non-Sale Transactions: Like inheritances, gifts, or refinancing that doesn’t involve buying property.

- Transfers to satisfy debt: This includes foreclosures, deeds in lieu of foreclosure, or when a property is abandoned.

- Small Transactions: If the total amount is under $600.

Real estate professionals must evaluate each transaction to determine whether an exception applies, especially for principal residence sales, to avoid over-reporting or non-compliance.

IRS Form 1099-S Deadlines and Penalties

The IRS has strict deadlines, and missing them can lead to serious penalties.

Here are the key dates to keep in mind:

- February 17 – Provide the seller with their copy of Form 1099-S. This gives the seller enough time to include the proceeds on their tax return.

- March 31 – Deadline to e-file Form 1099-S with the IRS. Most filers are required to e-file. If filing by mail, the deadline is typically February 28.

Missing these deadlines can result in costly penalties, anging from $60 to $660 per form. Depending on how late you file and how many forms are involved. The longer the delay, the higher the penalty, so it’s important to stay on top of these dates.

Who Is Responsible for Filing Form 1099-S?

The responsibility for filing usually falls on the person handling the closing, often the closing agent such as a title company, as listed on the Closing Disclosure.

Let’s break it down and see who is required to e-file 1099-S with the IRS If there’s no closing agent, responsibility follows this order:

- Buyer’s attorney (if involved in document preparation or fund transfer)

- Seller’s attorney

- Title or escrow company disbursing funds

- Mortgage lender with the primary lien

- Seller’s real estate broker

- Buyer’s real estate broker

- Buyer (if no other party qualifies)

This responsibility can be reassigned with a written agreement made before or at closing. The agreement must include names and addresses of the parties, be signed and dated, and retained for four years. Only one party is required to file for each transaction, and employees or agents may act on behalf of their company or principal.

In transactions without a title company (e.g., internal closings), real estate professionals ensure the form gets filed. Practical strategies include:

- Requesting the seller to complete Form W-9 for buyer submission

- Including a designation clause in the purchase agreement

- Giving the seller a pre-filled and addressed form to send to the IRS

How to Complete Form 1099-S, Step by Step

Filling out Form 1099-S accurately is crucial if you want to avoid penalties. Here’s what you’ll need to complete the form:

- Filer’s name, address, and TIN: Identifies the reporting party

- Seller’s name, address, and TIN: Must be obtained via Form W-9 (U.S. persons) or Form W-8 (foreign persons), with certification under penalty of perjury. Keep these records on file for at least four years.

- Closing date: The official date the transaction is finalized

- Gross proceeds: This includes the total amount received including cash, notes, and assumed liabilities. If the payment depends on future events like earnouts, report the highest amount that can reasonably be determined. Don’t deduct seller-paid expenses like commissions, report the full amount.

- Property address or legal description: Specific identification of the property sold

- Foreign seller indicator: Check if the seller is a nonresident, which may trigger withholding (see IRS Publication 515)

- Buyer-paid real estate tax: If the buyer paid any real estate taxes, include that amount here.

Real estate professionals should verify all the details at closing to make sure everything’s accurate and compliant.

How to Report Real Estate Sales on Your Tax Return

If a sale is reported on Form 1099-S, it must also be reported on the seller’s tax return, with reporting methods depending on the property type:

- Principal Residence: If the gain qualifies for the exclusion ($250,000 for individuals, $500,000 for joint filers), it may be tax-free. But if a 1099-S is issued, the sale still needs to be reported, usually on Schedule D.

- Investment Property: Use Schedule D and Form 8949 to report any gains or losses.

- Rental Property: Use Form 4797 and Schedule D to report the sale, and be sure to account for depreciation recapture.

- Business Property: Similar to rental property, use Form 4797 and Schedule D, including depreciation if applicable.

Real estate professionals should help clients navigate the reporting process to make sure everything’s filed correctly and all exclusions or deductions are claimed.

Beyond the basics, there also a few special situations that require extra attention:

- Multiple Sellers: You’ll need to file a separate 1099-S for each seller. Be sure to allocate the gross proceeds clearly, and make a reasonable effort to contact all parties.

- Foreign Sellers: These sales still need to be reported, and they may be subject to withholding under FIRPTA. (See IRS Publication 515 for details.)

- Contingent Payments: Report the highest amount that can reasonably be determined at the time of sale.

Avoid These Common 1099-S Filing Mistakes

Form 1099-S may seem straightforward, but small missteps can lead to costly consequences. Here are some of the most common errors real estate professionals make and how to avoid them:

- Verify Taxpayer Identification Numbers (TINs): Ensure the seller’s TIN is accurate and complete to avoid backup withholding or automatic penalties.

- Complete All Required Fields: Include the seller’s full name, address, TIN, property address, gross proceeds, and closing date.

- Use the Right Form: Don’t mix up Form 1099-S with other types like 1099-MISC or 1099-NEC.

- Meet IRS Deadlines: Provide the seller’s copy by February 17 and file electronically with the IRS by March 31.

- Keep Records: Hold onto copies of the form and any supporting documents for at least four years.

- Assign Responsibility: Add a clause in the purchase agreement to clearly state who’s filing the form—this helps prevent duplicate submissions.

To stay compliant, real estate professionals should:

- Add a clause to the purchase agreement designating the Form 1099-S filer.

- Use Form W-9 to obtain the seller’s TIN to avoid backup withholding issues.

- Be aware of non-filing penalties, starting at $250 per violation, up to $565,000 annually.

Final Thoughts

If you’re in real estate, chances are you’ve run into Form 1099. It’s not the flashiest part of closing a deal, but it’s important to get it right. Knowing when it’s required, who needs to file it, and how to avoid common mistakes can save you from costly penalties. The right e-file provider can make the process a lot easier and help keep your transactions moving forward.