Selling a mortgage note means transferring the loan to another party, who takes over collecting the payments. Homeowners and investors often choose to sell their notes to get quick cash, usually a lump sum between 65% and 95% of the note’s value, depending on the risk and market conditions.

It’s important to have all the right documents ready and to understand what buyers are looking for, such as the borrower’s credit and the property’s location. You can sell the entire note or just a portion of it. It’s also important to consider whether the sale is recourse or non-recourse, since that affects your future financial obligations. In the end, this is a way to access quick cash while transferring the responsibility of collecting payments.

Understanding Texas Mortgage Notes

A mortgage note in Texas is a legal agreement between the borrower and the noteholder. The borrower agrees to repay the loan based on specific terms, while the noteholder has the right to collect payments and, if needed, start foreclosure proceedings.

Texas uses both deeds of trust and traditional mortgages, so your note could be secured by either one. This mainly affects how foreclosure is handled if it ever becomes necessary, but it doesn’t impact your ability to sell the note. Strong real estate markets in Texas, especially in major cities, often lead to higher note values.

Property values in Dallas suburbs vary by area:

- Established neighborhoods like Richardson, Garland, and Irving tend to show steady appreciation.

- High-growth areas such as Frisco, McKinney, and Allen often attract premium offers from note buyers.

- Emerging markets like Celina and Prosper show strong potential but usually require more specialized evaluation.

Why Sell Your Mortgage Note?

Meeting immediate capital needs is one of the main reasons people choose to sell their mortgage notes, whether it’s to grow a business, pursue new investment opportunities, or cover unexpected expenses. Instead of waiting years to receive the full value of the note, you can get cash up front.

Estate planning is another common reason for selling a mortgage note. Heirs often prefer liquid assets and want to avoid the hassle of managing ongoing payments. For example, a 78-year-old noteholder in Dallas might sell a $200,000 note simply to streamline their finances and spare family members from having to handle payment collections.

Risk mitigation also motivates sales. Economic uncertainty, borrower employment changes, or property market shifts can make guaranteed cash more attractive than future payment streams. When a Texas mortgage note buyer purchases your note, they assume these risks.

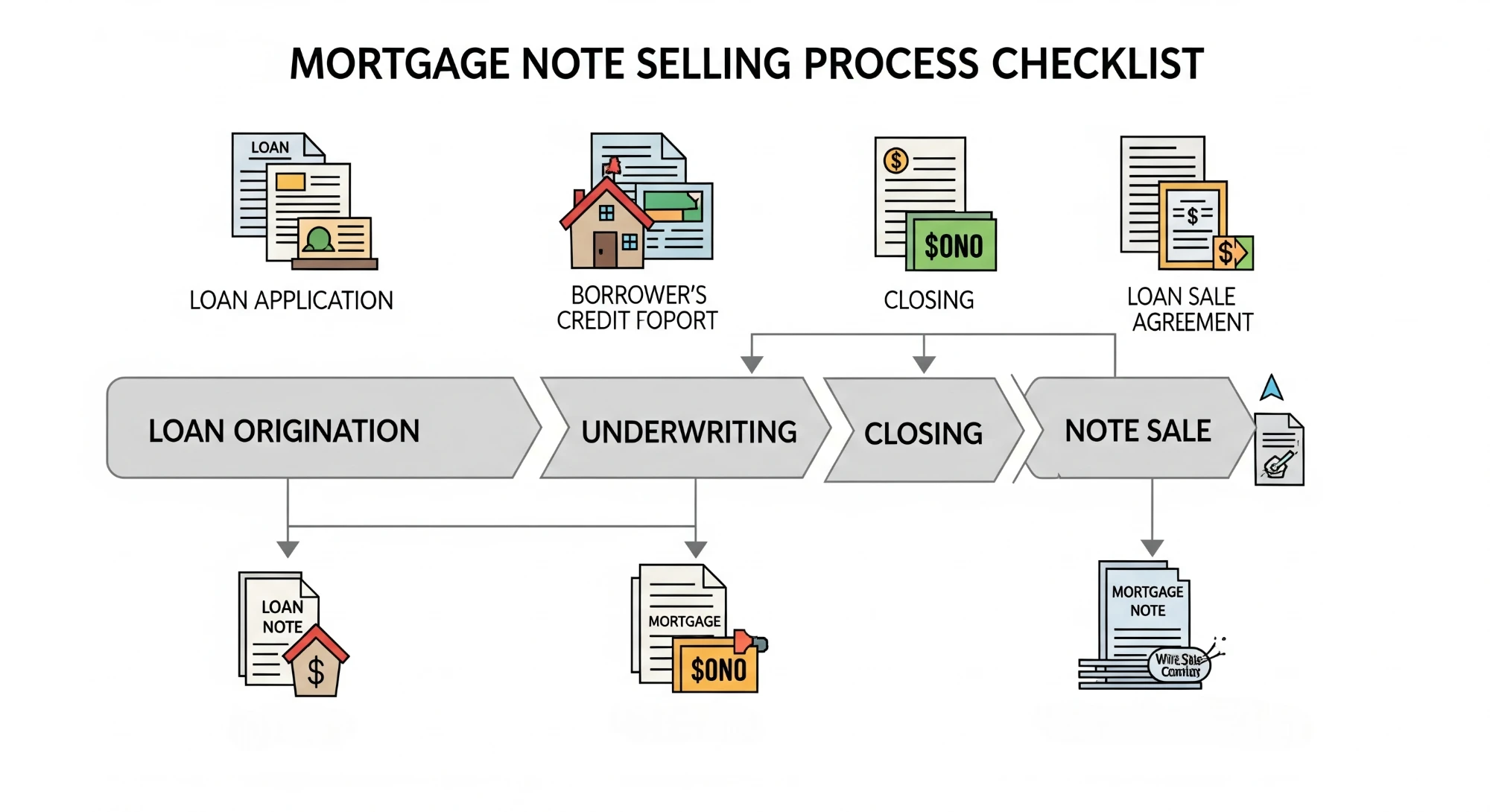

The Texas Note Selling Process

Initial Evaluation

Your note’s value depends on several factors:

Payment history is the most important factor; consistent and on-time payments are a strong indicator of reliable income. Property value also matters significantly, especially in appreciating markets like Dallas-Fort Worth. Furthermore, interest rates directly affect pricing; notes carrying rates above current market levels often sell at a premium.

A note originated three years ago at 8% interest holds more value today than one at 4%, simply because buyers receive higher returns. While borrower creditworthiness is less critical than payment history, it still influences the note’s value. Lastly, documentation quality is also crucial; complete files with recorded mortgages, title insurance, and detailed payment records significantly streamline transactions.

Documentation Requirements

Texas note sales require specific documentation. The original promissory note and the recorded mortgage or deed of trust form the absolute foundation. Additionally, payment records demonstrating a clear collection history are crucial for accurate pricing.

Essential documents include:

- Original promissory note and recorded mortgage/deed of trust

- Complete payment history with dates and amounts

- Property appraisal and title insurance policy

- Borrower credit reports and income verification from origination

- Property insurance policies and current tax records

Additional documents might include any modification agreements or significant correspondence with borrowers. Ultimately, well-organized documentation not only accelerates the evaluation process but also frequently leads to better offers.

Timeline and Closing

Texas note sales typically close within 15 to 35 days. After submitting complete documentation, you can expect initial offers to arrive within 48 to 72 hours.

Following this, due diligence commences, which includes a property appraisal and title examination. Appraisals in a major market like Dallas usually complete within one week. However, unique property characteristics in areas such as Southlake or Highland Park might require additional time. Similarly, rural properties located in counties outside major metropolitan areas may necessitate specialized appraisers, slightly extending these timelines.

Closing for note transfers occurs through experienced title companies or attorneys familiar with these specific transactions. The process closely resembles traditional real estate closings, where all necessary documents are recorded, and funds are disbursed simultaneously.

Understanding Texas Foreclosure Laws

Texas’s foreclosure laws significantly impact note values and buyer confidence. The state permits both judicial and non-judicial foreclosures; however, non-judicial procedures overwhelmingly dominate due to their speed and cost efficiency.

Non-Judicial Foreclosure Process

The foreclosure process in Texas begins with a 20-day notice to the borrower, providing them an opportunity to cure any defaults. This relatively short cure period is highly beneficial to noteholders when compared to states that require longer notification periods.

Following the cure period, lenders are required to post a notice of sale 21 days prior to the auction. These sales consistently occur on the first Tuesday of each month, typically between 10 AM and 4 PM, at the county courthouse.

Key timeline benefits:

- Total process typically concludes within 27 days

- Among the fastest foreclosure procedures in the nation

- Compare to judicial foreclosures in New York or Florida exceeding 18 months

Foreclosure Costs and Recovery

Texas foreclosure costs typically range from $1,200 to $3,500, positioning it as one of the most cost-effective states for enforcement. These relatively low costs translate to a higher net recovery for noteholders and, consequently, better pricing for notes secured by Texas properties.

Furthermore, Texas permits deficiency judgments, which allow for the collection of any remaining balance after foreclosure sales. This right significantly strengthens note security, a particularly crucial aspect for notes with high loan-to-value (LTV) ratios. It’s important to note, however, that Texas provides no redemption rights after foreclosure sales; meaning, once the property is sold at auction, the borrower cannot reclaim it.

Dallas Market Considerations

Dallas represents Texas’s largest note market, characterized by diverse property types and strong economic fundamentals. The metroplex’s robust job growth, particularly within the technology and healthcare sectors, consistently supports property values and enhances borrower stability.

Market characteristics by area:

Different areas within Dallas County exhibit varying characteristics. For instance, notes secured by properties in established neighborhoods like Highland Park or University Park typically command premium pricing due to their stable values and affluent borrower demographics.

Suburban markets, on the other hand, present distinct opportunities. Frisco’s rapid growth, for example, attracts note buyers seeking appreciation potential, while established areas like Richardson offer reliable stability. However, notes secured by properties in emerging areas such as Celina or Prosper might receive slightly lower pricing due to limited comparable sales data.

Commercial notes secured by Dallas properties often outperform those in smaller Texas markets. The city’s diverse economy robustly supports various business types, ranging from small retail establishments in Deep Ellum to major corporate facilities in Las Colinas.

Regional Comparisons

While Dallas certainly dominates Texas note trading, other markets definitely offer unique opportunities.

Houston’s energy-driven economy, for instance, creates distinct note characteristics, especially for commercial properties. Austin’s booming technology sector strongly supports residential note values, though it can also lead to more volatile pricing. San Antonio’s consistent growth provides steady note performance, while smaller markets such as Amarillo or Beaumont might require specialized buyers who are particularly familiar with local conditions.

Dallas also benefits from having multiple note buyers operating locally, which fosters competitive pricing.

Maximizing Your Note’s Value

Several strategies can significantly improve your note’s sale price. First and foremost, maintaining detailed payment records unequivocally demonstrates reliability. Digital records showcasing consistent, on-time payments, especially during periods of economic stress (such as 2020-2021), will substantially boost buyer confidence.

Property maintenance directly impacts the underlying collateral’s value. While you might not directly control a property’s upkeep, staying well-informed about neighborhood developments can certainly aid your timing decisions.

Market timing considerations:

- Rising rates can improve pricing for existing notes carrying higher interest rates

- Falling rates might compress premiums

- Consider partial sales for large notes exceeding $500,000

- Selling a portion while retaining some payments provides immediate cash while maintaining income stream

Choosing the Right Buyer

Note buyers vary significantly in terms of their pricing, service, and overall reliability.

Direct buyers, such as institutional funds, typically offer highly competitive pricing but may require more extensive documentation. Local buyers, conversely, might provide faster service, though potentially at the cost of lower offers. Experience with Texas properties is paramount; buyers familiar with local foreclosure laws, market conditions, and documentation requirements often facilitate smoother transactions and provide more competitive pricing.

Closing ratios are a strong indicator of buyer reliability. Established buyers commonly close 90-95% of accepted offers, whereas newer entrants might exhibit lower success rates. Failed closings not only waste valuable time but also have the potential to cost money, especially if market conditions shift.

Key Takeaways

Selling mortgage notes in Texas offers noteholders efficient access to capital. The state’s favorable foreclosure laws, diverse economy, and robust real estate markets consistently support competitive note pricing.

Achieving a successful sale, however, hinges on proper documentation, setting realistic expectations, and carefully selecting qualified buyers. Ultimately, Texas’s streamlined legal environment and well-established real estate infrastructure make note sales a relatively straightforward process when compared to many other states.

For noteholders within the Dallas metroplex, abundant buyer options and strong property fundamentals create truly optimal selling conditions. Whether your note is secured by a suburban home in Plano or a commercial property in downtown Dallas, Texas undeniably offers one of the nation’s most efficient note markets.

Ultimately, the decision to sell always depends on your individual circumstances. However, Texas noteholders significantly benefit from operating in a mature, highly competitive market that appropriately values their assets.