Tariffs and evolving trade policies play a huge part in shaping real estate trends across the United States. While housing markets are usually discussed in terms of interest rates, population growth, or lending standards, global trade dynamics quietly influence the underlying costs of building, renovating, and ultimately purchasing or selling a home.

Understanding these forces helps explain why some regions experience sharper price shifts, construction slowdowns, or inventory constraints following changes in tariffs and trade.

In the current market, buyers and sellers increasingly rely on local expertise to interpret these signals. Working with the best real estate agent can help you translate national and international economic changes into practical insights about pricing, timing, and negotiation within a specific US local market.

This article examines how tariffs and trade policy shifts affect construction costs, housing supply, consumer confidence, and broader economic conditions, and how these factors interact to influence real estate trends nationwide.

Tariffs, Trade Policy, and Construction Costs

Changes in tariffs and trade policy influence residential construction costs by affecting material pricing, project feasibility, and development timelines which ultimately shapes broader real estate trends.

Materials Most Affected by Tariffs

Tariffs and trade policies directly affect the cost of key construction materials used in residential and commercial development. When tariffs are applied to imported goods, domestic prices often rise due to reduced competition or higher input costs.

Here are the common materials influenced by tariffs and trade:

- Lumber and wood products used for framing and finishes

- Steel which is used in structural components and reinforcements

- Aluminium used in windows, siding, and roofing

- Manufactured components such as fixtures, appliances, and HVAC systems

Even when materials are sourced domestically, tariffs can still affect pricing by altering supply chains or increasing demand for local substitutes. These higher material costs may be passed through to builders and contractors and, eventually, to consumers.

Effects on New Construction Pricing

Rising material costs directly affect the pricing of new homes. Builders must account for higher expenses when estimating project budgets, which often leads to specific outcomes like:

- Increased list prices for newly built homes

- Reduced profit margins for developers in competitive markets

- Delays in project starts while costs stabilize

- Greater emphasis on value engineering or design changes

In some US local market areas, especially those experiencing rapid population growth, these price pressures can be absorbed more easily. In gradual-growth regions, higher construction costs may discourage new development altogether, affecting local real estate trends.

Renovation Costs and Timelines

Tariffs and trade policies also influence renovation and remodeling activity. Homeowners facing higher prices for imported materials may postpone upgrades or scale back project scope. Contractors may experience longer lead times if supply chains are disrupted.

Renovation impacts typically include:

- Higher bids for kitchen and bathroom remodels

- Extended project timelines due to material availability

- Increased demand for alternative materials

- Greater cost uncertainty for fixed price contracts

These dynamics affect resale values and inventory quality, particularly in markets where older housing stock relies heavily on renovations to remain competitive.

Housing Supply, Builder Activity, and Affordability

As construction costs fluctuate, builder decisions and regional constraints directly shape housing supply and affordability across the local market.

Impact on Housing Supply Levels

When construction costs rise, housing supply growth slows. Developers may delay or cancel projects if projected returns no longer meet financial thresholds. Over time, reduced new construction can tighten inventory, especially in high-demand areas.

Limited supply can contribute to:

- Upward pressure on home prices

- Fewer entry-level housing options

- Increased competition among buyers

- Greater regional divergence in real estate trends

These effects are rarely uniform. Some cities with strong employment growth may continue building despite higher costs, while others see noticeable slowdowns.

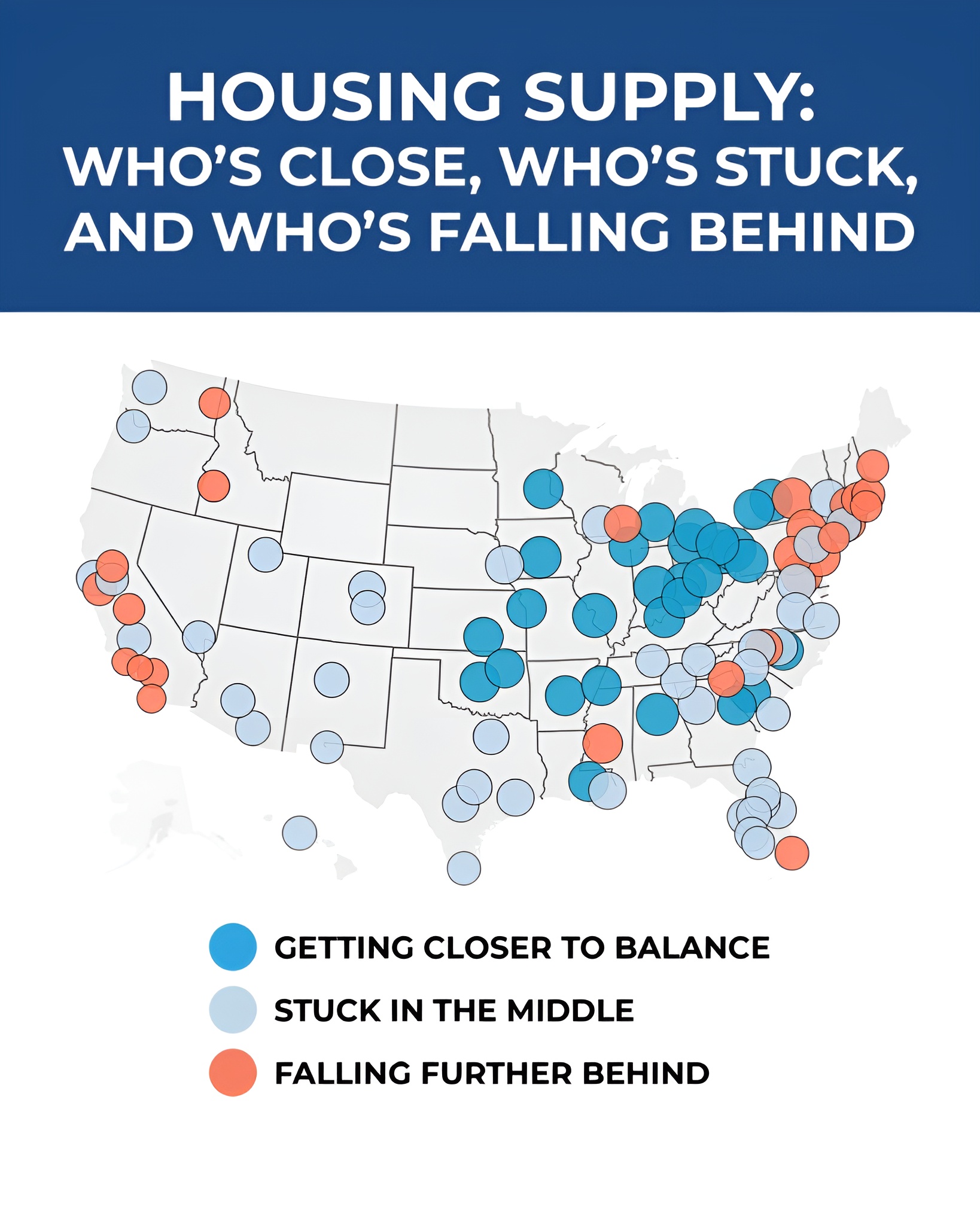

Regional Differences Across the US Local Market

The influence of tariffs and trade varies by geography. Coastal markets, manufacturing hubs, and areas dependent on imported materials may feel stronger effects than regions with more localized supply chains.

Regional variations depend on:

- Proximity to ports and trade infrastructure

- Local labor availability and costs

- Zoning and regulatory environments

- Existing housing stock age and type

Understanding these differences is essential when evaluating real estate trends at the city or state level.

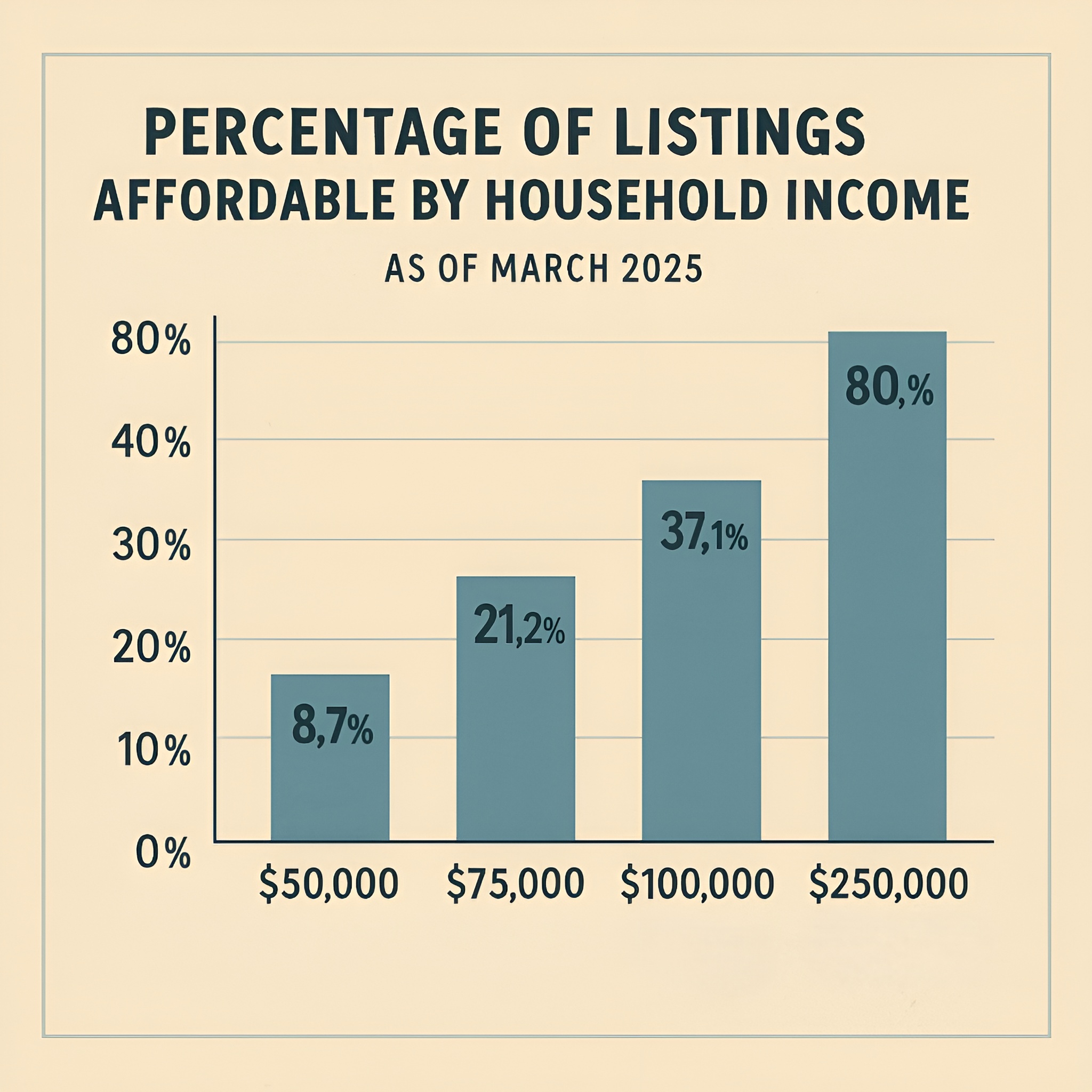

Affordability and Buyer Constraints

Higher construction and renovation costs can reduce affordability, particularly for first-time buyers. As prices rise faster than incomes, some households delay homeownership or shift preferences toward smaller homes or different locations.

Affordability pressures may lead to outcomes like:

- Increased demand for townhomes and condos

- Migration toward lower-cost metro areas

- Longer search times for buyers

- Greater sensitivity to interest rate changes

Economic Conditions, Confidence, and Housing Demand

Housing demand does not operate apart from the broader economy. Employment stability, inflation, and borrowing conditions interact with tariffs and trade to influence buyer behavior and market momentum.

Interaction With Interest Rates and Inflation

Tariffs and trade policies can contribute to broader inflationary pressures by increasing the cost of goods. In response, monetary policy adjustments may affect mortgage rates, which directly influence housing demand.

Higher rates result in consequences such as:

- Reduced purchasing power for buyers

- Slower price appreciation

- Increased importance of negotiation

- Shifts toward renting in some markets

This interaction among tariffs, trade, inflation, and interest rates highlights how global policy decisions filter into everyday housing decisions.

Employment Trends and Consumer Confidence

Trade policy changes can affect employment levels in sectors such as manufacturing, logistics, and construction. Job stability and wage growth play a significant role in consumer confidence, which in turn shapes housing demand.

When confidence is strong you typically see that:

- Buyers are more willing to commit to long-term purchases

- Sellers may list homes at higher price points

- Transaction volumes tend to increase

When confidence weakens, markets may experience longer listing times and greater price sensitivity.

Market Volatility and Short-Term Uncertainty

Periods of trade uncertainty can introduce volatility into housing markets. Buyers and sellers may adopt a wait and see approach, leading to temporary slowdowns.

Short-term effects are:

- Fluctuating inventory levels

- Wider pricing ranges between similar properties

- Increased importance of local data

- Greater reliance on professional guidance

Navigating these conditions requires careful analysis of both national indicators and local market behavior.

What Buyers and Sellers Should Watch For

Both buyers and sellers benefit from tracking indicators that reflect shifting economic and construction dynamics.

Inventory Shifts and Price Stability

Changes in construction activity and demand can alter inventory levels.

Buyers and sellers should monitor indicators such as:

- New listings versus completed sales

- Price adjustments on comparable homes

- Time on market trends

These indicators provide early signals of changing real estate trends within a specific local market.

Negotiation Dynamics in Changing Markets

As cost pressures and economic uncertainty evolve, negotiation strategies may shift. In some markets, buyers gain leverage through increased inventory, while in others, limited supply sustains seller advantages.

The following are key negotiation considerations:

- Seller concessions or credits

- Flexibility on closing timelines

- Inspection and appraisal contingencies

Housing Type and Location Sensitivity

Different housing types and locations are shaped by cost pressures not just from tariffs but from broader construction cost increases, with construction expenses representing a record 64.4 percent of the average new home price in 2024 which is up from 60.8 percent in 2022.

This directly influences how single-family, condo, and multifamily markets respond to pricing and demand pressures.

Interpreting Real Estate Trends in a Complex Environment

Tariffs and trade policy shifts influence US housing markets through construction costs, supply constraints, affordability pressures, and broader economic conditions. While these forces operate at the national and global levels, their effects are ultimately felt locally, shaping neighborhood outcomes and long-term real estate trends.

Buyers and sellers benefit from understanding how tariffs and trade interact with interest rates, employment, and consumer confidence. Inventory changes, pricing behavior, and negotiation dynamics reflect these underlying factors before they become widely visible in headline data. Because impacts vary by region, housing type, and timing, broad generalizations can be misleading.

In periods of economic uncertainty, informed decision-making becomes more important than prediction. Interpreting market signals accurately requires local context, historical perspective, and ongoing analysis.

For many, partnering with the best real estate agent provides a structured way to assess shifting conditions, understand the nuances of a specific local market, and respond thoughtfully to evolving real estate trends.