If you own a home in the Dallas-Fort Worth area, severe weather isn’t a question of if, but when. Hail storms pound North Texas every spring. Tornadoes cut through the suburbs. The February 2021 Texas winter freeze left behind thousands of burst pipes and ruined ceilings. And when property damage happens, most homeowners do the same thing: they call their insurance company and assume the process will go smoothly.

Unfortunately, that is rarely how it goes. Texas has one of the highest claim denial rates in the country, and the gap between what insurers offer and what repairs actually cost can be substantial. The good news is that homeowners who understand the process before disaster strikes are usually in a much stronger position than those who don’t.

This guide walks through what to do right after damage occurs, what your insurer is legally required to do, and when it makes sense to bring in outside help.

The Reality of Texas Insurance Claims

Here’s a number worth knowing before you ever file a claim. According to a Weiss Ratings study cited by the Houston Chronicle, approximately 47% of homeowners insurance claims filed in Texas in 2024 were closed without payment. That means nearly half of all claims got zero payout. At the same time, Texas homeowners are paying more than ever. Average premiums jumped over 55% between 2019 and 2024, marking the fastest increase in the country. This puts the average annual cost somewhere between $3,291 and over $4,000 depending on your location, according to data from Texas 2036 and the Texas Department of Insurance.

Those two facts are frustrating side by side because the adjuster who shows up after your claim is filed works for the insurance company. Their job is to evaluate the damage, but they are also representing the company paying the claim. That is not being cynical. That is simply how insurance claims are set up.

That’s where a quick search for a public insurance adjuster near me can help level the playing field. These are licensed professionals who work for you instead of the insurer. They read your policy, document the damage, and negotiate the settlement on your behalf. Consider the numbers. There are over 117,000 insurance company adjusters operating in Texas, compared to only 944 licensed public adjusters in the state, according to data cited by Insurance Claim Recovery Support, a Texas public adjusting firm. The insurer side has numbers and experience, so hiring a public adjuster can help balance the process.

Before you ever need that kind of help, though, there’s a lot you can do on your own.

Step-by-Step: How to Handle a Damage Claim the Right Way

If you’re dealing with storm, hail, or water damage in Dallas, the way you handle the first few days after the incident can affect how your claim turns out. Taking the right steps early helps protect your property, strengthens your documentation, and reduces the chances of disputes with your insurer later on.

Document Everything Before You Touch Anything

The single biggest mistake Dallas homeowners make after a storm is cleaning up before they’ve documented the damage. Leave everything exactly as it is. Walk through every affected area with your phone and record a narrated video. Open cabinets, show the ceiling, and get close-ups of cracked walls or soaked floors. Photos are good, but a video with narration is better because it captures context that a single frame can miss.

Keep every damaged item you can. Adjusters and insurers sometimes dispute whether damage was caused by that storm, leak, or freeze, or whether it was pre-existing. Physical evidence is harder to argue with than photos alone. If you’re unsure what to look for, reviewing signs of water damage in your home can help you catch issues you might overlook on a first walkthrough. Preparing your home for severe weather beforehand can also reduce the risk of more serious and expensive damage later on.

Make Temporary Repairs Only

You’re allowed and expected to make temporary repairs to prevent further damage. This includes covering broken windows, patching holes in the roof with a tarp, and keeping every receipt. What you shouldn’t do is replace windows, tear out water-damaged drywall, or re-roof before the adjuster has seen the original damage. Insurers can and do argue that they can’t verify the scope or cause of the original damage when permanent repairs are made first.

File Promptly and Build a Paper Trail

File your claim as soon as you have documentation ready. Texas law requires insurers to acknowledge a claim within 15 days of receiving it, then accept or deny it within 15 business days of receiving all requested information, and pay within 5 business days of agreeing to pay, according to the Texas Department of Insurance. The clock on those deadlines starts the moment you file.

After every phone call with your insurer, send a follow-up email summarizing what was discussed and what was agreed to. Keep a running log with dates, names, and what was said. If a dispute ever comes up, that paper trail is what you’ll rely on.

Know What Your Policy Actually Says

Wind and hail deductibles in Texas are often calculated as a percentage of your home’s insured value instead of a flat dollar amount. On a $400,000 home with a 2% deductible, you’re responsible for the first $8,000 before coverage kicks in. That’s not unusual here, and a lot of homeowners don’t find out until after they’ve filed.

Also pay attention to whether your policy pays Actual Cash Value or Replacement Cost Value. Actual Cash Value factors in depreciation, which means a 10-year-old roof gets paid out at a fraction of what replacement actually costs. Replacement Cost Value pays what it costs to replace at current prices, though often in two installments. The difference can run into tens of thousands of dollars on a large claim. If you are new to homeownership in the DFW area, reading up on what a home inspection report covers can help you understand what your policy likely will and won’t cover.

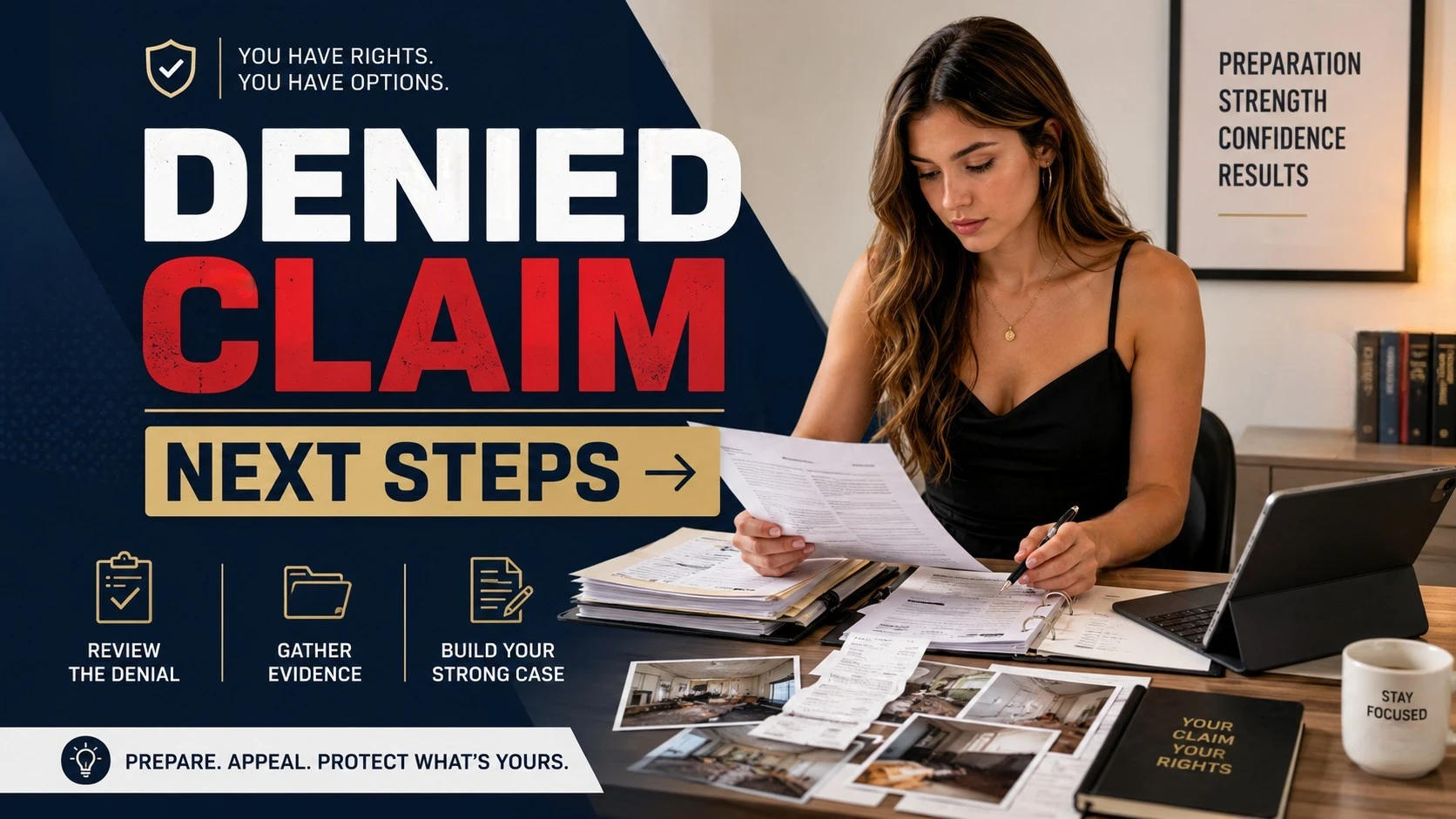

What to Do If the Insurance Offer Seems Low

Lowball offers are common in Texas. Insurance company adjusters often rely on Xactimate or similar pricing software, which can underestimate actual repair costs in markets where labor and materials are running higher than the software’s database reflects. The gap between what the software says a repair should cost and what a local contractor quotes you can be significant.

If the insurer’s offer feels low, get two or three independent contractor estimates before you accept anything and provide them to your adjuster in writing. If the insurer still won’t budge, most Texas homeowners policies include an appraisal clause. This is a formal process where both sides hire independent appraisers, and a third-party umpire resolves the disagreement. Invoking appraisal is not the same as filing a lawsuit. It is a contractual dispute process that often produces better outcomes without going to court.

If your claim was denied entirely, the nonprofit United Policyholders maintains a Texas homeowners insurance FAQ that walks through the denial appeal process in plain language. It’s one of the better free resources for homeowners who don’t know where to start.

Understanding Your Rights Under Texas Law

Texas has some of the clearest consumer protections in the country when it comes to homeowners insurance claims, but many homeowners never realize they have them.

Insurers face strict deadlines. They must acknowledge a claim within 15 days, make a decision within 15 business days of receiving your documents, and issue payment within 5 business days of approval. If they miss the payment deadline without a valid reason, they owe you 18% annual interest on the unpaid amount plus attorney fees if you have to sue to collect. That’s not a small penalty, and it applies when your claim is sitting idle without explanation.

It’s also illegal under Texas law for insurers to misrepresent your policy terms, make unreasonably low settlement offers, or use other unfair claims handling tactics. You can file a complaint with the Texas Department of Insurance. Taking this step can sometimes get a stalled or denied claim looked at again, even without going to court. The TDI’s disaster claims FAQ walks through your rights in plain terms.

One timing detail matters: you generally have two years from the date of loss to take legal action on a Texas homeowners claim. That deadline can come faster than you’d expect when you’re tied up with repairs, adjusters, and back-and-forth correspondence.

How a Licensed Public Adjuster Can Help

The difference between an insurance company adjuster and a public adjuster comes down to who they work for. The insurer’s adjuster is employed by or contracted to the insurance company. A public adjuster is hired by you, paid by you as a percentage of your final settlement, and answers to you alone.

As noted earlier, the numbers are heavily tilted toward insurers. Trained advocates who work with policy language and damage valuation every day can help homeowners pursue stronger settlement outcomes than they may be able to achieve alone on complex claims.

Under Texas law, public adjusters can charge up to 10% of the final settlement amount. They can’t collect anything upfront in most cases, and you have a 72-hour cancellation window after signing a contract. Before hiring anyone, verify their license through the Texas Department of Insurance’s lookup tool, which is explained in the TDI public adjusters guide. Unverified storm chasers who show up after major weather events and promise to handle your claim are a separate problem entirely.

Public adjusters make the most sense on larger or more complex claims, especially those involving multiple damage types, significant structural damage, or a claim that has already been denied or significantly underpaid. For a minor wind claim with a clear cause and an offer that matches contractor estimates, you may not need one. But if something feels wrong about how your claim is being handled, that feeling is usually worth acting on.

On the financial side, how storm damage affects your home’s resale value often depends as much on whether repairs were fully funded as on the damage itself. An underpaid claim that leads to incomplete repairs can show up years later when you go to sell.

Do Not Let a Denied Claim Be the End of the Story

Dallas homeowners aren’t powerless against their insurers, but you do have to know the rules. Document before you clean up, file fast and in writing, and read your deductible and coverage type before you assume you know what you’re owed. Challenge low offers with contractor estimates, and invoke the appraisal clause if you need to.

Texas law gives you real protections, including strict timelines, interest penalties for delays, and the right to file complaints with the TDI. Those tools work, but only if you use them.

The Texas property insurance market is genuinely tough right now: premiums keep rising, and close to half of claims are reportedly closed without payment. That’s not a reason to walk away from a legitimate claim. It’s a reason to go in prepared, keep records of everything, and recognize when the process has gotten complicated enough that you need someone in your corner.