Picture this: your family is ready to cash in on a booming Kaufman County land subdivision, and then the title company flags the property. The deed is clouded by a missing or outdated will. You’re not alone in that frustrating scenario, either; 35% of U.S. adults report family conflict tied directly to a lack of estate planning.

A smooth real estate closing depends on a clean title from day one. A clean title means there are no disputes or unclear claims about who legally owns the property. A missing estate document, an unresolved probate issue, or a dispute among heirs can stop a sale before it gets to closing.

So before you ever stick a “For Sale” sign in the yard, you need to be sure you have documented, undisputed legal ownership.

Why a Missing Will Clouds Your Property Title

A clouded title is a defective title or a title with an outstanding claim against it which prevents transfer of the property. If the original owner dies without a clear, up-to-date will, ownership may be split among heirs, causing major problems at closing.

And you may be surprised at the number of unprepared property owners. In 2024, only 32 percent of Americans had a will or estate planning documents. When clear legal authority is missing, disputes pop up fast. In one recent Texas case, someone with no legal relationship to the deceased attempted to control the deceased’s estate property and evict tenants.

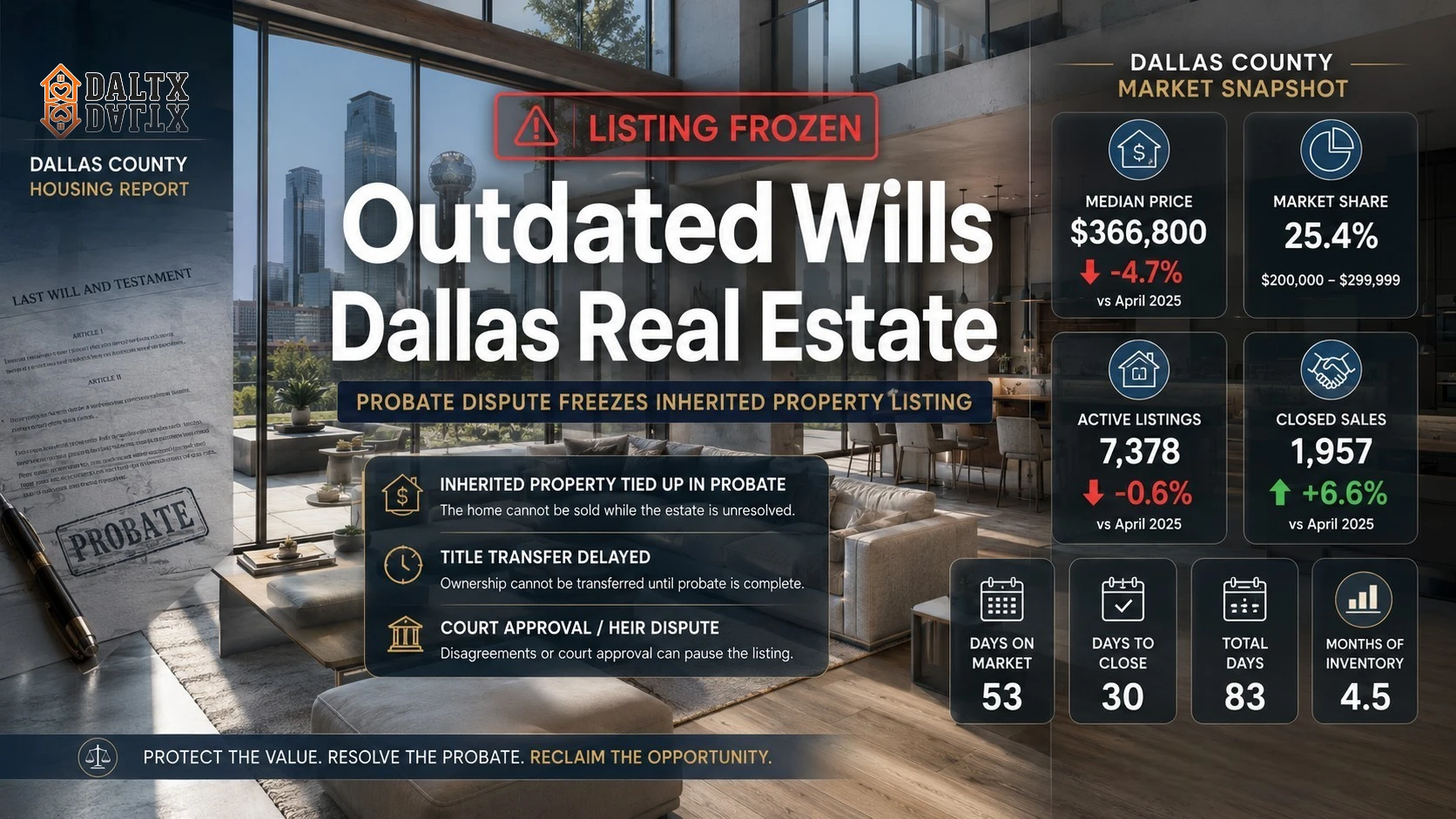

The Kaufman and Dallas County Impact

Rapid DFW growth has made inherited land valuable, but buyers avoid subdivisions or homes with title disputes. Title companies require certainty, and unclear ownership stalls the underwriting process.

How Divorce Can Wreck Your Estate Plan

One of the biggest reasons real estate deals fall apart? An outdated will sitting in a drawer after a divorce. Life moves on, but the paperwork often doesn’t. Only 10% of people update their estate plan after a major life change, such as marriage or divorce. That kind of negligence turns a straightforward home sale into a months-long legal headache.

When an outdated will still names an ex-spouse, it can halt a home sale entirely while the title company tries to untangle the mess. If you’ve recently gone through a divorce and need to know how to protect your estate in your will, updating it should be the first thing on your list.

Getting ahead of this paperwork is the single best defense against a delayed closing.

Here’s a quick breakdown of how different situations can affect a property sale:

| Scenario | Will Status | Impact on Property Sale | Real Estate Outcome |

|---|---|---|---|

| Post-divorce (updated will) | Current | Clear chain of title established | Smooth closing |

| Post-divorce (outdated will) | Ex-spouse still listed | Extensive legal documentation or court orders needed | Delayed by months; possible deal cancellation |

| Intestate (no will) | Non-existent | Requires Affidavit of Heirship; all relatives must be located | High risk of disputes; buyers likely walk away |

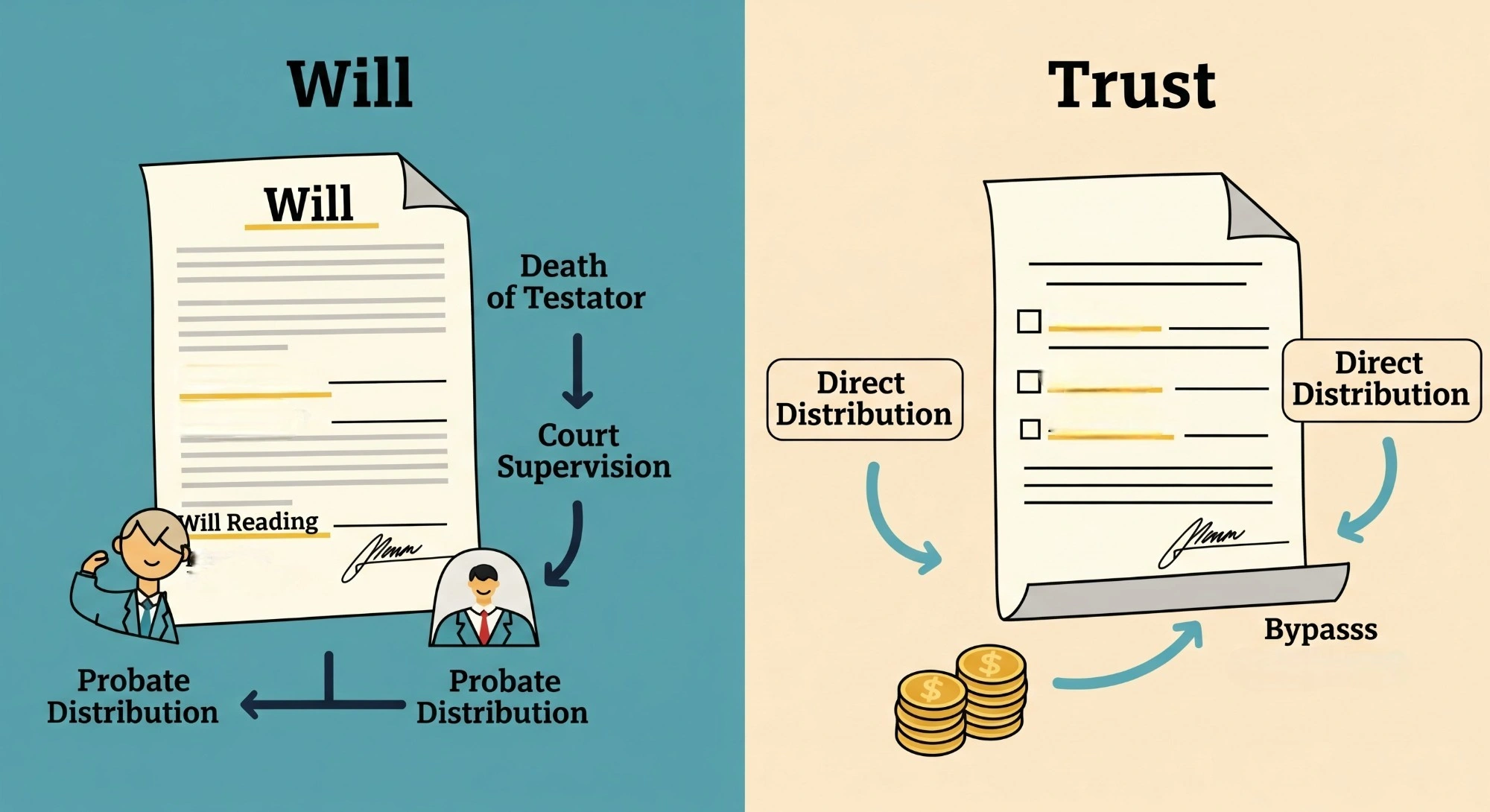

How Contentious Probate Freezes Property Listings

Probate is the court-supervised process that determines whether a will is valid and directs how assets should be distributed after death. You cannot legally transfer ownership of a deceased parent’s house without this legal process, especially when there are unknown liens, unreleased mortgages, or other legal claims against the property. Try to skip probate, and your title company will immediately reject the sale.

The landscape is getting harder to navigate, too. In 2025, 11,328 will challenges were filed, many involving blended families, second marriages, estranged relatives, or disputes over an aging parent’s estate. These disputes instantly freeze property listings, barring families from their inherited equity.

The financial hit can be brutal, and the process can drag on for months or even years. During that time, the property sits exposed to outside financial claims. To understand one of the biggest risks, check out this guide on MERP claims, which explains how the state might place a Medicaid lien on your home.

Clearing an Inherited Property Title

Selling an inherited house in North Texas? Take proactive steps to avoid legal issues.

Use this step-by-step blueprint to help ensure your title is marketable and the closing goes smoothly:

- Locate the original will. Before doing anything else, find the legally binding document. A photocopy often won’t cut it with a Texas title company underwriter.

- Verify your legal authority. Make sure you’re the legally appointed executor. As highlighted in recent Texas court rulings, establishing the proper court to validate your authority is the critical first step.

- Address outstanding liens. Work closely with a trusted title agent to uncover unknown judgments, unpaid Dallas County property taxes, or unreleased mortgages that could blow up the sale.

- Secure an Affidavit of Heirship (if needed). If there’s no will, have an attorney draft one. This requires signatures from disinterested witnesses who know the family history well.

- Review promissory notes. If the estate involves seller-financed mortgages, you’ll want to understand your options. This guide on selling your mortgage note in Texas can help.

Securing Your Property’s Future

A clean, legally vetted title isn’t optional; it’s required before listing any property in the Dallas market. Ignoring estate planning doesn’t just cause emotional strain for families; it also harms their finances. It can practically and legally block the transfer of wealth. Sounds dramatic? It’s not.

Take control of your real estate assets through proactive planning today. Update your will and learn the local probate process and you will protect the value of your property and ensure a smooth transition for your heirs.