Dubai’s property market has made money for plenty of investors, but it has also cost others a lot when they picked the wrong project. In many bad purchases, the issue starts with one thing buyers do not look at closely enough: the developer. Choosing the right developer is one of the most important decisions you’ll make before buying. The warning signs need to be checked before you sign, not after.

Dubai has real buyer protections, especially for pre-construction purchases, but regulations do not remove the need for your own due diligence.

Here are the red flags worth checking before you move forward.

No Proven Track Record of Completed Projects

A credible developer in Dubai should have a track record you can verify. Completed projects, handover dates, and feedback from buyers who have already moved in can often be checked through official tools, site visits, and direct conversations with existing residents.

A developer that cannot point to completed, on-time deliveries deserves caution. Reputable real estate developers in Dubai are transparent about their past projects. They usually make project tours, construction updates, and owner feedback easier to access. If getting basic proof of delivery feels difficult, treat that as a problem.

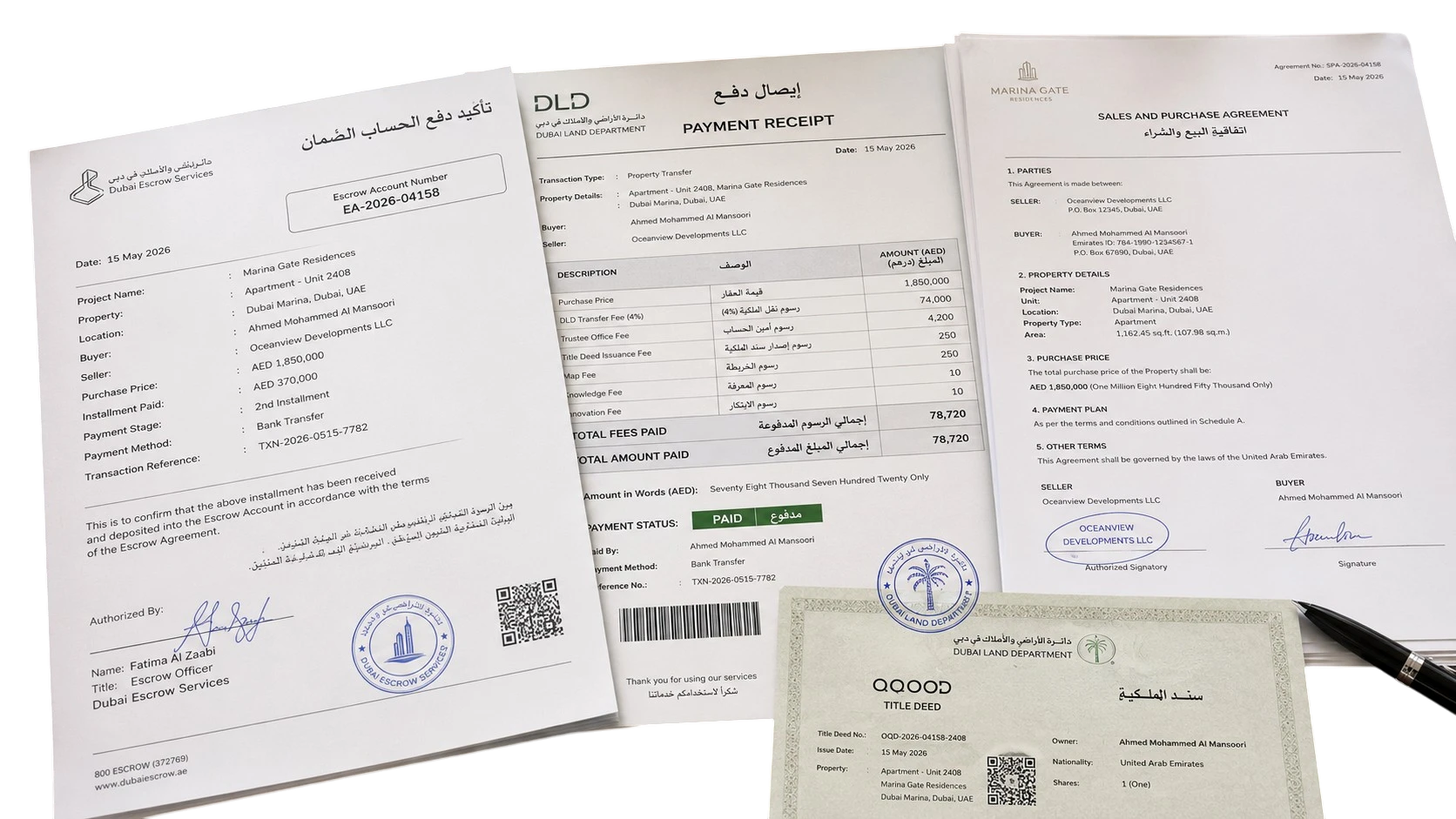

Dodging Escrow Rules

For pre-construction projects in Dubai, buyer payments should go into the project escrow account under the DLD/RERA framework. Those funds are meant for the project, and releases from the account are tied to verified construction progress.

Any developer that cannot provide clear escrow account details, or tries to route payments outside the required structure, is not worth the risk. This is not a small paperwork issue. It is one of the main legal protections that you have. If a developer tries to work around it, walk away.

Payment Plans That Don’t Match Construction Progress

Payment plans are common in Dubai’s off-plan market. A phased payment structure is not a problem on its own. The concern is when large installments are due upfront without enough construction progress to justify them.

The schedule should make sense when compared with documented, inspectable progress on site. Each construction-linked installment should be tied to a stage you can verify. If the payment plan seems built around the developer’s cash needs instead of actual progress, you may be financing the build before the work is there to support it.

Vague or Changing Property Details

Sales agreements for pre-construction properties should include clear, binding specifications for finish materials, appliance brands, flooring, bathroom fittings, and smart home systems. Broad phrases like “premium finishes” or “luxury appliances” without brand names, grades, or clear equivalent standards leave too much room for changes at handover.

Developers that are confident in their product will put the details in writing. Publicly naming the architect, interior designer, or fit-out partner can be useful, but it does not replace written specifications in the contract. Ask for the details and be cautious if the developer pushes back.

Unverified Design and Construction Partners

In a market known for ambitious buildings, a developer’s design and construction partners are worth checking. If a luxury project depends on unnamed in-house teams or little-known firms without a clear record, ask more questions.

Well-known architecture, design, and construction firms add another layer of accountability. Their work can be reviewed, and their reputations are also attached to the project. That does not guarantee a perfect result, but it is still a detail worth weighing.

Poor Communication During the Sales Process

How a developer communicates before you buy is a good preview of what you may deal with during construction and handover. Sales teams that avoid timeline questions, hold back documents, or brush off technical concerns are showing you how the company operates.

Pay close attention to how they answer direct questions. A serious developer should be able to explain delivery dates, project partners, materials, escrow details, and expected service charges without making you chase every answer. Evasive answers during the sales process are not a small mistake. They are part of the pattern.

High-Pressure Sales Tactics and Artificial Urgency

Scarcity can be real in popular Dubai projects, but it is also used to rush buyers. Claims like “only two units left” or “prices go up next week” are often meant to get you to move before you finish your due diligence.

A serious developer does not need to make careful questions feel like a problem. If the sales process pushes you to act quickly and discourages review, slow down. No property is attractive enough to justify skipping basic checks.

The Real Cost of a Bad Decision

Dubai’s regulations can offer real protection, but they are not a substitute for due diligence. These red flags are not abstract concerns. They are the kinds of issues that often show up after buyers realize they made the wrong call.

Take the time to verify the developer, review the contract, check the escrow details, and compare the payment schedule against actual construction progress. Trust documents, site evidence, and direct answers more than polished marketing. The right developer will answer your questions without making the process harder.