The Dallas housing market, which appreciated rapidly over the past few years, is finally showing some early signs of cooling. While the fundamentals that fueled that growth remain strong (rising population, job creation, and business expansion), the market appears to be moving toward a more balanced state. This could be good news for prospective buyers, who may see more opportunities in 2026.

Why Dallas Prices Rose So Fast

So how did we get here? Why did housing prices in Dallas shoot up so quickly?

Over the last decade, Dallas-Fort Worth (DFW) has been one of the fastest-growing markets in the country. Reports show that home values soared 19.6% in 2021 and 22.4% in 2022.

A combination of factors drove this increase. For one, rapid population growth, as both companies and individuals relocated to the region, boosted demand. More companies mean more job opportunities, particularly in the fields of tech, logistics, finance, and healthcare, which have been growing rapidly in DFW for years. There’s also the issue of tight supply and construction delays, which often mean bidding wars and price hikes well above historical norms.

In short, the conditions in DFW created a highly competitive environment that made buying particularly challenging for first-time buyers, even for those with strong finances. But that explosive growth started to wane in 2023 through 2025, and it looks like that trend will continue into 2026.

Current Indicators Pointing to Market Moderation

If we take a look at Dallas housing market trends, all indicators point to the market entering a cooler, more stable phase.

Here are a few:

Slower price growth. Data from Movoto shows that the median sale price in DFW has stabilized in recent months at around $425,000. Compared with the massive increases in the early 2020s, this is a much more reasonable rate of growth.

Homes are also sitting longer on the market, 65 days on average, compared with 54 days at the same time last year. Longer listing times indicate that buyers are no longer rushing to beat rising prices, which means sellers will have to set more realistic expectations when it comes to home prices in Dallas.

More inventory is coming to market, with additional active listings and new construction. An increase in supply gives buyers more choices, which tips negotiations in their favor.

It’s important to note that “cooler” Dallas home prices don’t mean a downturn or a crash, they simply indicate the market is shifting from an overheated seller’s market toward a more balanced market.

What’s Influencing Dallas Home Prices in 2026?

With that in mind, what are the key factors that will influence the housing market heading into 2026?

First, mortgage rates: as of this writing they are still high but easing. Higher interest rates from 2023 to 2025 reduced the affordability of Dallas housing, and thus buyer demand. But many analysts expect rate cuts in 2026, which will improve borrowing power, bring more buyers back into the market, while still supporting moderate price growth. Until then, however, affordability is likely to remain a problem for first-time buyers.

There’s also the reality of more homes and new construction coming onto the DFW housing market. After years of underbuilding, the construction industry in DFW is finally catching up, with many new developments and active listings coming online. More supply means fewer bidding wars, more realistic pricing, and more negotiation room for buyers.

Dallas remains one of the country’s most economically prosperous metropolitan areas, with the tech and engineering sectors, financial services, healthcare, biotech, and logistics. It’s likely that job growth and in-migration will remain strong, which means demand for housing will stay elevated.

What to Expect in the Dallas Market in 2026

With all that in mind, based on current trends, what can we expect for 2026?

The most likely outcome is moderate, rather than explosive, growth. Prices will likely continue to rise, but slowly, perhaps low to mid-single-digit appreciation. It’s also possible that newly developed suburbs may see small price declines or softer negotiation terms, especially if inventory climbs faster than projected buyer demand.

This all adds up to better conditions for buyers, while sellers will need to temper expectations. These conditions will give buyers more negotiating power, more listings to choose from, and more room to breathe when it comes to decision-making. Meanwhile, sellers will need to price their homes competitively, invest time in staging and repairs, focus on good presentation when showing homes, and avoid assuming their listings will go under contract instantly.

It’s unlikely that Dallas will see a crash in 2026, but signs point toward a cooler, more predictable housing market. The future of Dallas housing is stable, even if it’s no longer red‑hot.

Buying a home in the DFW area is exciting, and it’s smartest when you look past today’s needs and plan for tomorrow. DFW has lots of neighborhoods, strong job centers, and good schools, but the best pick for your family is the one that stays comfortable, safe, and functional as life changes.

That means thinking about size and layout, daily routines, and how close you’ll be to services your family may need now and later. One piece many buyers skip is access to dependable healthcare and supportive services for aging family members or those with serious health needs.

Choosing a home near clinics, hospitals, and Medicare‑certified hospice providers can lower stress and help you manage tough moments with a plan. If you want local options for end‑of‑life support, families in DFW often look into trusted Hospice care in Texas so care is close when it counts. Put healthcare access on the same checklist as schools, commute, and parks, because it can matter just as much over the long haul.

Understanding Your Family’s Long-Term Needs in DFW

Image Source: pexels.com

Picking a house is really about making sure it fits your family now and still works five or ten years from today. Across DFW, buyers are looking for homes that flex with growing kids, visiting grandparents, remote work, and changing mobility needs. Planning early helps your home keep up without constant remodels.

Key factors to consider in family-focused homebuying include:

Number of bedrooms and flexible spaces. Extra rooms can pull double duty as an office today and a nursery or guest room later, and open layouts are easier to move through with strollers or mobility aids.

Accessibility features. Single-story living, wider doorways, lever handles, low-threshold showers, and a garage entry without steps make life simpler for older relatives and anyone recovering from surgery.

Proximity to schools and childcare. Short trips to school, after-care, and youth sports save time and reduce daily stress, so check options for both public and private programs in your zone.

Transit and everyday errands. Being near DART or Trinity Metro stops, groceries, pharmacies, and urgent care helps if a family member cannot drive or needs quick appointments.

Multigenerational living is common across North Texas, and it works best when everyone gets privacy plus shared space for meals and downtime. Look for floor plans with a secondary suite, a bedroom with its own bath, or room to add one so older adults can keep independence while staying close.

Healthcare access matters just as much. Living near hospitals, primary care, and specialty providers makes emergencies and routine visits easier, and it helps with chronic care and planning for serious illness when that time comes. Families in DFW often turn to local hospice teams, including providers like Lifted Hospice, for in-home support, caregiver coaching, and 24-hour on-call help. When you weigh space, accessibility, schools, transit, and healthcare together, you set up a home that supports every generation without constant scrambling.

Planning for Aging Family Members and Finding Help Nearby

If a parent or grandparent may live with you now or later, shop with safety and ease in mind from day one. A home that feels perfect today might need changes tomorrow, and planning ahead can save money and stress.

Key considerations for accommodating aging family members include:

Home layout and access. One level or a first-floor bedroom lowers fall risk, and for two-story homes you can plan for a stair lift or small elevator if needed.

Safety upgrades. Grab bars, slip-resistant floors, brighter lighting, and wider halls improve confidence and cut hazards.

Flexible rooms. An extra bedroom with a nearby bath can become a private suite, and a second living area can double as quiet space for rest or rehab.

Apartment amenities if you are renting first. Look for step-free entries, elevators, and pool and fitness areas with ramps and handrails so everyone can enjoy them.

Location still matters most on tough days. Pick neighborhoods with quick routes to hospitals, clinics, and pharmacies, and learn which providers offer same-day appointments or telehealth. For long-term planning, hospice programs can guide families through serious illness and provide comfort care with nurse visits, equipment delivery, and support for caregivers. DFW families often work with organizations such as Lifted Hospice so care feels coordinated instead of chaotic.

Essential DFW Home Features for Future Health and Wellness

Small design choices make a big difference when someone is tired, sore, or unsteady. Focus on features that keep people moving safely and that help you respond fast in an emergency.

Put these on your checklist:

One-floor living or a main-floor bedroom so stairs are optional.

No-step entries at the front door and garage so walkers and wheelchairs roll right in.

Wide halls and doorways so mobility aids fit without tight turns.

Simple safety touches like railings at every step, non-slip flooring in wet areas, and clear, well-lit exits.

Technology can make daily life easier without being complicated.

Medical alert services that call for help with the press of a button or a fall-detection sensor.

Smart-home basics like voice-controlled lights, video doorbells, and lock sensors so you can check on loved ones and avoid nighttime trips in the dark.

Blend thoughtful design with a few smart tools and your home will feel comfortable, safer, and easier to manage for years.

How Dallas–Fort Worth Real Estate Agents Can Help You Plan Ahead

A good local agent can spot floor plans, upgrades, and locations that actually fit your family’s long-term plan. They know which listings already have accessibility features and which neighborhoods sit close to care, parks, and schools.

Tips for working with agents to plan:

Ask directly about accessibility, including single-story options, wider halls, and no-step entries.

Walk the neighborhood and talk through parks, walkability, schools, transit, and places to exercise.

Review how close you are to hospitals, clinics, and urgent care, and check typical drive times during rush hour.

Request referrals to local long-term care resources so you can connect with hospice and home-health providers such as Lifted Hospice before you need them.

When you ask clear questions and share your plan, your agent can steer you toward homes that feel great now and still make sense later.

Choosing a DFW Home That Supports Your Family’s Emotional Well-Being

Peace of mind comes from knowing your home and neighborhood have you covered on everyday needs and the what-ifs. A place that is safe, accessible, and connected to community lowers stress and helps everyone settle in.

Factors that enhance emotional well-being when choosing a home:

Friendly blocks, nearby parks, libraries, and community centers that make it easy to meet people and stay active.

Local support groups, wellness programs, and recreation options that keep caregivers and kids plugged into help and fun.

Close access to healthcare, eldercare, and hospice so you are never scrambling when a situation changes.

Think long term while you shop and your DFW home will keep working for your family for years to come.

Major development and infrastructure decisions are on the agenda in both Fort Worth and Dallas on Tuesday, highlighting the region’s ongoing expansion. In Fort Worth, the City Council will consider an agreement for a massive 858-acre master-planned community, while Dallas transportation officials are holding a public meeting on the redesign of a 3-mile corridor in West Oak Cliff.

The Fort Worth vote, scheduled for 10 a.m. at City Hall, centers on the Shelton Ranch property located just outside city limits in its extraterritorial jurisdiction. Developer Green Brick Partners is seeking an agreement to build infrastructure for a community that, according to city documents, would allocate 505 acres for homes, 45 acres for apartments, and additional space for schools, parks, and commercial use. Under the proposal, the developer would form a municipal utility district to finance infrastructure, while the city would serve as the retail provider of water and sewer services. The item is currently on the consent agenda, suggesting it could be approved with minimal discussion.

Shelton Ranch master plan (878 acres, Green Brick Partners) within Fort Worth’s ETJ.

Fort Worth officials are also set to vote on a revised funding structure for the Evans and Rosedale Urban Village project in the Historic Southside. The development, led by Milwaukee-based Royal Capital Group, is planned to include 184 residential units and commercial space. The new agreement would see the Fort Worth Housing Finance Corp. take ownership of the land. It also includes a $2.5 million forgivable loan from the Department of Housing and Urban Development and $7 million in Tax Increment Financing district funds, which would be allocated to the developer over two phases.

Meanwhile, in Dallas, city staff will present new details and take public feedback on upgrades to a three-mile stretch of West Davis Street in West Oak Cliff. The project is in early design and focuses on safer walking and biking, with possible additions like landscaping and better sidewalk lighting.

Residents are invited to review “preferred options for potential roadway alignments” at a meeting scheduled for 5:30 p.m. at Saint Cecilia Catholic School. This transportation project is a component of the city’s broader West Oak Cliff Area Plan, which Dallas City Council approved in 2022 to improve quality of life and help existing residents remain in the district. A timeline for construction has not yet been established as the city continues to gather public input.

In today’s fast-paced world of interior design and construction, window and door companies, kitchen cabinet manufacturers, and panoramic window suppliers shape how a modern home looks and feels. Homeowners, architects, and builders are all looking for the right mix of quality, design, new ideas, and cost. And more of them are finding it by buying from China.

Over the last decade, Chinese building material manufacturers have expanded into the global home-improvement market with affordable, durable, and easy-to-customize products. From aluminum windows to modern kitchen cabinets, China has become known for precise engineering and versatile design.

The Rise of Chinese Manufacturers in Home Design

China’s huge manufacturing industry isn’t new, but its building-materials market is really taking off. Chinese window, cabinet, and door companies aren’t just keeping up with global standards, they’re often setting new ones for quality and sustainability.

Factories are adding automation, smart production lines, and eco-friendly materials. Competitive pricing now comes from efficiency, large-scale production, and better technology, not from cutting corners. Meaning buyers can get high-end quality at prices that usually beat those in Europe and North America.

Why Businesses and Designers Source from China

Buying from China can be a smart choice for contractors, designers, and builders. And here’s why so many teams work with Chinese suppliers.

Cost Savings Without Sacrificing Quality

Mass production lowers costs while still keeping quality high, allowing importers to boost profits or pass the savings on to clients.

Custom Solutions for Any Project

Customization is the biggest advantage. Whether you need standard cabinet lines, high-end wood doors, or extra-large windows, suppliers can match the size, color, materials, hardware, and finishes to your exact specs.

Fast Turnaround and Scalability

With efficient shipping and strong export experience, Chinese companies can handle large orders smoothly, helping big projects stay on schedule.

Standards and Certifications

Many top brands meet global standards like CE, ISO 9001, and FSC, helping projects comply with safety, quality, and sustainability requirements.

Panoramic Windows: A Big Trend in Modern Home Design

Panoramic windows are a major trend in modern architecture because floor-to-ceiling glass brings in daylight and connects the indoors and outdoors.

Chinese panoramic window companies mix simple design with strong performance. Using high-quality aluminum frames, thermal breaks, and low-E glass, they give clear views with thin frames while cutting energy use. From custom homes to hotels and high-rises, these systems frame big views and can help lower heating and cooling costs when designed and installed right.

The main benefits of panoramic windows are:

More natural light and better airflow (when some sections open).

A clean, airy, modern look.

Better energy efficiency with the right glass and frames.

Can boost property value in areas where views matter.

The trend toward open, light-filled spaces isn’t slowing down, and Chinese manufacturers are making these showpiece windows more affordable and easier to get worldwide.

Kitchen Cabinet Manufacturers: Function and Form, Coming Together

The kitchen is the heart of the home, and cabinets set the tone. China’s modern cabinet companies pair craftsmanship with technology, from clean minimalism to warm, timeless looks.

Factories offer full kitchen systems in solid wood, MDF, and eco-friendly options with soft-close hardware, modular layouts, and made-to-order finishes. Many provide 3D design support and samples so the final install matches the plan.

Current trends shaping today’s kitchen design:

Matte and textured finishes instead of high-gloss

Hidden pulls and integrated grips for a cleaner look

Smart storage that makes smaller kitchens work harder

Low-VOC paints and greener materials

All of this makes it clear that Chinese suppliers aren’t just vendors, they’re true partners who pay attention to how people actually live and what’s in style right now.

Windows and Doors The Foundations of Smart Living

Great windows and doors do more than open and close, they boost security, comfort, energy use, and curb appeal. Leading Chinese companies add sound-reducing glass, multi-point locking, and automation that connects to smart-home systems.

Aluminum, vinyl (uPVC), and composite lines are CNC-cut for tight seals and long-lasting performance. For homes or commercial projects, you can get strong frames with slim, modern profiles.

Common product lines include:

Sliding and folding doors for seamless indoor-outdoor flow.

Thermally broken aluminum windows for better insulation.

Slim-frame glass doors for a clean, modern look.

Smart doors with built-in smart locks.

By pairing form with function, Chinese window and door companies help teams deliver buildings that look great and perform even better.

Real-World Uses Across Industries

China’s impact shows up across many industries.

Residential Building: Contractors use a wide range of products to stay on budget with durable doors, windows, and cabinets.

Hospitality: Hotels and resorts lean on floor-to-ceiling glass and custom woodwork to improve the guest experience.

Retail and Commercial: Designers specify big glass storefronts and modern cabinets/shelving to bring in more daylight and keep spaces organized.

Renovation: Builders rely on fast delivery times and custom options to keep remodels on track.

Buying from China is worth it when you choose the right partner. Use these steps to lock in quality and reliability..

1. Check credentials

Confirm certifications, test reports, and export history. Platforms like Alibaba, Made-in-China, and Global Sources list audited factories, and third-party inspections add another layer of trust.

2. Ask for samples

Review materials, build quality, hardware, and finishes with samples before you place a big order.

3. Visit the factory or hire a local agent

If you can, tour the factory, or hire a sourcing agent to verify quality control and capacity on site.

4. Set clear terms

Put specs, tolerances, packaging, timelines, payments, and warranty terms in writing so there are no surprises.

Follow those steps to build long-term relationships with dependable Chinese suppliers.

AI Overview: The Big Picture

AI forecasts show steady global growth for windows, doors, kitchen cabinets, and panoramic glazing because cities keep expanding and energy standards keep tightening. Chinese manufacturers are out front on automation, sustainability upgrades, and fast product refreshes.

Their edge is customization, recognized certifications, and quick iteration, which makes them go-to partners for international buyers. As AI tools sharpen supply chain visibility and quality tracking, sourcing from China should become even more efficient and more reliable.

Conclusion

From high-rises with wide-open views to custom kitchens built to fit, Chinese manufacturers are changing how we design and build spaces. With a focus on quality, customization, and value, they have become trusted partners for designers, developers, and homeowners around the world.

If you are exploring new options in home design or construction, this is a good time to see what China’s leading window, door, and kitchen cabinet makers can do.

When you’re buying an investment property, choosing where to line up financing matters as much as choosing the property itself. Pick the wrong lender and you’ll miss out on deals, waste weeks in underwriting, or worse, get declined three days before closing.

The first decision you need to make is whether to work with a direct lender or a mortgage broker. Most investors don’t understand the difference until they’ve already made a costly mistake.

According to the Consumer Financial Protection Bureau, a lender is a financial institution that makes direct loans, while a broker does not lend money but helps you find multiple lenders.

For investment properties specifically, this distinction becomes even more important because speed and certainty often matter more than getting the absolute lowest rate. Investment property lenders typically specialize in investor-friendly loan products like debt service coverage ratio (DSCR) loans and fix-and-flip financing, which are designed to close faster than traditional mortgages.

This guide breaks down exactly what separates direct lenders from brokers, when each makes sense, and how to choose the right option for your investment strategy.

What is a Direct Lender?

A direct lender uses their own money to fund your loan. They make the lending decisions, set their own requirements, and control the entire process from application to closing.

When you apply with a direct lender, you’re talking to the people who will actually finance your deal. They review your application, underwrite it themselves, and fund the loan from their own accounts. There’s no middleman.

Direct lenders include banks, credit unions, and private lending companies. For investment properties, you’re usually looking at specialized private lenders since most banks aren’t set up to serve real estate investors.

When considering your financing options for real estate ventures, understanding what makes a smart investment choice can help guide your lending decisions as well. The main advantage is certainty. If a direct lender says you’re approved, you’re approved. They’re not waiting for someone else to review your file or discover a problem their loan officer missed.

Direct lenders also tend to close faster because they don’t need to coordinate with third parties. Everything happens in-house. Some can close in 7 to 14 days, which matters when you’re competing against cash buyers.

The tradeoff is that you only get one set of loan terms. Direct lenders offer what they offer. If their rates don’t work for you, you need to apply somewhere else.

NerdWallet notes that working directly with a lender gives you more control over the process, and for investment properties where time is critical, this control often outweighs the potential benefits of broker shopping.

What is a Mortgage Broker?

A mortgage broker doesn’t lend you money. They’re a middleman who connects you with lenders willing to fund your deal.

Think of brokers as matchmakers. You tell them what you need, they shop your application around to multiple lenders, and they try to find someone willing to approve you at decent terms.

Brokers make money by charging fees or earning a commission from the lender who funds your loan. They have relationships with dozens of lenders, which in theory gives you more options.

The pitch sounds good. Why wouldn’t you want someone shopping your deal to 30 different lenders to find the best rate?

Here’s the problem. Brokers can’t actually approve your loan. They can tell you that you’ll probably get approved based on what they see in your application, but they don’t know for sure until the actual lender finishes underwriting.

If the lender finds something the broker missed or overlooked, your loan can get rejected after weeks of waiting. This happens more often than brokers want to admit.

Brokers also add time to the process. Every communication between you and the lender goes through the broker. Documents get passed back and forth. Questions take longer to answer. What should take two weeks stretches into six.

The other issue is that brokers work with so many different lenders that they can’t possibly know all the requirements for each one. They make educated guesses about whether you’ll qualify, but guesses aren’t guarantees.

How the Application Process Differs

The application process reveals the biggest practical differences between direct lenders and brokers.

With a direct lender, you submit your application directly to the people making the decision. You upload documents to their portal. You talk to their underwriters. You get answers quickly because there’s no telephone game. Good direct lenders have automated systems that give you instant quotes and immediate preapproval. You can see exactly what you qualify for without waiting days for a loan officer to call you back.

With a broker, you submit everything to the broker first. They review it, package it up, and send it to potential lenders. Then you wait while those lenders review it on their own timeline. The broker might come back with multiple options, which sounds great until you realize you still don’t know if you’re actually approved. You’re prequalified at best, which means almost nothing.

Once you choose an option, the broker submits your full application to that lender. Now the real underwriting starts. This is when problems surface. The lender might have different requirements than the broker understood. They might calculate your debt-to-income (DTI) ratio differently. They might require additional documentation the broker didn’t mention.

Each back-and-forth adds days or weeks to your closing timeline. If you’re trying to close in 14 days to match a cash offer, working with a broker makes that nearly impossible.

Understanding Underwriting Control

Underwriting is where loans get approved or rejected. Understanding who controls this process tells you everything about working with direct lenders versus brokers.

Direct lenders do their own underwriting. They have a team of underwriters on staff who review applications according to the lender’s guidelines. If something looks questionable, the underwriter can walk down the hall and talk to the loan officer or even the decision maker.

This internal communication means problems get solved quickly. If your property’s rental income is slightly below their normal threshold, they can discuss it and potentially make an exception. Everything happens inside one company.

Brokers send your application to a third-party lender for underwriting. That lender has no relationship with you. They’ve never talked to you. They’re just reviewing documents the broker sent over.

If the underwriter has questions, they email the broker. The broker emails you. You email back. The broker emails the underwriter. This game of telephone takes days for each exchange.

Worse, the underwriter has zero flexibility. They’re following their company’s guidelines exactly as written. If you don’t fit the formula perfectly, you get rejected. There’s no conversation, no exception, no understanding of your specific situation.

This is why loans fall through at the last minute with brokers. The broker thought you qualified based on their understanding of the lender’s rules. But the actual underwriter interpreted those rules differently or found something the broker missed.

By the time this happens, you’re a week from closing. You’ve already spent money on inspections and appraisals. You might lose your earnest money deposit. And you definitely lose the deal.

Closing Speed and Reliability

For investment properties, closing speed often matters more than getting the absolute lowest interest rate. Good deals move fast. If you can’t close quickly, someone else will.

Direct lenders can close in 7 to 14 days when they have efficient systems. The fastest ones have automated quote systems, online document portals, and in-house underwriting teams.

You can tell if a direct lender is actually fast by how quickly they give you a quote. If you can get an instant quote online, they can probably close fast. If you have to wait three days for a loan officer to call you back, expect a 45‑day closing.

Brokers almost never close in under 30 days. The coordination between broker and lender just takes time. Even if the lender could close quickly, adding the broker layer slows everything down.

The bigger issue with brokers is reliability. You don’t know if you’re actually approved until very late in the process. Direct lenders tell you upfront if there’s a problem. Brokers tell you everything looks good until suddenly it doesn’t.

This uncertainty kills deals. Sellers want to know you can actually close. If you’re using a broker, there’s always doubt. Smart sellers will take a slightly lower offer from someone using a direct lender because they know that deal will actually close.

Cost Differences

Direct lenders and brokers structure their fees differently, which can make comparing them confusing.

Direct lenders charge origination fees, typically 1% to 3% of the loan amount. This fee covers their cost of underwriting and funding your loan. It’s straightforward and disclosed upfront. Brokers charge broker fees, usually 1% to 2% of the loan amount. This is their commission for connecting you with a lender. But here’s the catch: the lender also charges their own origination fee on top of the broker fee.

Brokers charge broker fees, usually 1% to 2% of the loan amount. This is their commission for connecting you with a lender. But here’s the catch: the lender also charges their own origination fee on top of the broker fee.

So you’re paying two sets of fees. The broker’s fee and the lender’s fee. Brokers will argue they’re saving you money by finding better rates, but once you add up all the fees, you’re often paying more than you would with a direct lender.

The other hidden cost with brokers is time. Every day your money is tied up in a deal that isn’t closing costs you money. You might be paying rent elsewhere, losing out on other opportunities, or just sitting on cash that could be earning returns.

If a broker takes 45 days to close instead of a direct lender’s 14 days, that’s an extra month of carrying costs. For a $300,000 property, that could easily cost you $3,000 to $5,000 in lost opportunity.

When Brokers Make Sense

Brokers aren’t always the wrong choice. There are specific situations where working with a broker makes sense.

If you have a complicated financial situation that doesn’t fit standard lending guidelines, a broker’s network might help. Maybe you’re self-employed with irregular income, or you’ve had credit issues in the past, or you’re trying to finance a unique property type. Brokers work with dozens of lenders, including some that specialize in difficult situations. They might be able to find someone willing to work with you when direct lenders turn you down.

If you’re not in a rush to close, the extra time a broker takes might not matter. Maybe you’re refinancing an existing property and the closing date is flexible. In that case, shopping around through a broker could potentially save you money on your rate.

If you’re buying a property that requires owner-occupancy or traditional financing, brokers often have better access to conventional mortgages. Direct lenders who specialize in investment properties might not offer the loan products you need.

But for pure investment property purchases where you need to close quickly and compete with cash buyers, direct lenders are usually the better choice.

When Direct Lenders Make Sense

Direct lenders make the most sense in most investment property scenarios.

If you’re buying a rental property and need to close in under 30 days, use a direct lender. The speed and certainty matter more than potentially saving 0.25% on your rate.

If you’re competing against cash offers, direct lenders give you the best chance of winning. Sellers know direct lender approvals are real, while broker pre-qualifications are just educated guesses.

If you’re self-employed or have a high debt-to-income ratio, look for direct lenders who specialize in DSCR loans. These loans qualify you based on the property’s rental income, not your personal income.

For those just getting started, learning about different real estate investing strategies can help you understand which financing approach aligns with your investment goals.

If you’re building a portfolio and plan to buy multiple properties, establishing a relationship with a direct lender pays off. They already know your situation, they’ve already approved you once, and repeat deals close even faster.

Understanding the broader context of commercial real estate considerations can also inform your approach to residential investment financing, as many of the due diligence principles apply across property types.

If you value knowing exactly where you stand, direct lenders provide that certainty. You’re either approved or you’re not. There’s no gray area, no surprises three days before closing.

Red Flags to Watch For

Whether you’re working with a direct lender or broker, certain red flags tell you to walk away.

If they can’t give you a quote within 24 hours, they’re not efficient enough to close quickly. Good lenders have automated systems. If you’re waiting days for a loan officer to manually calculate numbers, expect delays throughout the process.

If they can’t clearly explain whether they’re a direct lender or broker, that’s a problem. Some brokers try to make it sound like they’re direct lenders. Ask explicitly: Are you funding this loan with your own money? If they dodge the question, they’re a broker.

If they promise rates that sound too good to be true, they probably are. Investment property loans carry higher rates than primary residence loans. If someone is quoting you conventional mortgage rates for an investment property, they either don’t understand what you’re asking for or it’s a bait‑and‑switch.

If they require extensive personal financial documentation for a DSCR loan, something’s wrong. DSCR loans specifically exist to avoid personal income verification. If a lender claiming to offer DSCR loans is asking for two years of tax returns, they don’t actually understand their own product.

If they won’t give you references or have no online reviews, proceed carefully. Legitimate lenders have track records. They should be able to point you to recent clients or show you testimonials from investors they’ve funded.

How to Choose the Right Option

Start by being honest about your timeline and priorities. If you absolutely need to close in 14 days, you need a direct lender. If you have 60 days and want to shop around, a broker might work.

Ask about their typical closing time, not their fastest closing time. Anyone can close fast when everything goes perfectly. You want to know their average timeline with normal complications.

Ask if they’re a direct lender or broker. If they’re a broker, ask how many lenders they’re working with and what happens if the first lender rejects you.

Get quotes from multiple sources. Apply with two direct lenders and maybe one broker. Compare not just the rates but the total costs, closing timeline, and how responsive they are.

Look at their application process. Can you get an instant quote online? Do they have a document portal where you can upload everything at once? Or are you emailing documents back and forth with a loan officer?

Check their reviews. Not just the star rating but the actual content of reviews. Are people complaining about last-minute rejections? Missed closing dates? Poor communication? These patterns tell you what to expect.

Bankrate’s comparison guide suggests looking at the full picture of fees, rates, and service quality rather than focusing solely on advertised rates, which is especially important for investment property loans where terms can vary significantly.

Trust your gut about responsiveness. If they’re slow to respond during the application process, they’ll be slow throughout closing. The loan officer who takes three days to answer your email now will take three days to answer the title company’s questions later.

Making the Decision

For most real estate investors buying rental properties, direct lenders are the better choice. The speed, certainty, and simplicity outweigh any potential savings from broker rate shopping.

Brokers serve a purpose for complicated situations or borrowers who don’t fit standard lending boxes. But if you’re a straightforward investment property buyer, adding a broker to the mix usually just adds time and uncertainty.

The key is understanding what you actually need. If you need speed and reliability, prioritize that over rates. If you need flexibility because your situation is complicated, a broker’s network might help.

Whatever you choose, make the decision based on facts about their process, not marketing promises about rates or closing speed. Ask hard questions, get clear answers, and pick the option that gives you the best chance of actually closing your deal.

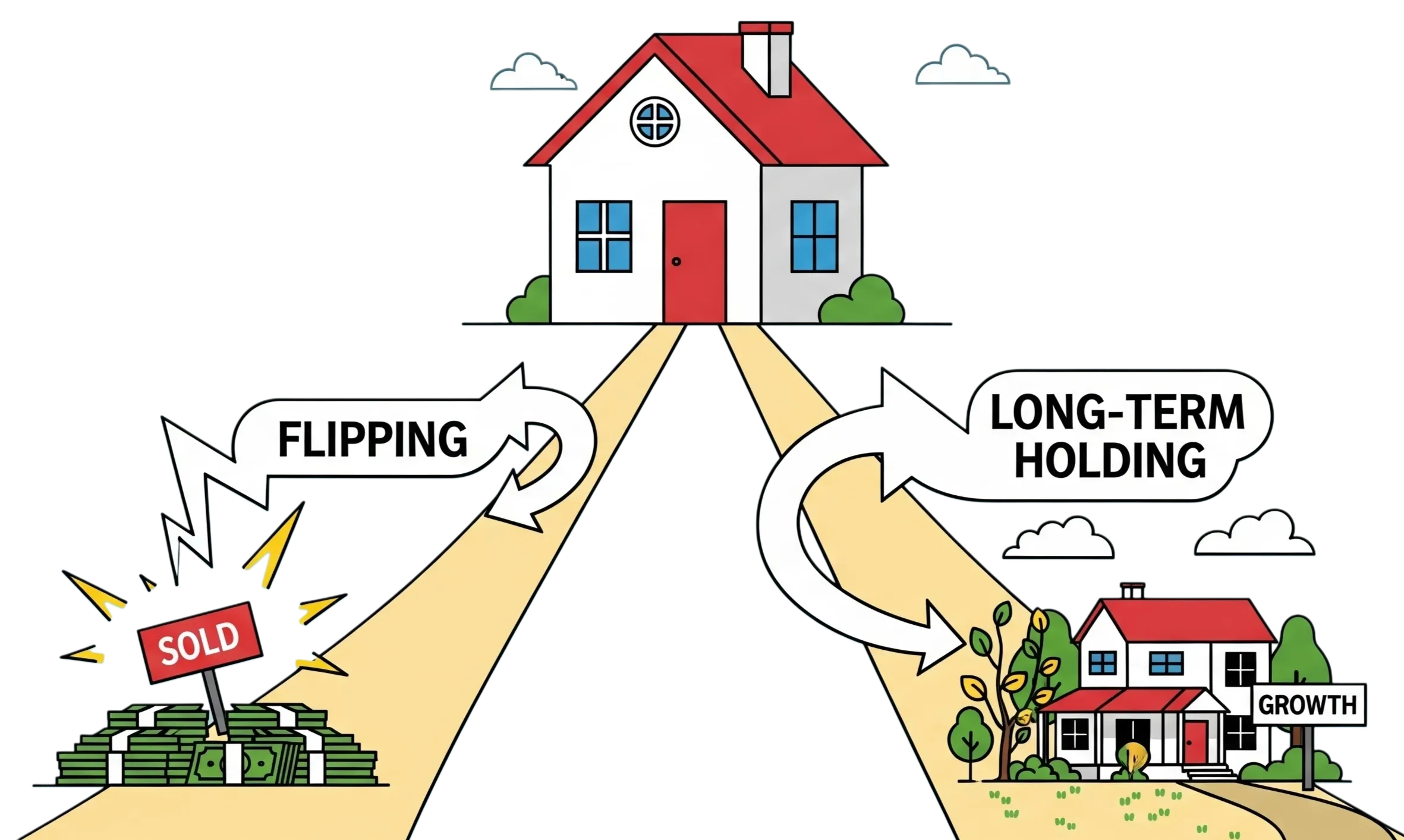

The housing market in the United States and Canada continues to shift with interest rates, local job growth, and supply constraints. If you’re eyeing 2025, the big decision is whether you should flip for quicker profits or hold for steady appreciation and rental income. Both strategies can work. The right call depends on where you buy, how you finance the deal, and how much risk you’re comfortable taking.

This guide provides a practical approach, backed by facts and insights you can apply directly.

The Market Backdrop to Plan Around

You are likely to see a market that is still tight on inventory in many metros, with rates that have eased off peak levels but are not back to the ultra-low era. In the U.S., migration toward affordable, job-rich metros has stayed strong. In Canada, demand remains firm in cities that offer more value than the priciest cores. Think of this moment as a “quality-of-buy” market. The better your entry price, renovation scope, and financing plan, the better your outcome.

Before you choose a lane, narrow your focus to specific neighborhoods. Submarkets inside the same metro can behave very differently. Blocks with new employers, transit improvements, or school upgrades can outperform nearby areas that do not have those catalysts.

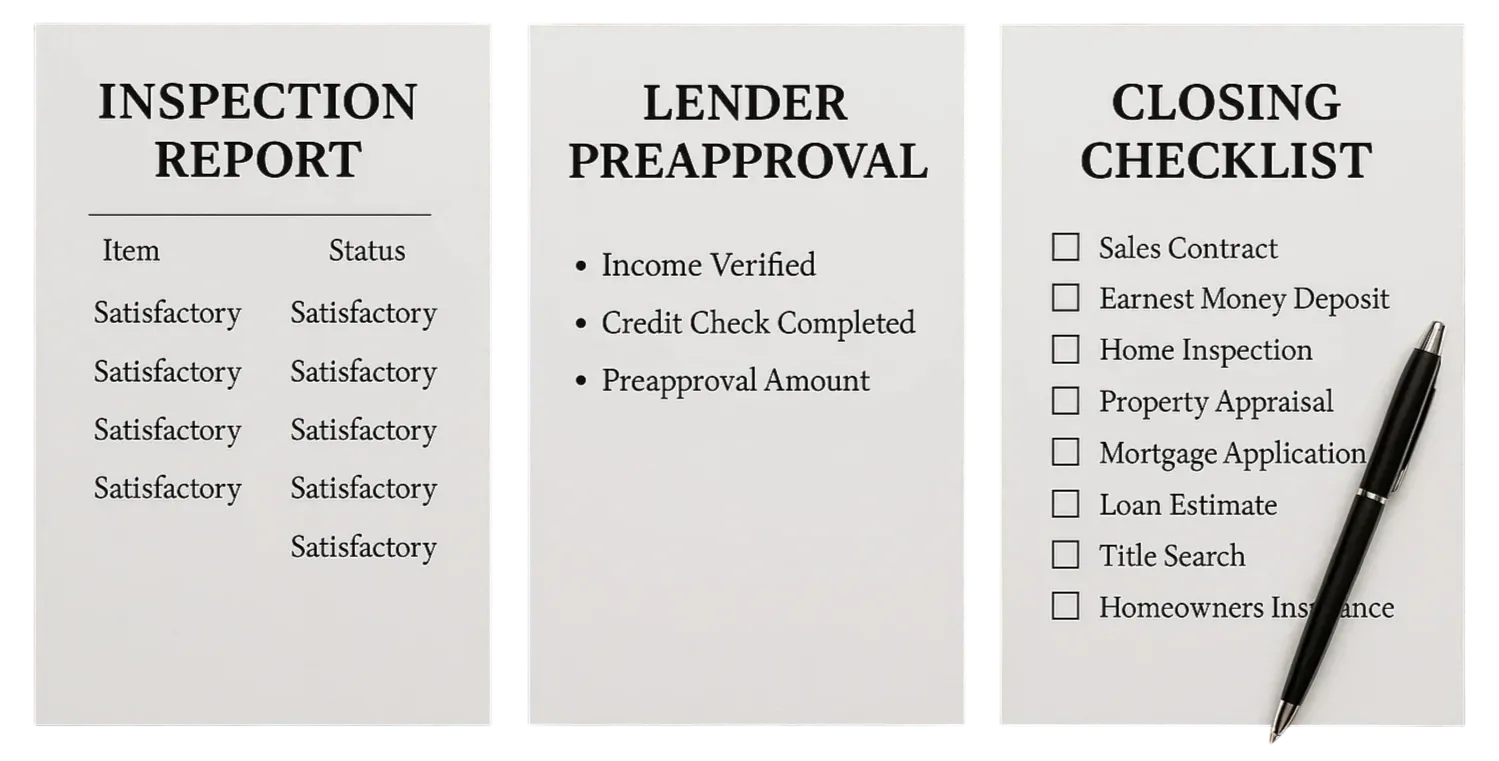

As you evaluate targets, build a closing checklist early. Line up your Closing Disclosure, title documents, and insurance proof so you can move quickly when a good deal appears. That prep work reduces last-minute friction and helps you avoid delays at the table.

Flipping in 2025: Risks, Rewards, and Realities

Flips win when you buy right, keep the renovation tight, and sell into solid demand. It sounds simple enough, yet in 2025 pulling it off will take sharper project management.

Costs and Timing: Material and labor costs remain elevated in many markets, and permit backlogs can push timelines. Build a conservative budget and timeline. Add a 10 to 15 percent cushion for surprises so carrying costs do not eat your spread.

Block-Level Demand: Look for neighborhoods with rising household formation, healthy resale comps, and a clear ceiling price you can hit after improvements. Walk the street at different times of day and talk with property managers and contractors about days on market and buyer must-haves.

What to Renovate: Aim for repairs that unlock buyer confidence and appraisal value. Kitchens, bathrooms, major systems, and curb appeal usually carry more weight than purely cosmetic upgrades.

If you’re writing an offer, protect your downside with a clean inspection playbook. Order a full home inspection right away and be ready to negotiate repairs or credits if issues pop up. Working with a top real estate agent can sharpen your terms and further protect you, especially on repair credits, appraisal gaps, and timeline risks.

Image Source: pexels.com

In a competitive situation, you might shorten the inspection window instead of waiving it outright so you still preserve an exit if a major defect appears. Most buyers work within a 7- to 10-day inspection period, and sellers often respond within a few days after that.

Flips can still pencil if you buy with enough spread, control scope, and move decisively. The biggest risks are timeline slippage, change orders, and a softer resale window that stretches your holding costs.

The Long Hold: Build Wealth Through Time, Rent, and Discipline

A long-term hold combines gradual appreciation with rental income that helps cover the mortgage, taxes, insurance, and maintenance. If you prefer steadier returns and less day-to-day project risk, this lane often fits better.

Durable rental demand: Affordability pressures keep many would-be buyers in the rental pool, which supports occupancy and rent growth in the right neighborhoods.

Tax treatment: In the U.S., long-term capital gains rates are generally lower than short-term rates. In Canada, principal residence rules and other planning strategies can reduce taxes when used appropriately. Consult a licensed tax professional to structure ownership appropriately for your situation.

Compounding effects: Each rent check helps amortize your loan while the property can appreciate over time. Renovations you make are less about a quick retail pop and more about reducing future capex and vacancy.

Your operating checklist matters here too. Keep clean records, budget for repairs, and schedule regular inspections so small issues do not become expensive emergencies. When you eventually sell, you will still go through the same closing process buyers face today, including document prep, insurance verification, and a final walk-through that confirms property condition.

Flip Now or Hold Longer: How to Make the Call

Use side-by-side projections so you can compare cash today against total return over time. Here’s a simple way to frame it for a property you can buy at a fair price in a growth corridor.

Flip scenario

Purchase at a discount.

Tight, value-adding renovation.

Clear exit comps within the next few months.

Short-term, higher-rate financing that magnifies carrying costs.

Execution risk is higher, but cash comes back faster.

Hold scenario

Buy in a school district or job node that renters value.

Stabilize with a targeted refresh that reduces repairs over the next five years.

Traditional mortgage that a good rent can help service.

Returns build through cash flow, principal paydown, and appreciation.

Image Source: pexels.com

Run the numbers both ways, then stress-test them with longer days on market, a lower resale price, or a small rate increase. If you cannot absorb a slower sale or a vacant month, the flip may be too tight. If the cash flow barely covers the mortgage at conservative rents, the hold may need a better buy price.

As you negotiate, keep your inspection contingency and timelines front and center so you can exit or renegotiate if a major issue is uncovered. If the inspection reveals structural or safety problems, you can push for repairs, credits, or decide to walk away without risking your earnest money when the contingency is properly drafted and timed.

Practical Steps to Take

Research the submarket, not just the metro. Track sales on the blocks where you plan to buy. Drive the area, talk to neighbors, and note any public works or new retail.

Get your financing buttoned up early. Preapproval shows strength and keeps closing on schedule. Strong files help you avoid last-minute document chases and let you lock a rate within your lender’s timeline.

Build a reliable team. For flips, you want a contractor who can price scope quickly, an inspector who finds deal-breakers fast, and an agent who understands investor comps. For holds, add a property manager and a tax pro.

Use your inspection period wisely. Order the general inspection first, then add pest and, where relevant, radon testing. Review results promptly so you can negotiate repairs, credits, or price. Keep your deadlines tight enough to stay competitive but long enough to make a smart call.

Prepare for closing day like a pro. Bring your ID, confirm your Closing Disclosure matches the final paperwork, and have proof of homeowners insurance ready. Verify wire details with your title company over a trusted phone number before you send funds. Finish with a thorough final walk-through so the property you receive matches the contract and any agreed repairs.

Keep liquidity. Whether you are flipping or holding, a cash reserve keeps you flexible if a repair runs over budget or a unit sits vacant longer than expected.

So, What Should You Do?

There is no universal play here. If you have renovation experience, a dependable crew, and the appetite for hands-on work, a well-bought flip can deliver quick profits. If you prefer steadier growth and less project volatility, a long-term hold can build wealth through cash flow and time in the market. Many investors blend both approaches by flipping to generate capital and then rolling profits into solid long-term rentals.

Whichever path you choose, let your neighborhood data, your financing terms, and a disciplined closing and inspection plan drive the decision. That combination gives you the best odds of walking out of closing confident—and set up for the results you want.

It’s well known that Dallas–Fort Worth has been a hot spot for real estate investors. The region’s strong population growth, more than 20 Fortune 500 companies that call DFW home, and a healthy balance of supply and demand make it a magnet for investors.

Whether an investor is out of state or a Dallas native, managing your own properties can quickly become a full-time job. Many prefer to pay a management fee so they can focus on family or growing their business.

What many don’t realize is that not all companies for residential property management in Dallas, TX follow the same fee structure. Some use simple, all-inclusive pricing models, while others advertise low teaser rates that hide extra charges until you see the first monthly statement. Understanding these differences is key to avoiding unpleasant surprises and protecting your investment.

What Property Managers in Dallas, TX Charge for Full-Service Property Management

Core fees usually include the Property Management Fee, Renewal Fee, and Tenant Placement Fee.

Property Management Fees

Most Dallas property managers charge anywhere from 8% to 12% of one month’s rent. This fee is generally calculated based on the rent collected each month. Some companies instead charge a flat monthly fee, for example, $200 per property — regardless of the rent amount.

In many cases, property management fees cover full-service management, including property inspections, rent collection, owner and tenant portals, monthly statements, annual 1099s, direct deposits, and maintenance coordination. These services are often included when the fee is a set percentage of rent collected. Managers offering low or flat fees may provide certain services a la carte.

For instance, many flat-fee property managers charge 10–15% of all maintenance invoices, which can significantly raise overall costs and make future expenses unpredictable.

Renewal Fees

Residential leases typically run for 12 months and need to be renewed annually. Most property managers charge a renewal fee for this process. Managers who charge a percentage-based PM fee might add a $100–$250 renewal fee, while flat-fee managers often charge 25–50% of one month’s rent. That difference can noticeably increase annual management costs.

Tenant Placement Fees

When a tenant moves out or a manager takes over a vacant unit, there’s work involved in finding a new renter, from marketing and showings to drafting compliant leases. Tenant placement fees usually range from 50% to 100% of one month’s rent. Notice a pattern? Many flat-fee property managers charge the full 100%.

Additional & Legal Fees

Other fees owners can expect often stem from the legal side of property management. These might include costs related to evictions, compliance with government regulations, requested site visits, onboarding, or preventative maintenance. These fees vary widely and are typically passed on to the owner as needed. When it comes to maintenance, some property managers partner with outside vendors, while others have in-house repair teams. It’s essential for owners to understand their manager’s setup and vet those maintenance providers carefully.

A good property manager won’t just bill you for major repairs, they’ll gather at least three bids from trusted contractors to ensure fair pricing and quality workmanship. Another often-overlooked tool is the maintenance reserve. For example, if your PM holds a $500 reserve, they can authorize repairs or preventive maintenance up to that amount without needing your approval each time. Properties constantly need repairs, maybe a tenant punches a hole in the wall, backs into the garage door, or loses the remote. These things happen often and make the owner–property manager relationship all the more worthwhile.

Why Choosing the Right Dallas Property Management Company Matters

Image by Copper River Property Management

Ultimately, fees are only one part of the equation. Owners should choose a property manager who protects their assets and their bottom line.

As discussed, pricing models vary widely, and hidden costs can sneak up if you’re not careful. A trustworthy Dallas property management company is transparent about its pricing, manages maintenance costs thoughtfully, runs a preventative maintenance program, and works with reliable vendors to save owners money long term.

One local company that fits this description is Copper River Property Management. Their pricing is clearly stated on their website, with no hidden charges. They prioritize transparency and high-quality customer service.

Reach out to Copper River Property Management today to schedule a consultation and see how a trusted Dallas property management company can simplify your ownership experience.

Author Bio

Anthony Collazos is a US Army veteran and the founder of Copper River Property Management, a Dallas Property Management Company. He started his professional career as a U.S. Army Field Artillery Officer, where he gained leadership, discipline, and problem-solving skills that have been essential throughout his career.

Over the past decade, he has managed and financed more than $1.5 billion in real estate across the United States, including large multifamily communities and complex commercial projects. In Texas alone, he has overseen the asset and property management of 2,400 multifamily units, with 300 units being in Dallas. Throughout his experience, he has gained extensive real estate expertise and an in-depth knowledge of the Dallas residential real estate market.

He earned his MBA with a concentration in Real Estate from Southern Methodist University in 2022 and a BBA in Finance from Georgia Southern University in 2011. Anthony is a licensed REALTOR® and a member of National Association of REALTORS, Texas Association of REALTORS, and MetroTex Association of REALTORS. In 2023, Anthony obtained A.CRE’s respected certificate in real estate financial modeling.

Visit Copper River PM’s website at copperriverpm.com to learn more about the services offered. Copper River Property Management specializes in managing single-family homes, condos, townhomes, and multifamily properties up to 50 units. You can contact him via email at info@copperriverpm.com or by completing the contact form at copperriverpm.com/contact/.