The Dallas-Fort Worth metroplex is adding thousands of new residents every year, and 2026 will likely be no different. Whether you’re moving for a new job, a more affordable cost of living, or just a change of scenery, this guide will help you get up and running.

Here’s what you need to know about the local market, neighborhoods, and logistics before you pack your bags.

Why People Are Moving to DFW

The DFW area consistently ranks as one of the fastest-growing metros in the country. The reasons are simple: Texas has no state income tax, which can put more money in your pocket from day one.

The job market is diverse, from tech and healthcare, to finance, logistics and manufacturing. Big companies like Toyota, AT&T and American Airlines have a strong presence in the area and the startup scene is booming. For anyone moving here, the economic opportunity is a major draw.

Choosing a City in the Metroplex

DFW is sprawling—covering more than 9,000 square miles across 11 counties—so your first big decision is where to put down roots. Every city has its own distinct vibe.

Dallas is more city-like with great food, arts and nightlife. It’s a good fit if you want walkable areas and city energy.

The culture in Fort Worth is more laid back western type, with a strong community. Housing can also be slightly more affordable.

Plano and Frisco are top choices for families because of their highly rated schools and newer suburban neighborhoods.

Located between Dallas and Fort Worth, Arlington makes it easier to commute to either side of the metroplex.

If you’re a frequent traveler who needs fast access to DFW Airport, Irving and Coppell are worth considering.

Before signing a lease or buying a home, do research on which city will suit your lifestyle, commute and budget.

DFW Cost of Living in 2026

DFW remains cheaper than many large cities on the coast, but housing costs have gone up. Home prices vary widely by ZIP code, so budget wisely. Everyday expenses like groceries and utilities tend to stay relatively close to the national average, but your exact costs will depend on where you live and how far you commute.

Getting Around the Metroplex

Owning a car is practically a must. The highway system is massive, and the metroplex is spread out. While DART (Dallas Area Rapid Transit), provides rail and bus service within Dallas and some suburbs, it doesn’t cover the entire metro area. If you’re commuting, map out your drive during peak hours before signing a lease. Traffic on major corridors like I-35E, I-635, and the Dallas North Tollway gets notoriously heavy during rush hour.

Planning Your Move

If you’re coming from out of state, visit first to tour neighborhoods in person instead of relying strictly on photos.

Many newcomers who are moving to Dallas find it helpful to hire professionals familiar with the city’s layout, building access policies, and high-rise move-in procedures, if applicable.

Things to Do After You Move

Get your Texas driver license through the Texas Department of Public Safety within 90 days of moving.

Set up utilities like electricity, water, gas, and internet as soon as you have a move-in date. Since much of Texas has a deregulated energy market, you may need to choose a retail electric provider depending on your address.

Find nearby healthcare providers, including a primary care doctor and a dentist.

Explore your neighborhood to find the closest grocery stores, pharmacies, and parks.

Finding Community

If you are moving to DFW, you will want to find your tribe. Check out community groups, neighborhood associations, and professional groups. Most cities in the metroplex have regular events such as farmers markets and outdoor concerts where you can meet people.

If you have children, joining their school or sports teams is a quick way to grow your social network. Volunteer groups and local hobby clubs are also good ways to meet new people.

Making DFW Your New Home

Moving is a big adjustment, but a good plan makes the transition much easier. Check out the different neighborhoods at your own pace, and you’ll be settling into your new DFW life in no time.

If you’ve lost your home to foreclosure, you’ve probably heard the same advice. Rent for a few years. Rebuild your credit. Apply for an FHA loan when the waiting period ends.

That’s not wrong. But it skips the hardest part.

Nobody tells you that foreclosure makes renting hard, too. Or that how you rent during those years is going to affect whether you can actually buy again when the time comes.

Foreclosure Doesn’t Just Hurt Your Mortgage Chances

So here’s what catches you off guard. A foreclosure doesn’t only matter when you apply for another mortgage. Tenant screening reports can include information from credit reports, too. And most Dallas apartment communities run tenant screening, credit checks, or both.

A lot of management companies may treat a foreclosure as a serious rental risk, especially when it appears alongside late payments, collections, or other negative credit history. Some will decline automatically. No conversation, no context, no second look.

So you go online, pick a community that looks good, pay the $15 to $50 nonrefundable application fee, sometimes more at larger communities, and get denied. You try another one. Denied again. A third. Now you’ve burned through $45 to $150, maybe more, and you still don’t have a place to live.

That’s not a credit problem. That’s an information problem.

Some Dallas communities will absolutely work with you if you have a foreclosure on your record. Others won’t. Period. The difference is knowing which ones before you apply.

Now, if your credit has already bounced back above 620 and the foreclosure is more than three years behind you, you can probably handle this search on your own. But if you’re still inside that window, or your score is somewhere in the 500s, good luck getting approved without some help.

The Part That Affects Whether You Can Buy Later

This is something you don’t think about until it’s too late.

The FHA waiting period after foreclosure is generally three years. And that clock usually starts from when title transferred out of your name through the foreclosure sale or deed-in-lieu, not when you first missed a payment. After those three years, you may be able to qualify for an FHA loan with a credit score of 580 or higher and a down payment as low as 3.5%, as long as the rest of your file qualifies.

That’s a real path back to buying a home. But there’s more to it.

When a lender reviews your file, they’re not just looking at your credit score. They want to see what you did during those three years. FHA now allows positive rental payment history to be considered in certain first-time homebuyer files, and that means 12 months of on time rent payments they can actually check. A lease in your name, paid on time every month, to a landlord or management company that will confirm it in writing.

That’s the difference between a strong application and a weak one.

And here’s where a lot of you run into trouble. If you can’t get approved at a conventional apartment, you end up in a rental that won’t help you when it’s time to buy. A cash only room off Craigslist. Some month to month setup with a private landlord who doesn’t keep records. Or a sublease where your name isn’t even on the agreement.

Those arrangements keep a roof over your head. They won’t help you get a mortgage.

Think about it this way. Two people walk into a lender’s office with the same 590 credit score. One has three years of on time rent payments from a management company that picks up the phone when the lender calls. The other has a Venmo trail to a roommate. Not the same position.

What to Look for in Your Next Apartment

If you want to buy again, pick your apartment carefully. A few things matter more than the amenities list.

A lease in your name. Not a sublease, not some handshake deal. Your name on a 12 month lease with a property management company.

A management company that will verify your rent payments. When your future lender calls to confirm your payment history, someone needs to answer that call and put it in writing.

A community that will actually approve you. They exist all over Dallas. Some management companies will actually look at your situation instead of just running a score. Others have programs that can help you get approved even with bad credit, as long as you have the income. If you’re not sure where to start, second chance apartment leasing in Dallas can point you in the right direction.

While you’re renting, don’t forget about your credit. Get a secured credit card and keep a small balance paid in full every month. Don’t use more than 30% of your total credit limit. And above all, no new negative marks. One late payment or new collection can set the whole timeline back.

Don’t Treat Renting Like Dead Time

The biggest mistake you can make? Treating the rental period like it’s just something to get through before the real goal starts.

It’s not. Those three years are when you prove to a lender that you can handle a mortgage. The right apartment gives you stable housing now and a payment history that backs you up when you’re ready to apply.

And if you’re in DFW and thinking about what comes next, start figuring this stuff out now. It makes everything easier.

Congratulations on finding the right home for your family. Now comes the part most people do not exactly love: moving.

Hiring professional movers can take a lot of stress off your plate, but there are still several things you should do before moving day. A little planning can help protect your belongings, keep the day organized, and make the transition into your new home much smoother.

Here are practical steps to help you prepare.

Start Packing and Sorting Early

Packing is not the most exciting part of moving, but starting early makes a big difference. If you have a few weeks before the move, begin by going room by room and sorting your belongings into four categories: keep, sell, donate, and throw away.

The less you move, the less you have to pack, carry, unload, and unpack later.

Start with items you do not use every day, such as seasonal clothing, books, decorations, extra linens, and rarely used kitchen items. Save daily essentials for last.

As you pack, label each box clearly. Include the destination room, a short list of contents, and notes such as “fragile,” “heavy,” or “open first.” It may feel tedious while you are doing it, but it saves a lot of time when you are trying to find your clothes iron, phone charger, towels, or coffee maker after the move.

It also helps to pack one essentials box or bag with items you will need right away, such as toiletries, medications, chargers, basic tools, paper towels, snacks, important documents, and a change of clothes.

Confirm Details Before Moving Day

A few days before the move, confirm the schedule with your movers and anyone else helping you. Make sure everyone knows the arrival time, addresses, parking instructions, gate codes, elevator access, and any special details about the home.

You should also take photos of furniture, electronics, appliances, and fragile items before they are moved. These photos can help if anything is damaged or needs to be reassembled later.

Before the crew arrives, clear walkways in both homes. Remove tripping hazards, secure loose rugs, and make sure doors, hallways, stairs, and driveways are easy to access.

Prepare the Home for Movers

Moving day goes faster when your home is ready before the first box leaves the house.

If possible, disassemble large furniture ahead of time or confirm whether the movers will handle it. Tape hardware in a labeled bag and attach it to the furniture it belongs to. Unplug appliances and electronics, wrap cords, and label cables so setup is easier later.

Keep valuables, passports, financial documents, jewelry, medication, and personal records with you instead of loading them onto the moving truck.

You should also set aside items that movers may not be allowed to transport, such as paint, propane tanks, gasoline, certain cleaners, pesticides, and other hazardous materials. Dispose of these items safely according to local rules before moving day.

Keep Moving Day Organized

Moving day can get hectic fast, so it helps to have one person directing traffic. This person can answer questions, tell movers where items go, and make sure boxes are loaded and unloaded in the right order.

Here are a few smart moving-day tips:

Keep children and pets away from the work area.

Have water and simple snacks available.

Keep your phone charged.

Make sure the essentials box stays with you.

Do one final walk-through before leaving the old home.

Check closets, cabinets, drawers, the garage, the attic, and outdoor storage areas.

Even with a solid plan, small things may go wrong. A box may end up in the wrong room, or a piece of furniture may need to be moved twice. Stay flexible. Protecting your floors, walls, furniture, and people matters more than making every detail perfect.

Consider Portable Moving Containers

If you want more flexibility, a portable moving container can be a helpful option. Services such as you pack we move deliver a mobile container at your door step and allow homeowners to pack their belongings at their pace. Once it is loaded, the company picks it up and transports it to your new home or stores it until you are ready.

This can be useful if you need more time to pack, want to avoid driving a rental truck, or prefer to spread the work over several days instead of doing everything at once.

Unload With a Plan

Once you arrive at your new home, focus on the essentials first. You do not need to unpack everything all at once.

Start with the rooms you will need right away: bedrooms, bathrooms, and the kitchen. Set up beds, towels, toiletries, basic kitchen items, and anything you need for the first night.

Before opening every box, check the locks, utilities, appliances, lights, plumbing, and major systems. Make sure everything is working as it should.

As boxes come in, keep them grouped by room. This makes unpacking faster and helps prevent clutter from spreading through the whole house.

Take Care of Yourself During the Move

Moving is physically and mentally draining, even when everything goes well. Take short breaks, drink water, eat something simple, and stretch when you can.

Do not feel pressured to finish the entire house in one day. Start with what you need to sleep, shower, eat, and function. The rest can happen step by step.

Final Thoughts

Moving to a new home can be stressful, but it becomes much easier with the right preparation. Pack early, label boxes clearly, confirm details with your movers, keep important items with you, and focus on the essentials when you arrive.

A move is not just about getting your belongings from one place to another. It is the start of a new chapter, and a little planning can help you begin it with less stress and more confidence.

When you’re looking to buy a house, a new kitchen, fresh paint, and modern finishes are easy to notice. But foundation problems are much easier to miss, and they can be far more expensive to ignore.

The foundation affects the entire structure of a home. Cracks, settlement, drainage problems or movement can mean expensive repairs after closing. Having the foundation inspected before you buy can help you catch red flags early.

Foundation Problems Can Spread Over Time

Foundation issues don’t always stay put. Movement in the foundation can show up in walls, floors, ceilings, doors, windows, and even plumbing systems. A small crack may not seem like a big deal at first. But if you see it with uneven floors, sticking doors, gaps around windows, or cracked drywall, it could be a sign of a more serious structural problem.

These warning signs don’t necessarily mean the home has serious foundation damage. Still, they shouldn’t be overlooked. As the problem gets worse, the damage can spread to other parts of the home.

Catching Problems Early Can Lower Repair Costs

Some buyers assume foundation concerns can wait until after closing. That can be a costly mistake. Minor settlement, drainage problems, or small cracks are often easier to address when they are found early.

More serious repairs might involve installing piers, stabilizing slabs, improving drainage, or doing crawlspace work, all of which can quickly add up, especially if the damage has already impacted floors, walls, or plumbing. Finding these problems before buying gives you a clearer picture of what the home may really cost.

Inspections Give Buyers More Negotiating Power

A foundation inspection gives buyers facts to work with instead of guesswork. If the report shows movement, damage, drainage problems, you can use that to negotiate.

The seller may agree to do repairs, lower the purchase price or give a credit at closing. You also may opt to have a structural engineer or foundation specialist come in for a more in-depth look. Sometimes, the inspection confirms that the problem is manageable. Other times, it helps you steer clear of a home that has more risk than you’re willing to take on.

Don’t Overlook Peace of Mind

When you buy a home with unresolved foundation issues, it can leave you worrying about every new crack, sloped floor, or sticking door. A foundation inspection doesn’t guarantee a perfect home, but it does give you more clarity. It gives you an idea of the structure’s condition, whether repairs might be needed, and whether the purchase is still within your budget.

That kind of clarity can save you money and stress long after closing. Checking a home’s foundation before buying is one of the smartest ways to avoid expensive surprises. In Dallas and across North Texas, where expansive clay soils and moisture changes can put added stress on foundations, structural concerns are especially important to catch early.

Before you commit to a home, take the time to understand what is happening beneath it. A solid foundation protects more than the house. It can help protect your budget.

If you have foundation problems or you want a professional opinion before buying a home, visit pinnaclefoundationrepair.com for professional guidance and support.

Moving to a new city? One of the first things to figure out is whether to rent or buy. It depends on your budget, timeline, and long-term plans, here’s how to weigh your options and make the smartest move for your current situation.

Figure Out Your Immediate Needs

Before you start browsing listings, figure out what you actually need from this move.

Temporary versus long-term: Are you just trying out a city, or are you putting down roots for several years?

Job security: Is your role stable, or are you in a probationary period where things could change?

Family and lifestyle: School districts, commute times, walkability, and access to parks or nightlife can heavily influence your housing choice.

The Case for Renting First

There is a reason many people choose to rent for at least 6 to 12 months after a move. The benefits are hard to beat.

Flexibility: Renting lets you change neighborhoods or jobs without dealing with a stressful home sale.

Lower upfront costs: Renters usually face lower upfront costs, such as a security deposit, application fees, and the first month’s rent, while buyers need to plan for a down payment, inspections, appraisals, and closing costs.

Time to explore: Take the city for a test drive and get a feel for traffic patterns and local hotspots before you buy.

A clean break: If the city or job doesn’t work out, breaking a lease is usually easier than trying to sell a house in a pinch.

Why Buy Soon After Moving?

If you are 100% sure about your move, buying soon after moving makes sense, if you have stable income, and plan to stay long enough to justify the transaction costs.

Building equity: Part of each mortgage payment can help build equity over time, though homeowners also need to budget for interest, taxes, insurance, maintenance, and other ownership costs.

Locked-in stability: With a fixed-rate mortgage, your principal and interest payment stays predictable, though property taxes, homeowners insurance, HOA fees, and maintenance costs can still change.

Complete control: You can renovate and customize your home without the approval of a property manager.

Cost Comparison: Renting versus Buying

The sticker price is never the whole story. You have to look at the total financial picture.

Monthly cost: Compare rent and renter’s insurance against a homeowner’s full monthly cost, including principal, interest, property taxes, homeowners insurance, utilities, maintenance, and any HOA fees.

Upfront payment: Renters pay deposits and application fees, while buyers pay down payments, appraisals, inspections, and closing costs.

The hidden carrying costs: If the HVAC dies, renters call the landlord. Buyers call a repairman and write a big check.

Market Conditions in Your New Location

Local conditions can tip the scale very quickly.

Home prices and trends: Is the market cooling off, or are you walking into a bidding war?

Interest rates: Higher mortgage rates reduce buying power because they make borrowing more expensive, which can lower the price range a buyer can afford.

Rental supply: A historically tight rental market may push you to buy sooner, while abundant rentals give you time to explore.

How Long Do You Plan to Stay?

Your time horizon is the golden rule of real estate.

Short-term: Renting often makes more financial sense if you expect to stay only one to three years, because buying and selling costs can outweigh the equity you build.

Long-term: Owning may become more financially attractive if you plan to stay several years beyond your local break-even point.

The break-even point: There are online calculators that can help you figure out when buying becomes more economical than renting within your specific zip code.

Know Your Credit Score and Financial Status

Before buying anything, take stock of your financial situation.

Credit history: Your credit profile can affect whether you qualify for a mortgage and the rate you are offered.

Debt-to-income ratio: Your existing debts affect exactly how much house you can afford.

Emergency savings: Buying a home can drain your savings at the same time you need a cushion for repairs, moving costs, and other unexpected expenses.

Lifestyle and Personal Preferences

Your personality is just as important as the math.

Flexibility versus roots: If you like to move around, renting can be liberating. If you want to put down roots, buying may be more satisfying.

Maintenance: Are you willing to mow the lawn and fix a leaky sink, or do you want a maintenance-free weekend?

Community: Some rentals have gyms, pools, and common areas, but with a home, you are more likely to be tied to a stronger, long-term neighborhood community.

Rent First, Buy Later

A common strategy is to rent first, then buy after you know the area better. This lets you test commute times, schools, and neighborhoods in real life. Working with a trusted local moving company can simplify that first relocation so you can focus on scouting where you might eventually purchase.

Tips for Making the Right Decision

Consult both a real estate professional and a financial advisor.

Use rent-vs-buy calculators and a detailed budget.

Visit potential neighborhoods at different times of day and talk to residents.

Common Mistakes to Avoid

Rushing into a purchase before understanding the local market.

Ignoring long-term career or family plans when choosing a location or property type.

The Bottom Line

Choosing between renting and buying after a relocation comes down to your timeline, your wallet, and the kind of lifestyle you want. There is no universal right answer. Take a breath, run the numbers, and choose the path that makes your move a little less stressful and supports the life you’re building in your new city.

A property’s true value goes far beyond the asking price and a fresh coat of paint. In the DFW market, two properties with the exact same square footage and finishes can perform very differently over time. Why? Because location, ownership rights, zoning, and future development all dictate a property’s long-term worth.

A high-priced property might actually be a bargain if it offers serious commercial upside, redevelopment opportunities, or sits in a rapidly growing neighborhood. On the flip side, an affordable home often hides costly repairs, drainage issues, title concerns, or restrictive HOA rules.

Smart buyers look beyond the photos. They study legal documents, operating costs, neighborhood trends, and future usability before making an offer. Whether you are buying a family home or a commercial investment, this guide explains the hidden factors that actually drive real estate value in North Texas.

What Does Hidden Property Value Actually Mean?

Hidden property value boils down to a property’s real-world usefulness and long-term upside. It includes legal rights, location quality, future development potential, and the flexibility to use the property how you want.

In the Metroplex, hidden value often comes from zoning flexibility, nearby growth, parking access, rental potential, and road visibility. A property near expanding retail or employment corridors will naturally appreciate faster than one in a stagnant area.

But hidden value can also work against you. Foundation damage, flood risk, old plumbing, unclear title history, or strict deed restrictions can kill your investment, even if the building looks attractive during a showing.

The Hidden Value Factors That Matter Most

These are the specific details that make or break your future resale value, ownership flexibility, income potential, and long-term operating costs:

Buyers who review these areas early make better financial decisions and avoid costly surprises at the closing table.

Listing Price vs. True Property Value: What Is the Difference?

The listing price is just a number the seller wants, while the true property value reflects what the property is realistically worth over time. The difference matters because visible upgrades do not always equal strong long-term value.

A remodeled kitchen or fresh paint may look great, but foundation problems, zoning restrictions, or high operating costs will quickly drain your equity. Meanwhile, an outdated property in a fast-growing corridor may hold massive untapped value.

Here’s a quick comparison:

Listing Price

True Property Value

Based on what the seller wants or expects

Based on the property’s real long-term worth

Often influenced by appearance and market positioning

Looks deeper at condition, ownership rights, and actual risks

Rarely accounts for hidden issues

Includes hidden risks that could affect value

Works as a starting point for negotiation

Should guide your final offer

Legal and Ownership Details You Can’t Ignore

Always review the title history, easements, deed restrictions, liens, and HOA rules before committing to any property. These legal details control what you actually own and what you are legally allowed to do with it.

An easement may limit where you can build an addition. HOA rules may restrict rentals (like Airbnb), parking, fencing, or running a business out of the property. Older properties may also carry outdated surveys or unresolved permits.

Important documents to request include:

Title commitment

Seller disclosures

Property survey

HOA documents

Permit history

Easement records

Tax history

Zoning confirmation (for commercial use)

What Are Mineral Rights and Why Do They Matter in Texas?

Mineral rights are property rights connected to underground resources like oil and gas. In Texas, it is very common for these rights to be separated from surface ownership. This means you might own the house, but someone else owns the rights to the resources underneath it.

This matters because mineral ownership can affect long-term property value and future financial opportunities. Always confirm whether any mineral interests are included in the sale and whether previous leases or reservations exist.

Understanding mineral rights value helps explain why some Texas properties hold value beyond the surface land itself.

How Easements, HOA Rules, and Deed Restrictions Affect Value

These rules directly impact your property value by limiting your flexibility. Some restrictions protect neighborhood quality, while others can become a massive headache.

A utility easement may block future construction plans. HOA rules may limit rentals, parking, landscaping, or exterior changes. Deed restrictions may prevent commercial use or specific renovations.

Never assume you can freely modify a property without reading the fine print first.

Why Location is More Than Just a Zip Code

Location creates value by driving convenience, resale demand, safety, and future growth. In Dallas, location quality almost always trumps cosmetic upgrades.

Properties near strong job centers, retail growth, highways, schools, or transit access hold stronger long-term value. Commercial properties with good visibility naturally attract more business traffic and future redevelopment interest.

Buyers should evaluate:

Commute patterns

Flood and drainage history

School district quality

Nearby retail and grocery access

Future development projects

Walkability and traffic flow

Noise from highways or nightlife

A property’s surroundings often shape its future value more than the building itself.

Spotting Commercial and Mixed-Use Potential

If you are looking at real estate from an investment standpoint, commercial potential is a huge factor. It is the ability of a property to support business activity, mixed-use conversion, rental income, or future redevelopment. Many transitional neighborhoods continue to shift toward mixed residential and commercial zoning.

Depending on local laws, a property may support retail, office, café, medical, or foodservice use. Even residential buyers should pay attention to nearby commercial activity because it affects traffic, convenience, taxes, and resale value.

The most important issue is permitted use. A building may look ideal for a storefront, but it might still require zoning approval, parking upgrades, or utility improvements before you can open for business.

The Value of Signage and Street Visibility

For commercial buyers, street visibility increases property value because businesses thrive on customer exposure and traffic. Retail, restaurant, and service-based properties command higher prices when they sit on busy corridors with clear frontage.

Visibility depends on road traffic, signage placement, lighting, and nearby intersections. However, always confirm local permit and zoning rules before assuming large signs or illuminated displays are allowed.

Existing Infrastructure: Kitchens and Foodservice

Kitchen or foodservice potential matters hugely when a property could support a restaurant, café, bakery, ghost kitchen, or catering operation.

Foodservice properties require heavy-duty plumbing, ventilation, electrical capacity, refrigeration space, and fire safety systems. A building with these systems already installed saves buyers tens of thousands of dollars in renovation costs.

When reviewing restaurant layouts and equipment needs, information about commercial kitchen equipment helps buyers understand how infrastructure affects long-term business value.

Hidden Costs That Destroy Your Budget

Renovation and operating costs can significantly change the true cost of ownership. A property with a low purchase price may still require major spending after closing.

The biggest cost factors include:

Roof and foundation repairs

HVAC replacement

Plumbing and electrical upgrades

Insurance premiums

Property taxes

Utility costs

Permit and compliance expenses

Drainage correction work

Commercial properties may also require ADA improvements, grease traps, parking changes, or fire safety upgrades. You need to estimate these costs before negotiating the final price.

How to Spot Hidden Value Before You Buy

Auditing hidden property value means reviewing the legal, structural, financial, and future-use details before purchasing.

Follow these six key steps:

Review the listing carefully for missing details or vague descriptions.

Check title history, easements, and ownership records.

Confirm zoning and permitted use.

Hire inspectors to evaluate the structure and systems.

Estimate repair, tax, insurance, and utility costs.

These questions often reveal problems that are impossible to spot during a property showing.

Red Flags That Turn Value Into Risk

Hidden value becomes hidden risk when attractive features are outweighed by structural problems, legal restrictions, or unrealistic renovation assumptions.

The biggest warning signs include:

Unclear ownership or title history

Major foundation movement

Flood or drainage issues

Restrictive zoning rules

High insurance costs

Unrealistic renovation estimates

Always be skeptical when properties are heavily discounted without a clear explanation.

The Bottom Line

You should look beyond the listing price because true property value depends on far more than appearance. Ownership rights, zoning, location quality, operating costs, and future use all shape long-term value.

A property with strong fundamentals will easily outperform a more attractive home in a weaker location. At the same time, hidden repairs or legal restrictions can quickly turn a cheap property into an expensive nightmare.

The smartest buyers treat every property as both a functional space and a long-term financial asset.

Everyone talks about building credit, but finding clear advice you can actually use is not easy. You probably know that a good credit score is essential when applying for a loan, renting an apartment, buying a car, or getting a lower interest rate. But if you’re starting from scratch or trying to get back on your feet after past mistakes, knowing where to start can be overwhelming.

You don’t need to waste time looking for shortcuts, risky schemes, or confusing advice. You can build your credit history the right way with legal, straightforward steps that show lenders you can handle credit responsibly.

For renters, homebuyers, and anyone planning to apply for a mortgage, your credit history can also affect your real estate options. A stronger credit profile can help you qualify for an apartment, a mortgage, or better loan terms when you’re ready to buy.

Here’s a look at what credit history is, why it’s important, and how to start building it in a safe, practical way.

What Is Credit History?

Credit history is a record of how you have handled borrowed money. This includes credit cards, loans, payment activity, account balances, credit limits, and how long you have had your accounts.

Lenders pull your credit report to see if you’re responsible with borrowed money. They want to know that you pay on time, keep your balances low, and don’t borrow more than you can afford.

Your credit score is directly tied to your credit history. The better your history, the easier it is to get approved for credit cards, car loans, personal loans, mortgages, and other borrowing opportunities.

Why Building Credit the Right Way Matters

When you want better credit fast, quick fixes can be really tempting. You might see posts online about credit shortcuts, new credit profiles, or alternate ID numbers. This kind of thing can get confusing, especially if you’re trying to bounce back from a low score.

For example, some people search for information about CPNs when they are looking for a fresh start. Before making any decisions, it is important to understand the facts about CPNs and learn the risks before you consider any credit-building option.

For most people, the safest way to build credit is to use your own legal identity and consistent financial habits. It takes time, but it creates a stronger foundation for later.

Start with a Secured Credit Card

One of the easiest ways to start building credit is with a secured credit card. It works just like a regular credit card but requires a refundable deposit upfront. That deposit usually becomes your credit limit.

If you put down $300, your card limit will likely be $300. You can make small purchases with the card and pay it on time.

The goal isn’t to spend a lot. The goal is to show lenders that you can use credit responsibly. A small recurring bill, like your phone bill or a subscription, can be a simple way to use the card without overspending.

A few simple rules help:

Keep your balance low.

Pay your bill on time every month.

Avoid maxing out your card.

Choose a card that reports to all three major credit bureaus.

Over time, your card issuer might upgrade you to an unsecured card if you manage the account well.

Become an Authorized User

Another way to build credit is to be added to someone else’s credit card account. This usually involves a trusted family member or close friend who adds you to their existing account as an authorized user.

If the account has a strong payment history, a low balance, and has been open for years, it may help your credit. The reason is that the account may show up as a tradeline on your credit file.

A tradeline is simply a credit account listed on a credit report. Credit cards, auto loans, student loans, and mortgages are all tradelines. Learn more about tradelines here.

Before you do this, make sure the primary account holder manages the card responsibly. If they miss payments or carry a high balance, it can hurt your credit too.

Consider a Credit Builder Loan

A credit builder loan is designed for people who want to establish or rebuild credit. It’s not like a traditional loan. Instead of getting the money upfront, you make payments, and the lender keeps the loan amount in a savings account.

Once you finish paying the loan, the money is released to you. During the loan term, your payments are usually reported to the credit bureaus.

This can be helpful because you can build a payment history and save money at the same time. It’s a practical option for people who want structure and don’t want to rely only on credit cards.

Credit builder loans are often offered by credit unions, community banks, and some online lenders.

Pay Your Bills on Time, Month After Month

Payment history is one of the most important factors in your credit profile. If your payments are reported to the credit bureaus, late payments can affect your credit.

The best way to protect your credit is to set up a system that helps you pay your bills on time.

You can:

Set up autopay.

Set up calendar reminders.

Write due dates on a monthly budget planner.

Pay at least the minimum amount before the due date.

If you can only pay the minimum amount, always pay on time rather than late.

If you think you might miss a payment, call the lender before the payment is due. Some lenders may be able to help, but it’s always best to communicate with them early.

Keep Credit Utilization Low

Credit utilization is the ratio of your balances to your limits. So, for example, if your limit is $1,000 and you have a balance of $300, you have a 30% utilization rate.

Lenders like to see lower utilization. It shows that you aren’t relying too heavily on borrowed money.

A good habit is to use your credit card lightly and pay it down before the statement date. You don’t need to carry a balance to build credit. Carrying a balance can cost you more money in interest.

Keep your utilization as low as possible, especially if you are building or rebuilding credit.

Avoid Applying for Too Many Accounts at Once

When you apply for new credit, a hard inquiry will show up on your credit report. One inquiry is usually not a big deal, but too many in a short period can make lenders nervous.

If you’re new to credit, take it slow. Pick one or two good credit-building tools and manage those well before you apply for more.

It’s better to have a handful of well-managed accounts than too many accounts you can’t keep up with.

Check Your Credit Reports

Checking your credit report is an important part of building a credit history. Your report shows what lenders actually see when they review your application.

You can request free weekly credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com.

Look for the following details:

Errors on your credit report

Wrong personal information

Accounts you don’t recognize

Wrong payment history

Old negative items

Wrong balances or credit limits

If you see something that’s wrong, you can dispute it with the credit bureau. Making sure your credit report is accurate and reflects your actual financial behavior may help.

You should also monitor your credit reports regularly so that you can catch problems early.

How Better Credit Can Help You Rent an Apartment

If you are planning to rent, your credit history can affect how landlords and property managers view your application. A stronger credit profile may help you look more reliable and financially prepared.

Good credit may help you:

Get approved for an apartment more easily.

Strengthen your rental application.

Reduce concerns from landlords or property managers.

Compete better in a tight rental market.

Avoid needing extra documentation in some cases.

Credit is not the only thing landlords look at. They may also consider income, employment history, rental history, and references. Still, a strong credit history can make your application look stronger.

How Credit History Affects Mortgage Approval

If you are planning to buy a home, credit history becomes even more important. Mortgage lenders use your credit profile to help decide whether you qualify for a loan and what terms you may receive.

Even a small difference in interest rate can change how much you pay over the life of a mortgage. That is why building credit before you start house hunting can be a smart move.

If homeownership is part of your future plan, start reviewing and improving your credit early. The sooner you build strong habits, the better prepared you may be when it is time to apply for a mortgage.

Build Good Money Habits

Opening accounts is not the only way to build credit. It’s about creating habits that help you stay in control.

A simple budget can help you know how much money is coming in, how much is going out, and how much you can safely spend. When you know your numbers, it is easier to avoid missed payments and high balances.

Try to build an emergency fund, even if you start small. Keeping extra money saved can prevent you from reaching for your credit cards when unexpected expenses come up.

Be Patient With the Process

Your credit score won’t change overnight. Lenders need to see how you handle bills over a long period before they feel comfortable approving you for more credit.

It can be frustrating when you want a quick fix, but shortcuts can make things worse.

Focus on what you can control:

Pay on time.

Use credit carefully.

Keep balances low.

Check your reports.

Avoid unnecessary debt.

Use legal credit-building tools.

Small habits can add up over time.

Smart Credit Habits Lead to Better Real Estate Opportunities

You can build credit history the right way, even if you have no credit or are trying to recover from past financial problems. A helpful Credit Privacy Number guide can also explain why safer and legal credit-building steps matter.

There’s no need for risky shortcuts or confusing tricks. Secured credit cards, authorized user accounts, credit builder loans, on-time payments, and low credit utilization can all help you build a stronger credit profile.

The most important thing is to build credit in a legal, honest, and sustainable way. It may take some patience, but the foundation you build can open the door for better financial options in the future.

If you are planning to rent an apartment, buy a home, or apply for a mortgage, now is a good time to start reviewing your credit.

House hunting in a hot market can feel like you’re already behind before you even walk through the door. Well-priced homes can draw multiple offers quickly, and buyers often feel pressured to make a major financial decision on a tight deadline.

But strong real estate decisions rarely come from chasing the crowd. They come from knowing your numbers, your market, and your limits before the right property shows up. Instead of focusing only on winning the offer, focus on buying a home that fits your life and still makes sense after closing.

1. Look Past the National Housing Headlines

Real estate is local, sometimes down to a few blocks. National headlines can help explain the broader market, but they won’t tell you what is happening in one school zone, subdivision, or condo building. One neighborhood may have tight inventory and rising prices, while a similar area nearby may be sitting longer and seeing price cuts.

Before you write an offer, study the recent comps. Look at days on market, list-to-sale price ratios, price reductions, and how many comparable homes are available. Also pay attention to local factors such as school boundaries, planned roadwork, zoning changes, flood risk, and access to transit. Two homes that look similar online can perform very differently over time because of location details buyers may not notice at first.

2. Don’t Confuse Staging with Value

A beautifully staged home is meant to make you feel at home the second you walk in. That is the point. But expensive furniture, designer lighting, and fresh paint are not the same thing as long-term value.

Look closely at the things that are expensive or impossible to change: the lot, the street, the floor plan, the natural light, the roof, the mechanical systems, and the overall condition. A polished home on a noisy road may not be a better buy than a dated home on a quieter, more desirable block. You can update finishes later. You cannot move the house to a better lot.

3. Know Your Non-Negotiables Before You Tour

In a fast market, buyers who know their priorities have a real edge. Before your first open house, split your wish list into three groups: must-haves, flexible items, and nice-to-haves.

Your budget ceiling, commute range, number of bedrooms, and school or neighborhood requirements may belong in the must-have category. Flooring, paint colors, landscaping, and light fixtures are usually flexible. Lifestyle extras, such as a wine room, gym, pool, or guest suite, should be treated as bonuses unless they truly affect how you live day to day. Clear priorities help you move quickly without letting pressure make the decision for you.

4. Understand the Full Cost of Ownership

The purchase price is only one part of the cost. Higher-end homes can come with higher taxes, insurance, utilities, maintenance, and HOA fees. Those costs matter just as much as your mortgage payment.

Before raising your offer, run the full monthly number. Include property taxes, homeowners insurance, HOA dues, utilities, landscaping, pool service, repairs, and reserves for major systems. An older HVAC system, aging roof, large yard, or oversized pool can turn an already expensive home into a much tighter monthly commitment. A smart offer is not just the one that wins. It is the one you can comfortably carry.

5. Buy for the Way You Actually Live

A home can be a strong investment, but it still has to work for your daily life. Think honestly about how you use space. Do you entertain often? Do you need a quiet home office? Do you want separation between guest rooms and primary living areas? Do you need outdoor space, storage, or easy access to medical, fitness, or wellness services?

Personal comfort matters, too. For example, someone looking for a hand and foot sweating treatment may place more value on reliable climate control, strong ventilation, shaded outdoor areas, or a private wellness space than on cosmetic upgrades. The right home should support the way you live now, not just the lifestyle you picture on a perfect weekend.

6. Keep a Second Option in Mind

During a bidding war, it is easy to convince yourself that one home is the only one that will work. Usually, it isn’t.

Step back before you stretch too far. Could a nearby neighborhood offer better value? Would a smaller home leave room in the budget for renovations? Would a less flashy property in a better location be a smarter long-term move? Having another path keeps you from treating one address like your only shot.

7. Set Your Limits Before the Offer Deadline

Offer deadlines can make buyers act fast, but fast should not mean reckless. Before the seller sets a cutoff time, decide your highest price, your preferred terms, and which contingencies you are not willing to waive.

Know your walk-away number before emotions get involved. That number should account for the appraisal, inspection findings, repairs, closing costs, and the cash you still need after closing. A clear limit makes it much easier to stay calm when counteroffers start moving quickly.

8. Watch Out for the Winner’s Curse

Winning a bidding war feels good until the numbers settle in. If the deal drains your emergency fund, forces you to waive protections you are not comfortable waiving, or leaves no room for repairs and normal life, the win may not be worth it.

The goal is not to beat every other buyer at any cost. The goal is to buy a home that protects your finances and still feels good to live in after the excitement wears off.

9. Make Preparation Your Advantage

Preparation gives you leverage. Keep your pre-approval current, understand your financing, and have your agent walk you through recent comps before you tour. Know which inspectors, lenders, and insurance contacts you would call if you had to move quickly.

A competitive market rewards buyers who can act with confidence instead of panic. When you understand the local numbers, your own budget, and the trade-offs you are willing to make, you can write a strong offer without losing sight of the bigger picture.

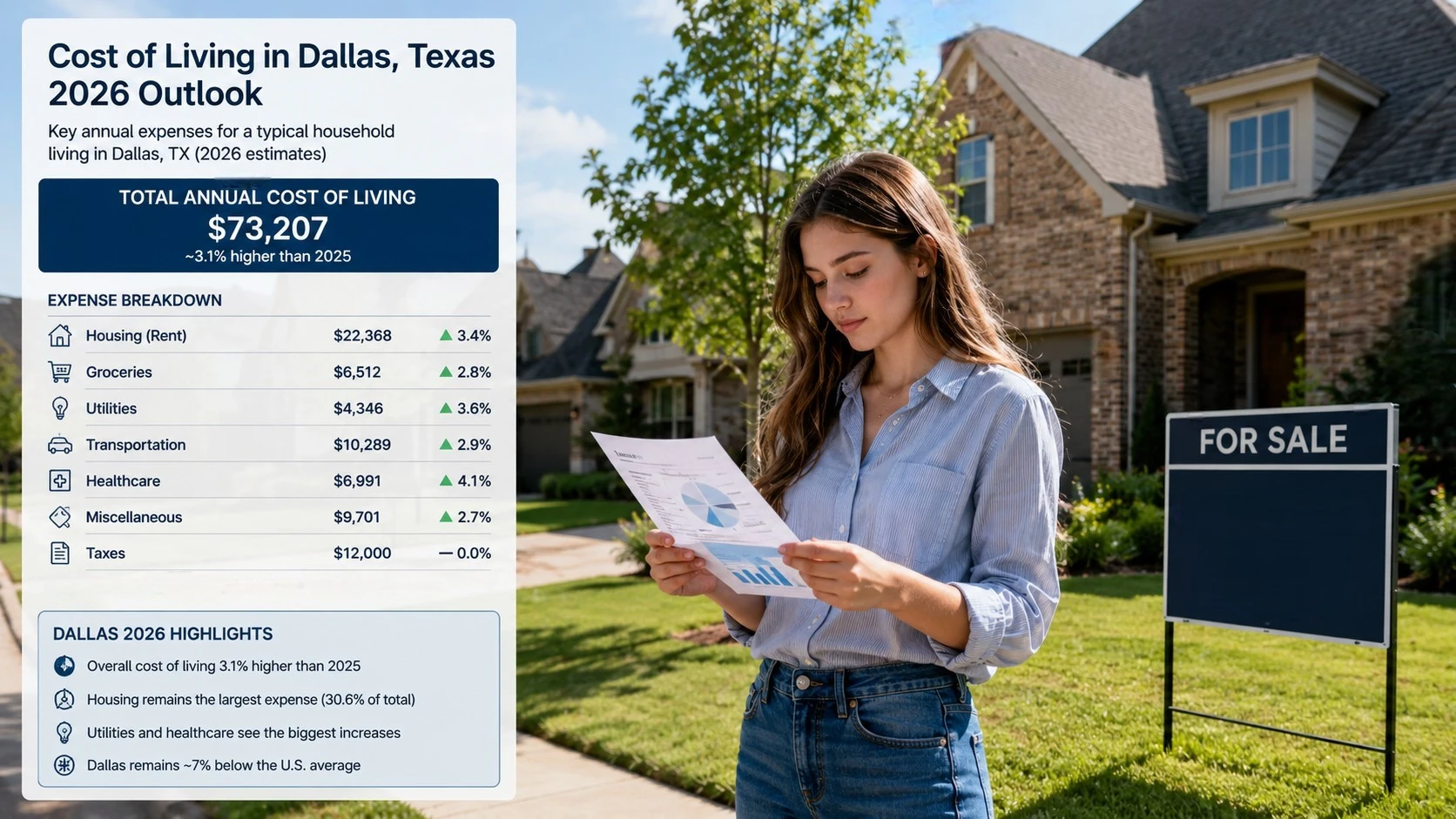

Everyone assumes Texas is cheaper. It shapes relocation conversations, “leaving California” headlines, and every TikTok about Texas freedom. But the reality is more layered, especially after two years of shifting home prices, higher insurance premiums, and bigger property-tax exemptions.

Dallas is generally more affordable than Los Angeles, New York City, San Francisco, Boston, and Seattle. But the gap is not as wide as many newcomers expect. For some buyers, the savings shrink quickly once property taxes and insurance are added to the monthly payment.

Here is what the numbers actually look like in 2026.

The Short Version on Dallas Affordability

Dallas’s overall cost of living is roughly in line with the national average. That sounds modest until you compare it with the cities people are usually leaving. Dallas still remains meaningfully more affordable than most major coastal markets.

The four numbers that really move the relocation math are state income tax, property tax, insurance, and housing prices. Get those four right and you can usually tell whether the move actually pencils out.

What Zero State Income Tax Actually Means

This is the part that does live up to the hype. Texas has no state income tax. There is no progressive bracket, no flat income-tax rate, and no surcharge on high earners because the Texas Constitution prohibits a tax on individual net income.

For someone moving from California, the difference can be substantial. Using current California tax structures and including the 2026 SDI withholding, the rough savings look like this:

At $100K income: about $5,000 to $7,000 per year versus California

At $150K income: about $10,000 to $13,000 per year

At $250K income: about $22,000 to $25,000 per year

At $500K income: roughly $50,000+ per year

California also has something many people miss: State Disability Insurance. In 2026, the SDI rate is 1.3%, and there is no taxable wage ceiling. That means a $200K California earner pays about $2,600 in SDI alone, on top of state income tax. Texas has no equivalent.

The New York comparison can be just as dramatic. NYC residents pay city income tax on top of New York State income tax, and a $200K taxable income can produce roughly $19,000 in combined state and city income tax before federal taxes.

Illinois is closer to a wash, but not completely. Illinois uses a flat 4.95% income-tax rate, so someone earning $150K still gives up roughly $7,000+ in state income tax before exemptions.

This is the foundation of every claim that Texas is more affordable. It is true, but it leaves out several major costs.

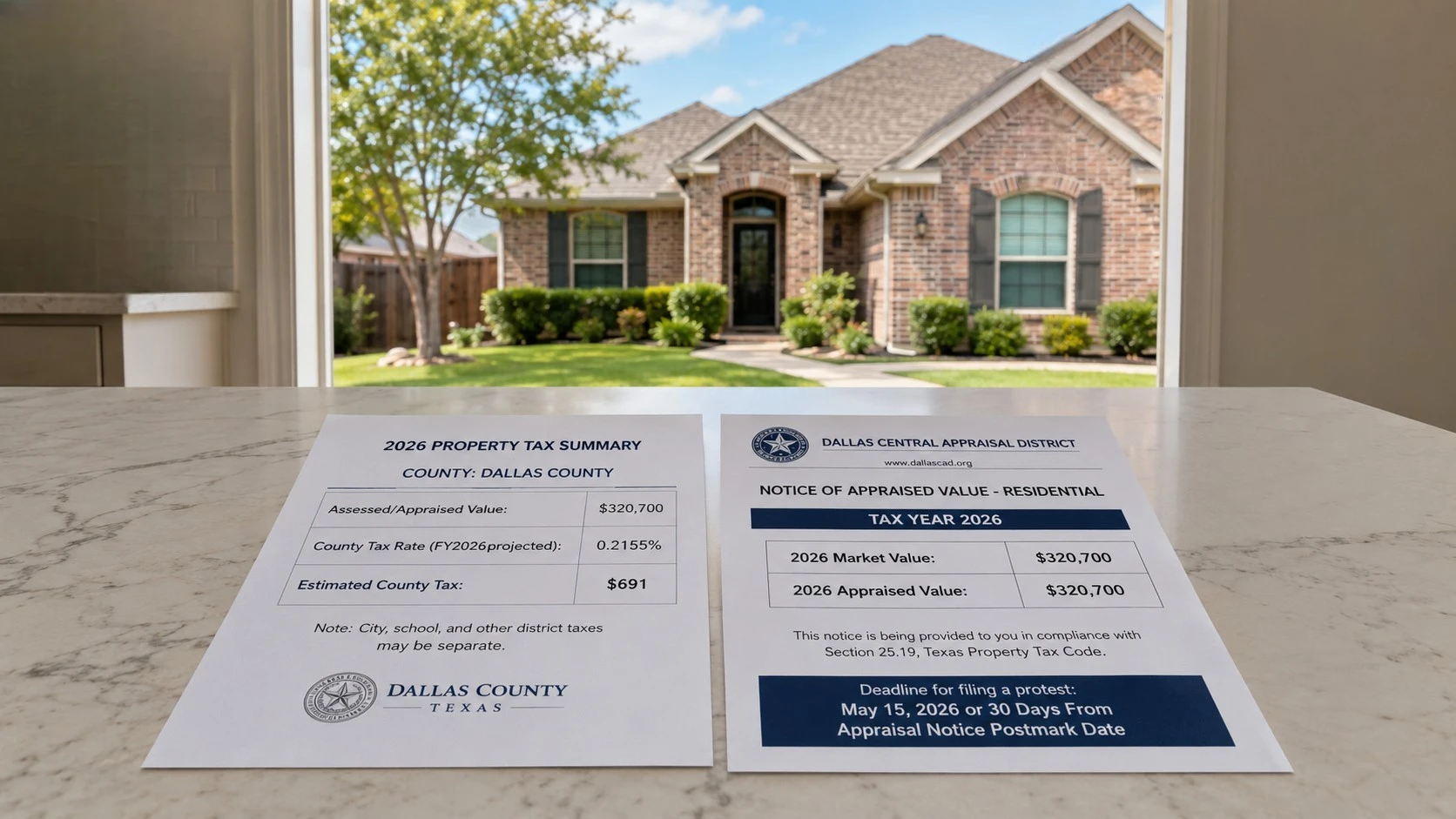

The Hidden Impact of Texas Property Taxes

Texas funds local government heavily through property taxes, and the rates are high. In many DFW cities, buyers should expect an effective property-tax burden somewhere around the high-1% to low-2% range, depending on the city, school district, exemptions, and the home’s assessed value.

In practical terms, the math can look like this:

A $500,000 home in Plano: roughly $9,000 to $11,000 per year in property tax

A $750,000 home in Frisco: roughly $13,500 to $16,500 per year

A $1,000,000 home in Southlake: roughly $18,000 to $22,000 per year, sometimes more depending on exemptions and tax rates

Now compare that with California. Proposition 13 limits the general property-tax levy to 1% of assessed value, though voter-approved local assessments can push the total above that. For long-term California homeowners, the tax bill may be far below current market value because assessed value is capped. That is why a person selling a long-held California home and buying a newer Texas home can be surprised by the property-tax reset.

Recent Texas changes help, but they do not erase the issue. SB 4 raised the school district homestead exemption from $100,000 to $140,000, and voters approved that increase through Proposition 13. Homeowners who are 65 or older, or disabled, now receive an additional $60,000 school district exemption, bringing the school exemption total to $200,000 for those homeowners.

Texas also has a 10% annual cap on increases to the appraised value of a qualified residence homestead. That cap helps long-term owners, but it does not prevent taxes from feeling expensive when someone buys into the market at today’s prices.

One practical point matters: homeowners generally need to apply for exemptions with the county appraisal district, and the usual deadline is before May 1. Missing or delaying that filing can mean paying more than necessary for a year.

Rising Insurance Premiums in 2026

Nobody talked about this much a few years ago, but Texas homeowners insurance is now one of the biggest affordability issues in the state. Dallas-Fort Worth has one of the highest insurance burdens in Texas, behind or alongside Amarillo depending on the measure.

The numbers are not small:

The average Texas home insurance premium in 2026 is about $4,085 per year

The national average is about $2,543 per year

Dallas-area quotes vary widely, but many buyers should budget roughly $3,500 to $5,000+ per year, depending on the home, roof age, deductible, carrier, coverage level, and ZIP code.

The drivers are severe weather, hail, wind claims, roof losses, and rising rebuilding costs. DFW sits in a major hail-risk region, and roof claims are a huge part of the insurance story. Some older homes can be harder or more expensive to insure, especially if the roof is aging or the carrier sees repeated storm risk.

Auto insurance follows a similar pattern. DFW drivers deal with heavy traffic, hail exposure, uninsured motorists, and vehicle-theft risk in certain ZIP codes. For many households, the combined home and auto insurance bill can eat into the income-tax savings faster than expected.

For a household budget, that means adding roughly $2,000 to $3,000 per year compared with a similar home in a lower-risk state. The income-tax savings often absorb it, but the margin is not as clean as the headline sounds.

Housing Costs Compared With Coastal Markets

The “Dallas is cheap” narrative still leans on old prices. The 2026 market is different.

In Dallas, recent market data shows:

The median sold price is about $408,000

The median listing price is about $435,000

The median rent is about $1,665 per month

The average one-bedroom apartment rent is about $1,400 per month, depending on source and neighborhood

The suburbs can be much higher. Collin County’s median listing price is around $500,000, Frisco is around $700,000, Plano is around $538,000, and Celina is around $585,000.

Compare that with other markets:

Los Angeles County median listing price is about $950,000

New York City average one-bedroom rent is about $4,100 per month

Chicago median listing price is about $355,000

Denver median listing price is about $541,000

Dallas is genuinely cheaper than Los Angeles, New York City, San Francisco, and Denver on most housing comparisons. Chicago is the tricky one. Chicago can still be cheaper for buyers, depending on the neighborhood, although property taxes and state income tax change the full picture.

For renters, Dallas is much easier to defend. Renters get most of the Dallas affordability advantage without taking on property tax, roof risk, or homeowners insurance. A renter moving from New York or Los Angeles to Dallas can see the savings immediately in the monthly budget.

Utilities, Groceries, and Daily Living Expenses

The smaller categories matter too. Dallas is not expensive across the board, but it is not low-cost in every category.

Here is where Dallas lands relative to the national average:

Housing: 8% below national average

Utilities: 16% above national average

Groceries: 1% below national average

Healthcare: 4% above national average

Clothing: 6% above national average

Entertainment and personal services: 6% above national average

Transportation: below the national average in this dataset, though car dependency still matters

The utility number deserves attention. Texas summers are long, hot, and expensive. Air conditioning can run hard from June through September, and many households see summer electric bills jump sharply.. Texas does have a deregulated electricity market, so you can shop providers. Choosing the wrong plan can cost hundreds of dollars a year. Choosing the right one can soften the summer-bill shock.

Sales tax is also part of the equation. Dallas has an 8.25% combined sales tax rate in 2026. That is not unusual for a big U.S. city, but it still matters because Texas relies more heavily on consumption taxes and property taxes instead of state income tax.

Comparing Dallas to Los Angeles

For a single filer earning $150K and buying around a $500K home, Dallas usually wins, but not by as much as people expect.

Category

Los Angeles

Dallas

State income tax

High, based on California brackets

$0

SDI charge

1.3% of wages, no wage ceiling

$0

Property tax

Often lower for long-term owners under Prop 13

Often higher as a percentage of value

Home insurance

Varies, but often lower than North Texas for standard risk

Often higher because of hail and storm risk

Auto insurance

Expensive

Also expensive in many ZIP codes

Bottom line

Baseline

Usually cheaper, but not automatic

Renters moving from Los Angeles to Dallas usually save much more. A Dallas one-bedroom averages around $1,400, while Los Angeles averages around $2,180 for a one-bedroom apartment. That alone can save roughly $9,000+ per year before taxes.

Comparing Dallas to New York City

New York City to Dallas is the clearest cost drop for many households. NYC rent, city income tax, state income tax, and daily living costs are all heavy.

A New York renter moving to Dallas can often cut rent by thousands per month. But there is a lifestyle trade-off. New York offers walkability and transit. Dallas is far more car-dependent, so newcomers may add a car payment, insurance, gas, tolls, parking, and maintenance.

Even with that added car cost, Dallas usually comes out ahead financially for most NYC movers. The bigger question is whether the lifestyle change works.

Comparing Dallas to Chicago

This is the comparison that surprises people. Chicago has lower median listing prices than Dallas, stronger public transit, and many neighborhoods where buyers can get more home for less money.

But Illinois has a 4.95% flat income tax, and property taxes in the Chicago area can be high. The savings from moving to Dallas are smaller here than they are for someone leaving California or New York. For some households, Chicago may actually be cheaper on pure housing cost. Dallas wins more often on job growth, taxes, newer housing stock, and long-term metro growth.

Comparing Dallas to Denver

Denver is a more straightforward comparison. Colorado has a flat 4.4% income tax, and Denver home prices remain higher than Dallas in many comparable areas. A $150K earner can save about $6,600 per year in Colorado state income tax alone by moving to Texas, before property tax and insurance differences.

Insurance is not a clean win either way because both regions deal with hail. But for many buyers, Dallas still comes out cheaper because the housing entry point is lower.

Who Benefits Most From Moving to Dallas

Here is who tends to save the most:

Big winners:

Renters at almost any income level, especially those leaving coastal markets

High earners buying homes under about $600K

Remote workers keeping coastal salaries

Business owners with pass-through income

Retirees with modest taxable income, since Texas does not tax Social Security or retirement income at the state level

Moderate beneficiaries:

Middle-income families buying homes between $400K and $700K

People moving from California, New York, or Illinois for a similar salary

Buyers who file their homestead exemption on time

Households that shop insurance and electricity plans carefully

Likely break-even cases:

Buyers purchasing homes above $800K

Long-term California homeowners protected by Prop 13 who sell and rebuy in Texas

People moving from Chicago or other relatively affordable Midwest metros

Households with multiple cars and high insurance costs

Potentially higher-cost cases:

Retirees with expensive paid-off California homes who buy expensive Texas homes

Buyers who forget to file the homestead exemption

Buyers purchasing older homes with roof, foundation, or insurance issues

Luxury buyers who assume Texas property taxes will be low because the state has no income tax

The Final Verdict on Relocation Costs

Dallas is cheaper than the coastal markets people are usually leaving, but the savings are not automatic. The income-tax advantage is the biggest reason the math works. Property tax and insurance are the biggest offsets.

A simple way to estimate it:

Take your projected income.

Subtract what you would pay in your current state income tax.

Add back the higher Texas property-tax burden.

Add the likely insurance difference.

Then compare housing costs honestly, not emotionally.

For most households earning above $100,000 and buying under $600,000 to $700,000, Dallas still pencils out. For renters, the move is usually strongly favorable. For buyers above $1 million, the math gets much closer than the headlines suggest.

The good news is that none of this requires guessing. County appraisal districts publish tax information. Insurance quotes are free. Electricity plans can be compared before move-in. Take-home-pay calculators are easy to run. The people who get burned are usually the ones who trust the “Texas is cheap” narrative instead of doing the math.

Once the numbers work on paper, the next variable is execution. A move to Dallas is not just a truck and a closing date. It can involve HOA rules, elevator reservations, gated-community access, storage timing, utility setup, and a few days of overlap between homes. Hiring a Dallas moving company that understands both interstate relocations and local DFW moves can make that transition much less stressful.

Texas is probably cheaper than where you came from. But the margin is smaller than the internet makes it sound, and the savings only happen when the numbers are handled carefully.

The first thing people notice about a foreclosure is the price. Fair enough. The second thing, if they’re honest, is the fantasy. Cheap house, quick cleanup, instant equity, and maybe a nice flip story to tell later. But while that fantasy is powerful, it also gets buyers into trouble.

If you’re looking at foreclosed homes, start with facts, not emotions. A lot of people use ForeclosureHub to see what’s actually on the market, what stage the property is in, and whether the deal even exists outside a catchy listing headline. That part matters more than most buyers think.

Foreclosures can be a smart buy, but they can also turn into slow, expensive messes. The line between them is usually the boring stuff like title work, repair estimates, local comps, and whether you’re buying with enough cash left over to survive bad surprises.

Why Buyers Chase Foreclosures in the First Place

A foreclosure often enters the market because the lender wants the property off their books. There’s no owner repainting the kitchen and baking cookies before showings. There’s no sentimental pricing and no family arguing over whether granddad’s old place is worth more because of the memories. That can create room for a buyer who’s paying attention.

In the best-case scenario, you buy below market value, fix what needs fixing, and either move in with equity already built in or rent it out at numbers that actually work. That last part is huge right now. Plenty of standard listings look fine until you run the math and realize the rent won’t support the payment, taxes, insurance, and repairs. A foreclosure, bought right, can give you breathing room.

There’s another advantage people don’t talk about enough. Distressed properties scare casual buyers away. Many don’t want to deal with repairs or uncertainty. Some hear the word “foreclosure” and assume every deal is cursed. That hesitation can reduce competition, especially on rougher homes.

But remember, this is not free money. It never was.

The Real Advantages of Buying a Foreclosure

A lower basis can change everything When investors talk about a good buy, they’re usually talking about basis. What you’re all-in for, not just the purchase price. If a foreclosure lets you come in lower than a comparable traditional sale, your options improve fast.

That’s the ideal situation, and it happens, just not automatically.

Lenders are usually less emotional than traditional sellers

Banks can be frustrating, slow, and weirdly rigid, but they’re not sentimental. They’re not rejecting your offer because they feel your family isn’t the right fit for the home. If the numbers, terms, and timing work, the deal can move. The process is often more mechanical, which some buyers actually prefer.

Value can be created, not just hoped for

A foreclosure with ugly paint, dated flooring, and neglected landscaping might look awful to a first-time buyer. To someone experienced, that can be a great opportunity. Cosmetic distress is where money can be made. Structural distress is where money disappears. That distinction matters more than the listing discount.

Where the Risks Start Sneaking In

Here’s the part that wipes out a lot of great deals. Buyers focus on the discount and stop asking important questions about the home’s true condition, who still has a claim against it, and whether it can be properly inspected. They also forget to check if anyone is still living there or what it will actually cost to make the property financeable, rentable, or livable. Those are the questions that separate a smart purchase from a financial migraine.

‘As-Is’ Really Means As-Is

Foreclosures are often sold as-is. People hear that and think they might just need to replace some carpet. In reality, as-is can mean anything from needs paint to the plumbing was stripped and the basement has been wet for eight months. It can mean the seller won’t fix a single item, won’t offer credits, and may not know much about the home in the first place. That’s not a reason to walk away every time, but it is a reason to get serious.

Hidden damage is common, and not always visible

Vacant homes age badly and quickly. A tiny roof leak becomes interior damage. A broken window becomes moisture, pests, mold, and vandalism. A property that sat without utilities can have HVAC, plumbing, or appliance issues that only show up later. Photos rarely tell the whole truth, and sometimes they tell almost none of it. This is where foreclosure buyers get themselves in trouble by estimating repairs from a phone screen. That habit is expensive.

Title problems can outlive the previous owner

A cheap house with a messy title isn’t cheap. It’s a problem. Depending on the state and the foreclosure process, you could be dealing with unpaid property taxes, HOA balances, junior liens, judgments, or old contractor claims. Some of these get wiped out, while others don’t. You need to know which is which before closing, not after. if you skip title work because you’re trying to save money, you’re buying blind.

Occupancy can become its own project

Some foreclosure properties are vacant, which is great, but others are not. The former owner or a tenant might still be living there. Maybe someone’s cousin, who no one mentioned, has been staying in the back room for months. Taking possession isn’t always a clean process, and legal removal takes time. Time costs money. If your whole plan depends on getting keys and starting renovations the next morning, you’re assuming too much.

Not Every Foreclosure Deal Works the Same Way

This part gets glossed over online, but it matters a lot.

Pre-foreclosure

This is the stage before the auction, when the owner is behind but still technically in control. These deals can offer better access and more normal negotiation. They can also be emotionally complicated, because you’re dealing with a distressed seller under pressure.

Auction property

This is where people get starry-eyed and sometimes wiped out. At auction, you may need cash, fast deposits, and a willingness to buy with limited access. You might not be able to inspect the interior, and title issues are often less clear than you’d like. The discount can be real, but so is the risk.

REO, or bank-owned property

If the property doesn’t sell at auction, it often becomes bank-owned. This is usually the most accessible version for everyday buyers because it tends to look more like a traditional sale. You might get inside and have the chance to inspect it. You still need to read every line of the bank addendum because those contracts are written to protect the seller, not the buyer.

Red Flags That Should Slow You Down

You don’t need to walk away from every deal, but you do need to slow down when the warning signs pile up.

visible water damage, foundation movement, or missing systems

a seller pushing speed while giving little documentation

One red flag isn’t always a dealbreaker, but several usually mean trouble.

A Smarter Way to Approach Buying a Foreclosure

What to do before you commit:

Figure out the foreclosure stage first. Pre-foreclosure, auction, and REO are different animals.

Run real comps, not wishful ones. Use sold data from the immediate area.

Get a repair number from someone who actually swings a hammer.

Order title work early when possible, and ask direct questions about liens, taxes, and HOA balances.

Budget for delays. Not hypothetical delays, but actual delays.

Leave yourself a cash cushion, because the first estimate is rarely the last number.

That’s not glamorous advice, but it’s the stuff that keeps a good buy from becoming a regret.

So, Is Buying a Foreclosure Worth It?

Sometimes, absolutely. Foreclosures can give disciplined buyers a real edge. You can get a better entry price, higher upside, less competition, and stronger long-term returns if the property is in the right area and the numbers make sense. But the keyword there is disciplined. If you’re buying on emotion, assuming the house is probably fine, or counting on everything to go smoothly, you’re doing it wrong. Foreclosures reward patience, cash reserves, local knowledge, and a strong stomach for details. They punish shortcuts.