A national survey from CopperSmith shows that more people see their home as more than just a place to live. It has become the space where they expect to recharge. The study found that most Americans struggle to relax in their own homes, and in Texas, where big houses and busy routines often meet, the results highlight something important for buyers, sellers and homeowners to think about.

How Often Do Americans Truly Relax at Home?

The CopperSmith survey of 1,000 U.S. adults found that just 26% of Americans feel they truly relax at home daily. For most, it doesn’t happen right away. About 42% said they need at least thirty minutes after getting home before they feel settled, while just 14% said they can relax as soon as they walk in.

Generational differences showed up as well. Only 9% of Gen Z respondents said they could relax immediately. Women also reported more difficulty than men: 45% said they need at least half an hour, compared to 39% of men.

For many Dallas households dealing with long workdays, Central Expressway traffic, and family obligations, these numbers reflect a familiar reality, finding calm at home often takes extra effort.

Home Size and Everyday Stress

Texas is known for bigger houses, but the survey shows that extra square footage doesn’t always make life calmer. About 39% of people said clutter or crowded rooms are a main reason they can’t relax.

Other common obstacles included:

45% said they feel too busy

30% said they feel guilty about “doing nothing”

30% said noise or too much stimulation gets in the way

Even in larger Dallas homes, the way a space is designed and used matters. A big living room full of clutter can feel just as stressful as a small apartment.

Ways People Relax at Home

Most Americans still choose simple activities to relax. In the survey:

51% said lying in bed or on the couch

48% said watching TV or streaming

29% said scrolling on a phone

19% said taking a bath or shower

The living room was the most common place to relax (64%), followed by the bedroom (49%). Outdoor areas came in at 28% and kitchens at 27%.

For homeowners in Dallas, these results point to the value of open family rooms, comfortable outdoor patios, and bathrooms that feel more like a spa. These features support relaxation and can also add value to a home.

Types of Relaxation at Home

The study pointed to six main ways people prefer to relax. Each group shows a different habit or focus:

Slowdweller (33%) – likes stillness and downtime.

Hushitect (20%) – pays attention to calming design.

Soulsoaker (15%) – enjoys baths and water routines.

Hearthmind (12%) – sees home as part of personal identity.

Glowmad (10%) – relies on light, candles, or scent.

Simmercrafter (10%) – relaxes through cooking.

For Texas, these groups matter. They hint at what buyers may notice when walking through a house. A Glowmad may be drawn to accent lighting or a fireplace. A Soulsoaker may look first at the bathroom.

What This Means for Dallas Homes

Relaxation is now part of the selling story. Homes with spa-style bathrooms stand out. Outdoor features like covered patios, a pool, or a small garden space are in demand.

Inside the home, clutter-free rooms make a difference. They look better in photos and help create a calm feeling during showings. Multi-use spaces also matter. A home office that can work as a yoga room, or a guest room that doubles as a reading corner, adds value.

For sellers, presenting the home as a place to recharge can be a simple but strong advantage. For buyers, it’s a reminder that square footage alone is not enough.

Practical Tips for Homeowners

The study shows that creating a more relaxing home does not always require a major remodel. Small adjustments can have a noticeable effect. Some practical steps include:

Upgrading lighting to set a calmer mood.

Adding outdoor furniture or shade to make patios more usable.

Using open layouts or rearranging furniture to reduce clutter.

Staging rooms with neutral colors and minimal décor for a clean look.

In a city known for long workdays and busy traffic, these changes can make a home easier to live in and easier to market.

Key Takeaways

The survey makes clear that many Americans are looking for calm at home, and not all houses deliver it. For Dallas residents, this can be seen both as a challenge and an opportunity. Homes with spa-style bathrooms, outdoor spaces, or organized layouts support daily comfort and stand out in the housing market.

As buyers continue to look for properties that provide a sense of retreat, homes that emphasize relaxation will carry more appeal.

The housing market in California continues to grow, with demand often surpassing the supply of available homes. Competition is fierce, and many buyers struggle to secure financing under traditional bank rules. Strict qualification standards often exclude capable borrowers such as entrepreneurs and even seasoned investors.

ID Mortgage Broker addresses this challenge by offering lending strategies designed for today’s diverse buyers. Through flexible financing, clients gain an edge in a fast-moving market and can pursue opportunities with greater confidence.

Meeting the Needs of Modern Borrowers

Financial lives rarely follow a single pattern. Many buyers are small business owners, independent contractors, or professionals with non-traditional income streams. For them, rigid documentation requirements create barriers that do not reflect their actual financial health.

Programs like the no-doc loan in California show how alternative lending adapts to these realities. By recognizing cash flow, business revenue, and other forms of stability, these loans expand access to financing. This flexibility enables buyers to secure properties that might otherwise be out of their reach.

Flexible Lending Options for Today’s Buyers

Alternative lending uses a broader view of financial health. Instead of relying solely on tax returns or W2 forms, lenders also consider bank statements, business income, and consistent cash flow. This approach gives buyers with unconventional income sources a fair chance to qualify for financing.

Flexibility in Documentation

Income can be shown through contracts, rental earnings, or personal statements rather than standard paperwork. This flexibility opens the door for more borrowers to secure loans and pursue ownership.

Streamlined Approvals

With fewer documentation hurdles, approvals move faster. Shorter timelines give buyers an edge in real estate markets where homes often sell within days.

Why It Matters in Competitive Bidding

In many markets, properties often receive multiple offers. Buyers who can act quickly and present flexible documentation are better positioned to win contracts. This speed and adaptability help them secure homes in sought-after neighborhoods.

Who Benefits Most?

Flexible lending is designed for buyers who don’t always fit the “traditional” borrower mold. Looking beyond rigid paperwork, it opens doors for people in many different situations. Here are a few examples:

Entrepreneurs & Small Business Owners

Have strong earnings but inconsistent tax filings.

Benefit from qualifying with bank statements or business revenue instead of W-2s.

Gain access to homeownership while continuing to grow their business.

Real Estate Investors

Often move quickly to secure properties in competitive neighborhoods.

Avoid delays caused by heavy documentation requirements.

Benefit from faster approvals that allow them to act before competitors.

Families Seeking a Second Home

Already own a primary residence but want a vacation home or rental property.

Standard banks may hesitate due to existing mortgages.

Flexible loan structures help them qualify, combining lifestyle upgrades with long-term financial returns.

The Broker’s Role

The right lending strategy can determine a buyer’s success. Mortgage brokers guide clients through financing options and make sure each loan fits their specific circumstances. Their knowledge gives buyers the confidence to move forward in a highly competitive environment.

Connectors: Brokers link clients with lenders and loan programs that reflect their financial situation.

Educators: They explain the benefits and risks of different financing choices, giving buyers the insight to make sound decisions.

Strategists: Brokers position clients to succeed in markets where speed and preparation carry weight.

Trusted partners: ID Mortgage Broker delivers tailored solutions designed to meet immediate needs while supporting long-term ownership and investment goals.

In real estate, the right broker acts as a partner who equips buyers with the tools, knowledge, and confidence to secure the right property at the right moment.

Looking Ahead: A More Inclusive Market

Alternative lending is steadily moving toward mainstream adoption. As more borrowers rely on non-traditional income, the demand for flexible loan options will continue to rise. Technology will streamline the process with faster approvals and easier documentation, while brokers remain essential in guiding clients to the right solutions.

A housing market that embraces inclusivity and flexibility creates more opportunities for families, investors, and entrepreneurs to participate.

Opening Doors with Flexible Lending

Flexible lending is creating fresh chances for homeownership. With the right broker at your side, intimidating financial hurdles shrink into small steps you can actually manage. Buyers gain the confidence to move fast, grab the property they want, and start building a stronger future in one of the most competitive real estate environments in the country

Ready to make your move? Call a trusted mortgage broker today and see how flexible lending can turn your goals into keys for the front door.

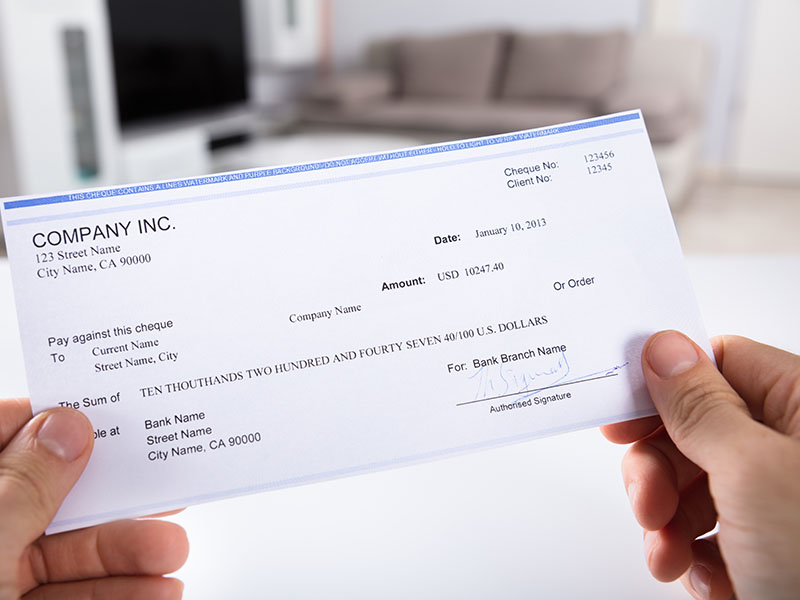

Margaret Chen, a retired teacher, received a check in the amount of $47,000 last month; she had no idea that she was entitled to this money. The money was the result of a life insurance policy her deceased husband had been paying through his employer twenty years ago.

Although the case of Margaret might seem extrordinary, it is not the only one. All over California, thousands of people have discovered forgotten accounts, refunds and benefits worth a few dollars to hundreds of thousands. These tales show that unclaimed property is not a legend, but a very real chance of ordinary Californians to take.

Image Source: istockphoto.com. An unexpected windfall: an unclaimed property recovery check worth over $10,000.

Small Claims, Big Impact: The $50–$500 Range

Even small recoveries can bring relief, especially in California’s high-cost environment.

A college student in Los Angeles uncovered $127 from an old apartment deposit, just enough to cover new textbooks.

A young professional in San Diego recovered $340 from a canceled car insurance policy, which helped cover groceries.

A retiree in Sacramento discovered an $89 account from a credit union membership dating back 15 years, which is enough for medication refills.

A family in Fresno found out that they had $456 in unclaimed wages due to the seasonal agricultural work and it made back-to-school shopping a possibility.

Such smaller checks might not hit the news but at just the right time. Everybody has had utility deposits, bank accounts or insurance policies that may reappear years in the future.

Mid-Range Recoveries: $1,000–$10,000 Life Changers

At the mid-range, forgotten assets become life-changing opportunities.

A single mother in Oakland claimed $3,200 from a workers’ compensation settlement, wiping out credit card debt.

A Bay Area tech worker discovered $7,800 in old stock options from an acquired startup, enough to pay graduate tuition.

A couple in San Jose found an old CD that had 4,500 that they used to repair their house.

A small business owner in Riverside recouped $9,100 in vendor refunds to help maintain payroll in a slow period.

Such recoveries are indicative of how unclaimed property may be used to relieve debt burdens, fund education or even support businesses. In the active economy of California, where technological transactions, company shutdowns, and moves are the order of the day, thousands of residents have such opportunities lying right under their noses.

Estate and Inheritance Recoveries: $10,000–$50,000

Larger recoveries often stem from estates and inheritances. These cases are more complex, requiring documentation and family coordination. Many Californians turn to ClaimNotify for support in navigating such claims.

Adult children in San Diego recovered $23,000 from their father’s pension.

A widow in Orange County uncovered $31,000 from her late husband’s life insurance policy.

A Modesto family located $18,500 from their grandmother’s forgotten bank accounts.

In Long Beach, heirs obtained a recovery of an investment account of an uncle of $42,000.

These amounts tend to come into the picture at emotionally trying times, and are both a relief financially, as well as a relief in the form of keeping a loved one alive. Although the paperwork may take months, families always claim that it is worth the effort.

Major Recoveries: $50,000–$200,000 Game Changer

In the six-figure range, unclaimed property can reshape lives.

A corporate executive retrieved $89,000 from a profit-sharing plan tied to a long-ago merger.

A real estate investor recovered $134,000 from an escrow error.

An entertainment professional received $67,000 in residuals from film and TV projects.

A business owner discovered $156,000 from a partnership dissolution settlement.

Amounts like these enable major financial decisions: college funding, early retirement, or home purchases. The claims process, however, often involves months of verification and professional support. California’s industries, tech, real estate, and entertainment generate unusually large unclaimed balances, making the state one of the most fertile grounds for such windfalls.

The Exceptional Cases: $200,000+ Extraordinary Finds

Some rare cases reach extraordinary sums.

California’s largest known recovery exceeded $800,000.

A San Francisco family uncovered $340,000 from a forgotten investment portfolio.

Former business partners found $275,000 in unclaimed distributions.

An international escrow account held $520,000 for a Californian who had moved abroad.

These exceptional claims involve lawyers, courts, and sometimes global agencies. While uncommon, they demonstrate that unclaimed property is not limited to pocket change; it can represent life-changing wealth.

Common Threads: What These Stories Teach Us

Despite the variety, common lessons stand out:

Life transitions, such as job changes, moves, and deaths, are the biggest triggers.

California’s economy generates higher-value claims than most states.

Old accounts grow in value; time doesn’t erase claims.

Multiple properties per person are common.

Bigger claims mean more paperwork, often requiring patience.

Professional tools like ClaimNotify help streamline complex filings.

The key takeaway is that persistence and complete documentation lead to success. Too many people give up when claims seem complicated, leaving money behind that could ease financial strain or create new opportunities.

Your Story Could Be Next

These stories are not hypothetical; they represent real Californians who turned forgotten accounts into financial relief. From $50 utility deposits to $800,000 inheritances, recoveries happen across all walks of life. If you live in California, there’s a real chance money is waiting for you, too. A quick search, paired with tools like ClaimNotify, could uncover funds you never imagined existed. Don’t assume the state is holding someone else’s property. Your success story could be next.

If you’re a homeowner, chances are you’ve built up more equity than you realize. In 2025, Americans hold an estimated $17 trillion in home equity, and many lenders are creating new ways for you to tap into that value for renovations, debt consolidation, or even new investments.

The challenge is that most traditional lenders require a stack of paperwork before approving you. For many self-employed borrowers or those with inconsistent income, that can be a deal breaker.

A No Doc HELOC removes that barrier. Instead of asking for tax returns or pay stubs, it gives you the option to borrow against your home’s equity with far less documentation. The application process is faster and simpler, though you’ll usually pay a higher interest rate in exchange for that convenience.

Understanding No Doc HELOC Loans

If you’re interested in using your home equity but don’t want to go through a long paperwork process, a No Doc HELOC could be an option. In this section, you’ll learn how these loans work, who they’re most useful for, and what the main benefits and drawbacks look like in today’s market.

What Does “No Doc” Mean in Lending?

When lenders talk about “No Doc,” they’re referring to loans that don’t require the usual income documents. You won’t be asked for pay stubs, W-2s, or years of tax returns. Instead, approval is based on your credit history, the amount of equity in your home, and your overall financial situation.

This type of lending is often used by people who are self-employed, run their own business, or have income that isn’t easy to show on paper. The appeal is that it’s faster and requires less back and forth. The trade-off is cost. Lenders typically set higher interest rates or ask for more equity to reduce their risk. In other words, you gain convenience, but you’ll want to weigh it against the added expense.

How a No Doc HELOC Works Compared to Traditional HELOCs

A No Doc HELOC isn’t all that different from a traditional home equity line of credit. You’re still tapping into the value of your home and paying back only what you draw. Where things change is in the approval process.

With a standard HELOC, the lender expects a paper trail like tax returns, W-2s, pay stubs, the works. A No Doc HELOC skips that step. Instead, your credit score, the equity you’ve built, and your overall financial health carry more weight in the decision.

For someone who earns income in less conventional ways, that can make the process feel a lot smoother. The trade-off is cost. You’ll usually see higher interest rates or stricter terms because the lender is taking on more risk without that traditional proof of income.

Feature

No Doc HELOC

Traditional HELOC

Income Verification

No tax returns, W-2s, or pay stubs required.

Requires full documentation of income

Approval Criteria

Based on credit score, home equity, and asset profile

Based on income, credit score, and debt-to-income ratio

Speed

Faster approvals due to minimal paperwork

Longer processing due to detailed verification

Interest Rates

Typically higher (8%–12%) to offset lender risk

Lower on average (6%–10%)

Best For

Self-employed, freelancers, investors

Salaried employees with steady income

Drawbacks

Higher cost, stricter equity requirements

Slower process, more documentation burden

No Doc HELOC vs. No Doc Mortgage: Key Differences

A No Doc HELOC and a No Doc mortgage may sound alike because both avoid the usual income paperwork, but they’re not designed for the same situation. A HELOC works like a revolving credit line, letting you borrow against your home’s equity as the need comes up. You only pay interest on what you use, which makes it practical for projects that happen over time, such as remodeling one year, replacing the roof the next or for tapping into opportunities where you don’t need all the money at once.

A No Doc mortgage takes a different shape. Instead of ongoing access, you receive the full loan amount at closing and repay it in fixed monthly installments. That kind of loan is better suited for a single, larger goal, like buying a new property or refinancing into different terms. So the real difference is flexibility: a HELOC keeps the line open for repeat borrowing, while a mortgage delivers one lump sum with predictable payments from the start.

Why Borrowers Choose a No Doc HELOC

For many homeowners, a No Doc HELOC can be a practical alternative when the traditional loan process becomes too rigid or paperwork-heavy.

Instead of getting slowed down by income documentation, borrowers can tap into their home’s equity more directly, which makes it appealing if your finances don’t fit neatly into standard lending requirements.

Benefits for Self-Employed and Retirees

People who are self-employed, run their own business, or live on investment income often find themselves in this position. Retirees can run into the same challenge. Even with steady earnings or substantial assets, proving income on paper isn’t always straightforward. Irregular cash flow, tax strategies, or earnings that don’t come with W-2s can hold up a traditional loan.

A No Doc HELOC avoids that hurdle by placing more weight on your credit profile and the equity in your home instead of focusing only on tax returns and pay stubs.

Speed and Simplicity in Approval

For many borrowers, one of the biggest advantages of a No Doc HELOC is how quickly the process can move. Traditional loans often get held up while you gather income paperwork or wait for a lender to review every line of your tax returns. Without that hurdle, applications tend to move faster, which can matter a lot if you’re dealing with urgent home repairs, need to cover a business expense, or want to take advantage of an investment opportunity before it slips away.

Avoiding the Refinance Rate Trap

Another reason borrowers look at this option has to do with today’s mortgage rates. If you already locked in a low-rate mortgage, refinancing just to access your equity could mean replacing it with a much higher rate. That’s a tough trade-off for many homeowners. A No Doc HELOC gives you another path, you can leave your existing mortgage untouched while still unlocking your equity. That way, you keep the benefit of your lower rate and still get the cash you need.

The speed of approval and the ability to protect your current mortgage terms make a No Doc HELOC attractive for a wide range of situations.

Who Qualifies for a No Doc HELOC Loan?

Even though a No Doc HELOC skips the usual income paperwork, lenders still want to see that you’re financially stable. Approval doesn’t come without standards, it just shifts the focus to equity, credit, and overall financial health.

Home equity is the starting point. Most lenders expect you to own at least 20% of your home, and they’ll usually limit the total line of credit to around 70–80% of the property’s value. Credit score plays a big role as well. Without tax returns or pay stubs, your credit history does the heavy lifting. A score in the upper 600s is often the minimum, while borrowers with scores in the 700s and above tend to get the best terms.

The type of property matters too. You can take out a No Doc HELOC on your primary residence, a second home, or even an investment property, though lenders are usually stricter with homes that aren’t owner-occupied. Beyond property type, they’ll still look at the bigger financial picture, your history of making payments, the reserves you have set aside, and whether your overall profile suggests you’ll be able to manage the new debt responsibly.

So while the paperwork burden is lighter, lenders still hold to clear standards. Strong equity, solid credit, and a stable financial base put you in a good position to qualify.

Current No Doc HELOC Rates and Terms in 2025

Rates and terms for no documentation home equity lines of credit (No Doc HELOCs) in 2025 can look a little different depending on the lender, but some clear trends stand out.

How Rates Compare to Traditional HELOCs

In 2025, most No Doc HELOC rates fall between 8% and 12%. Your actual rate depends on factors like your credit score, loan-to-value (LTV) ratio, and the type of property you’re borrowing against. These rates usually run about 1% to 3% higher than what you’d find with a standard HELOC, mainly because lenders are taking on more risk when they approve a line of credit without reviewing income documentation.

Typical Draw and Repayment Periods

Most No Doc HELOCs give you a draw period of 5 to 10 years, which is when you can take out money as you need it. After that, the account moves into the repayment phase. Repayment terms are commonly 10 to 20 years, during which you’ll pay both principal and interest until the balance is fully cleared. The length of each period will depend on the lender’s program and the agreement you sign.

Interest-Only Payment Options

Some lenders let you make interest-only payments during the draw period. This setup can lower your monthly payment in the beginning, making it easier to manage cash flow if you’re balancing other expenses. The trade-off is that your principal balance doesn’t shrink during that time, so once the repayment period begins, your monthly payment can climb quickly. If you’re considering this option, it helps to plan ahead so you’re not caught off guard when the payment structure changes.

How to Find the Best No Doc HELOC Lenders

Picking the right No Doc HELOC lender isn’t just about chasing the lowest rate. You want a lender that’s competitive on terms and one you can trust.

Where to Look: Banks, Credit Unions, and Specialty Lenders

Some banks and credit unions still offer these loans, but they’re not always easy to qualify for. That’s why many borrowers go to specialty lenders that focus on people with nontraditional income.

Truss Financial Group is one of the bigger names here. They’ve built programs for self-employed borrowers, retirees, and investors who don’t fit the standard W-2 mold. Their process is meant to move quickly, and you’ll usually have someone walking you through each step until funding.

What to Compare: Rates, Fees, and LTV Caps

Don’t stop at the headline rate. Take a close look at the APR since it includes fees. Ask about closing costs and loan-to-value limits too, because those can change how much you’re really able to borrow.

Truss Financial Group has earned attention for offering flexible terms and competitive pricing, with programs that cover not just primary homes but second homes and rentals as well.

Spotting a Reputable Lender

Good lenders are upfront. They’ll explain rates, fees, and terms without rushing you. You should get clear answers in writing, and they’ll take the time to go over your questions.

Truss Financial Group has strong reviews for being transparent and responsive. That’s what you want. On the flip side, if a lender dodges questions, won’t put numbers in writing, or pushes you to sign before you’re ready, that’s a red flag.

Is a No Doc HELOC Right for You?

A No Doc HELOC isn’t for everyone. It comes down to how much equity you have, how steady your credit looks, and what you plan to do with the money.

When It Makes Sense

This type of loan can work well if you’ve built up solid equity, have good credit, and your income doesn’t fit neatly into pay stubs or tax returns. Think business owners who write off a lot of expenses, retirees living off investments, or property investors with rental income.

It can also be a smart option if you need quick access to cash without disturbing a low-rate mortgage you already have. Many borrowers use the funds for renovations, debt payoff, or even to jump on another investment.

When to Steer Clear

If your finances are unsteady, your credit is shaky, or you don’t have much equity, a No Doc HELOC could backfire. Rates are higher than standard HELOCs, so borrowing gets expensive fast if you can’t pay it back on schedule. And if you already qualify for a regular HELOC at a lower rate, there’s little reason to pay extra just for convenience.

Putting It Together

A No Doc HELOC tends to work best for borrowers who value speed and flexibility over the cheapest rate. If you’re confident you can manage the payments, it can open the door to cash that would otherwise be tied up in your home.

Final Thoughts

For a lot of self-employed homeowners, showing income on paper is tougher than it sounds. Write-offs and business expenses can make tax returns look leaner than they really are, and traditional lenders don’t always account for that.

That’s where a No Doc HELOC can make a difference. Instead of dealing with stacks of paperwork, it gives you a quicker way to unlock the equity sitting in your home. The process is faster, more flexible, and designed for borrowers whose financial strength doesn’t show up neatly on a W-2.

If your income comes from a business, multiple sources, or seasonal work, this type of loan can help you keep cash flow steady, fund new projects, or cover investments, all without touching the low-rate mortgage you already have. With the right lender, a No Doc HELOC can be less of a hurdle and more of a tool to keep your plans moving. With the right lender, it’s a tool that works for you, not against you

The US construction industry is a vast enterprise that generates more than $2 trillion annually. Almost 8 million Americans are working in this huge sector.

We’re not just talking about building houses. The construction world covers housing, commercial spaces, infrastructure and energy projects.

Its activity is spread across all 50 states, with Texas, California and Florida currently leading in new builds.

The industry rises and falls with changes in interest rates, material costs, and labor supply. In recent years, construction growth has battled against inflation, supply chain disruptions and a shortage of skilled workers.

Yet innovation is driving growth across the sector. New materials, technologies and methods can provide sustainable growth for decades to come.But you may be asking, where do I start? And what is the best way to get construction leads in a manner where I can save time and get the best results.

Traditional Construction Leads

Construction companies used to rely on word of mouth. Personal referrals-built reputations which bought new leads.

Then came local advertising in newspapers and trade magazines. Networking at trade shows and industry events brought new contacts.

Some firms bid on public tenders posted in print or on municipal boards. Direct mail was increasingly used.

Companies sent flyers to local businesses and homeowners. Good relationships with architects, developers and suppliers were key to sustainable success.

But these methods were slow, and results depended on personal trust with lots of time spent building it.

Innovative Lead Generation

In today’s construction world, digital platforms often now produce leads. A company’s website acts as a 24/7 portfolio.

Search engine optimisation is crucial to ensure visibility on Google. At the same time social media campaigns might target developers, investors and homeowners.

LinkedIn ads can connect directly with decision-makers. Platforms like Houzz and Angi list contractors for residential and commercial projects.

Online tender portals now speed up the bidding process. CRM software can track prospects from the first contact to a signed contract and beyond.

Virtual tours can showcase projects without site visits and data analytics can identify growth markets by zip code.

With these technologies constructors can reach national and global audiences quicker and more cost-effectively than ever before.

The Benefits of Sustainable Growth

Sustainable growth can keep a construction business profitable over the long term. It’s the best way to avoid those boom-and-bust cycles.

Revenue increases steadily, costs remain under control and cash flow is stable. Construction companies achieve this by prioritising a reputation that lasts decades – not just winning the next job.

There’s another meaning to “sustainable” too. Clients increasingly demand eco-friendly, energy-efficient buildings.

Today’s investors often prioritise firms with strong environmental credentials. Many federal and state incentives reward green building projects.

It makes sense on a simple level too. Materials costs are rising so waste reduction saves money.

Public opinion favours companies that minimise carbon footprints so reputation and contacts will spread. Many large contracts require proof of the constructor’s sustainability policies.

And in some cases the most skilled workers will want to join companies with a future-focused vision. Sustainable growth is both an ethical choice – and a commercial necessity.

The Future of the US Construction Industry

The US construction industry may be a vast operation but it is at a turning point. The old methods still have value but innovation is the surest way to progress in the future.

Those that embrace digital tools, sustainable practices and smarter lead generation will be able to reshape the market. The companies that adapt will thrive.

Demand for green, efficient and technologically advanced projects is expected to grow across the US. Federal infrastructure spending and private investment will create new opportunities for forward-thinking companies.

The major challenges like skilled labor shortages and rising costs will push the industry toward greater efficiency and creativity. The path forward is to build smarter, build greener and to build for the long term.

Sustainable growth is not just becoming possible, it is going to be the new industry standard.

Every year, Fresno drivers face thousands of traffic collisions, many of them along Highway 99, State Route 41, and the busy streets near downtown. The heavy mix of commuters, farm trucks, and local traffic creates conditions where one driver’s careless mistake can change another person’s life in seconds.

Have you been injured in a car accident? If you were hit by a negligent driver in Fresno, you’re not alone. From rollovers near Clovis Avenue to rear-end crashes on Shaw or Blackstone, serious accidents happen across the city on a daily basis. Knowing what steps to take after a crash can help you protect your health, your finances, and your legal rights.

Understanding Negligence

Negligence in a car accident case refers to careless or reckless driving that violates traffic laws and creates unsafe conditions. Examples in Fresno include speeding on Highway 41, failing to stop at a red light downtown, or driving while distracted on Highway 99.

California law requires proof of negligence to hold a driver responsible after a crash. The main elements are:

The driver had a duty to operate their vehicle safely.

The driver breached that duty through careless or reckless behavior.

The breach caused the accident and resulted in injuries.

Evidence of negligence may include police reports, traffic citations, medical records, and statements from witnesses. These records help connect the driver’s conduct to the injuries sustained and are often necessary to establish liability in a personal injury claim.

Gathering Evidence

After a crash, the details you collect can make or break your case. In Fresno, people usually start by taking photos of the scene, such as the cars, the street, the traffic lights, even the skid marks on the pavement.

Eyewitnesses are another important piece. A passerby who saw a driver run the light at Blackstone and Shaw, or a neighbor who heard the impact outside their home, can back up what you’ve said. Police reports add to that picture too, since officers write down what they observed and may note if a driver broke the law.

Medical records are often the final link. Hospital charts, X-rays, and therapy notes connect your injuries directly to the crash. Together, these records show not only what happened but also what it cost you physically and financially.

Seeking Medical Attention

Getting medical help right after a crash isn’t just about taking care of your health — it also creates the records that tie your injuries to the accident. In Fresno, emergency rooms at Community Regional Medical Center or Saint Agnes often see car accident victims within hours of a collision. Even if you don’t feel badly hurt at first, it’s smart to get checked out, because some injuries don’t show up right away.

Those medical records become a timeline of what happened to you. Doctor’s notes, X-rays, prescriptions, and therapy recommendations all show how the crash affected your body. When it comes time to deal with insurance companies, those records can be the strongest proof that your injuries were real and caused by the accident.

Prompt treatment also keeps the other side from arguing that your injuries came from somewhere else. If you wait weeks before seeing a doctor, the insurance adjuster will likely question whether the accident was to blame.

Consulting Legal Professionals

Dealing with the legal side of a car accident can get overwhelming fast. Insurance adjusters may call you within days, and the paperwork piles up quickly. That’s when having a Fresno personal injury lawyer can make a difference. An attorney who knows the local courts and has handled Central Valley accident cases before can step in and guide you through the process.

Instead of trying to track down every record yourself or arguing with an insurance rep on the phone, your lawyer takes that off your plate. They can gather police reports, request medical files, and talk to witnesses who saw the crash. If things go further, they’re the one standing with you in Fresno County court, making sure your side of the story is heard.

Knowing someone else is keeping track of deadlines and dealing with the back-and-forth lets you focus on getting better.

Filing an Insurance Claim

After the dust settles, most people in Fresno end up dealing with insurance. That usually means making a call, reporting the crash, and sending over whatever paperwork the company asks for. It sounds simple, but it rarely is.

Adjusters don’t always take your word for it. Some will press you on the details of the crash or act like your injuries aren’t that serious. Having photos, the police report, and your medical records on hand gives you something solid to back yourself up. The National Highway Traffic Safety Administration also emphasizes the importance of proper documentation, since it can be critical in proving the extent of your losses.

Keep track of costs as they come in. Hospital bills, physical therapy, and even the paychecks you missed are part of the picture. Having that information ready makes the claims process smoother and helps you fight for a settlement that actually covers your losses.

Considering Legal Action

Sometimes an insurance claim just doesn’t get you where you need to be. If the settlement offer falls short or the company keeps dragging its feet, the next option may be filing a lawsuit against the negligent driver.

Filing a lawsuit takes more time than dealing with insurance. In Fresno County Superior Court, it’s not unusual for a case to stretch out for months. There are hearings, paperwork, and back-and-forth between lawyers. In some cases it ends in a trial, in others it settles before you ever see a courtroom.

Before going down that path, it’s worth talking it through with your attorney. They can look at the facts, weigh the chances of success, and let you know whether filing suit is the right move.

Understanding Compensation

What you can recover after a crash depends on how badly it changes your day-to-day life. For many people in Fresno, that starts with hospital bills and the cost of follow-up care, like therapy or medication. Lost wages often add to the strain if you’re forced to take weeks off work.

But it doesn’t stop there. California law also recognizes the less visible side of an accident, the pain that lingers, the anxiety about driving again, or the way an injury keeps you from doing things you used to enjoy.

Every situation is different. A sprained shoulder that heals in a month won’t be treated the same as a spinal injury that changes how you work and live for years. Having a lawyer explain the range of possible outcomes helps set expectations and gives you a clearer picture of what a fair resolution looks like.

Promoting Road Safety

Holding a negligent driver accountable isn’t just about your own case. It also shows that dangerous driving has consequences. In a city like Fresno, where Highway 99 and Shaw Avenue stay packed most of the day, one reckless move can affect far more than the driver making it.

When people see that accidents lead to lawsuits or higher insurance rates, most think twice before running a red light or checking their phone behind the wheel. That shift in behavior makes daily driving a little safer for everyone, whether you’re commuting to work, dropping kids off at school, or just running errands.

For accident victims, the goal is justice and financial recovery. For the community, it’s about encouraging safer habits and building a culture of responsibility on the road..

Emotional Support and Recovery

Car accidents don’t only cause physical injuries. In Fresno, many people find themselves nervous about driving again or dealing with stress long after the crash.

Support is often practical. Family or friends may give rides, handle errands, or sit with you during appointments. Professional counseling and local support groups are another option for anyone coping with anxiety or sleep problems after a collision.

Emotional recovery is part of the process, just like medical treatment.

Conclusion

Holding negligent drivers accountable takes a series of steps. Gathering evidence, seeking medical care, working with a lawyer, and pursuing an insurance claim or lawsuit all play a role. For people in Fresno, the goal is twofold: to recover from the accident and to encourage safer driving in the community.